.webp)

Listen To Our Podcast🎧

Introduction

MiCA compliance crypto is no longer a future planning exercise, the EU's Markets in Crypto-Assets Regulation entered full application in December 2024, and the clock is running for crypto-asset service providers, banks with digital asset operations, and fintechs serving European customers. Missing these obligations means licensing denials, operational shutdowns, and AML enforcement actions that can follow a firm across jurisdictions.

This guide covers exactly what MiCA demands from a practical standpoint: CASP licensing, aml compliance requirements, kyc automation mandates, sar filing obligations, and the anti money laundering technology decisions that will define your audit readiness in 2026. Whether you manage compliance at a bank adding crypto custody or lead a fintech team with a lean BSA/AML function, the steps here are specific and actionable.

- What Is MiCA and Why It Changes Everything for Crypto Compliance

- MiCA Compliance Crypto: Core Licensing and Operational Requirements

- AML Compliance Under MiCA: What Banks and CASPs Must Prepare

- How KYC Automation in 2026 Meets MiCA's Identity Requirements

- SAR Filing Requirements and CTR Filing Rules Under MiCA

Onboard Customers in Seconds

What Is MiCA and Why It Changes Everything for Crypto Compliance

MiCA (Markets in Crypto-Assets Regulation) is the EU's first comprehensive licensing and conduct framework for crypto-asset service providers (CASPs). Full application began December 30, 2024, under Regulation (EU) 2023/1114, covering CASPs under Title V and token issuers under Titles III and IV.

Unlike the patchwork of national crypto regimes it replaced, MiCA creates one rulebook across all 27 EU member states. A CASP authorized in France can passport its services to Germany without additional licensing. The downside: there is no longer a low-scrutiny jurisdiction to operate from within the EU.

The regulation applies to exchanges, trading platforms, custodians, wallet providers, portfolio managers, advisors, and token issuers. Banks holding MiFID II authorization get a transitional window, but they still need to register as CASPs if they actively offer crypto services to retail or professional clients.

How MiCA Intersects with Existing BSA/AML Frameworks

MiCA does not replace the EU's Anti-Money Laundering Directive (AMLD6) or the Transfer of Funds Regulation, it operates alongside them. For firms already running aml compliance programs under AMLD5 or US FinCEN rules, MiCA adds a licensing layer on top. The risk-based AML approach still applies, meaning your existing aml risk assessment guide needs to specifically account for crypto-asset typologies: DeFi exposure, mixer usage, peer-to-peer transactions, and stablecoin velocity patterns that simply do not appear in traditional payment risk models.

The EU AI Act's Impact on Financial Services Compliance

Firms using AI-driven transaction monitoring or automated KYC decisioning now face a second regulatory layer: the eu ai act financial services provisions. Under Regulation (EU) 2024/1689, AI systems used for credit scoring, risk classification, and AML screening fall under the "high-risk" category in Annex III, requiring conformity assessments, human oversight mechanisms, and detailed audit trails. If your compliance stack includes machine learning models for SAR triggering or sanctions screening, those models need formal documentation with explainability requirements. Most firms are underestimating this overlap with MiCA authorization timelines.

MiCA Compliance Crypto: Core Licensing and Operational Requirements

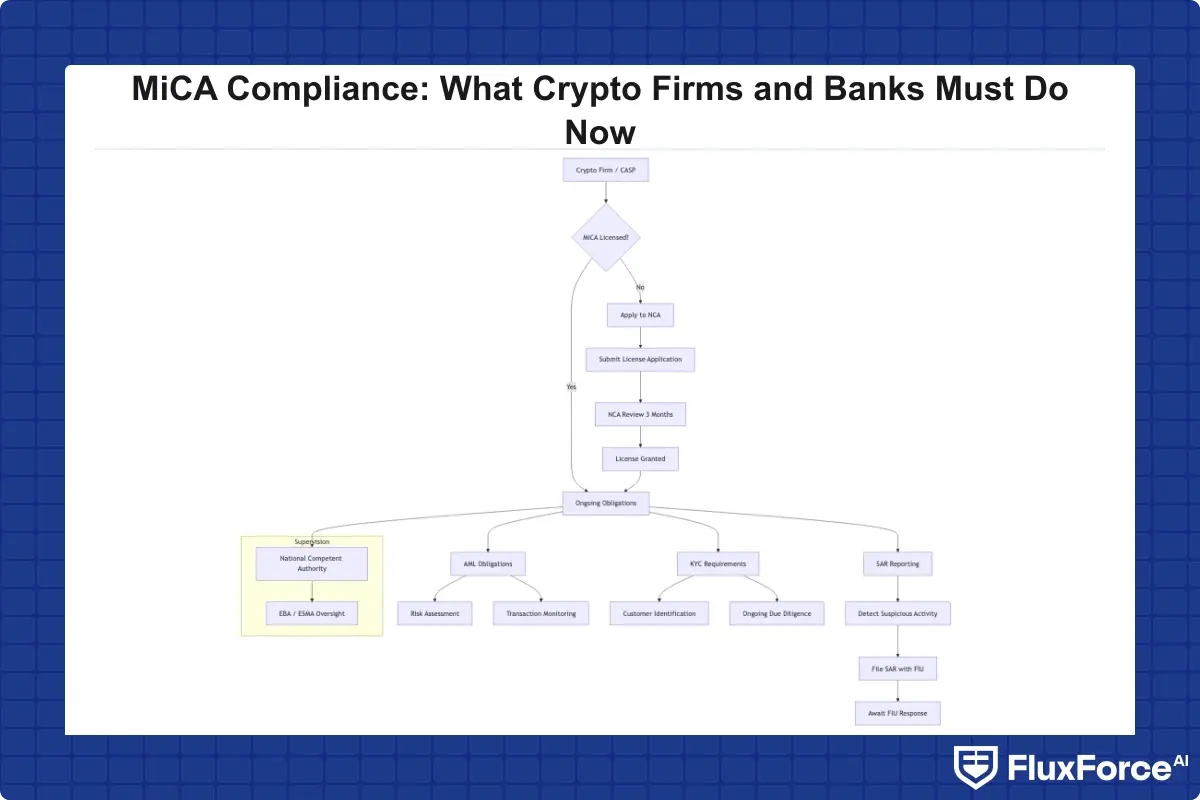

MiCA compliance crypto starts with authorization, not policy. A CASP cannot offer services in the EU without a license from its home-state national competent authority (NCA), which then notifies the European Securities and Markets Authority (ESMA). ESMA's guidelines set the minimum standards NCAs apply during evaluation, and several have already issued rejection letters for applications missing required AML documentation.

CASP Authorization Requirements

The authorization application requires:

- A detailed business plan covering the specific crypto-asset services to be offered

- Governance arrangements including fitness and propriety checks on management body members

- A written AML/CFT policy and procedures manual specific to crypto-asset activities

- Conflict of interest policies covering proprietary trading alongside client orders

- Safeguarding arrangements for client assets, segregated accounts or equivalent insurance coverage

- ICT risk management documentation aligned with DORA for in-scope firms

Authorization timelines vary by NCA but typically run 40 to 90 working days. Firms that submitted incomplete applications in early 2024 faced resubmission requests, adding months to their timelines. Several larger exchanges have reported six-month authorization processes in Germany and France. Quality on the first submission matters significantly.

Capital and Safeguarding Rules

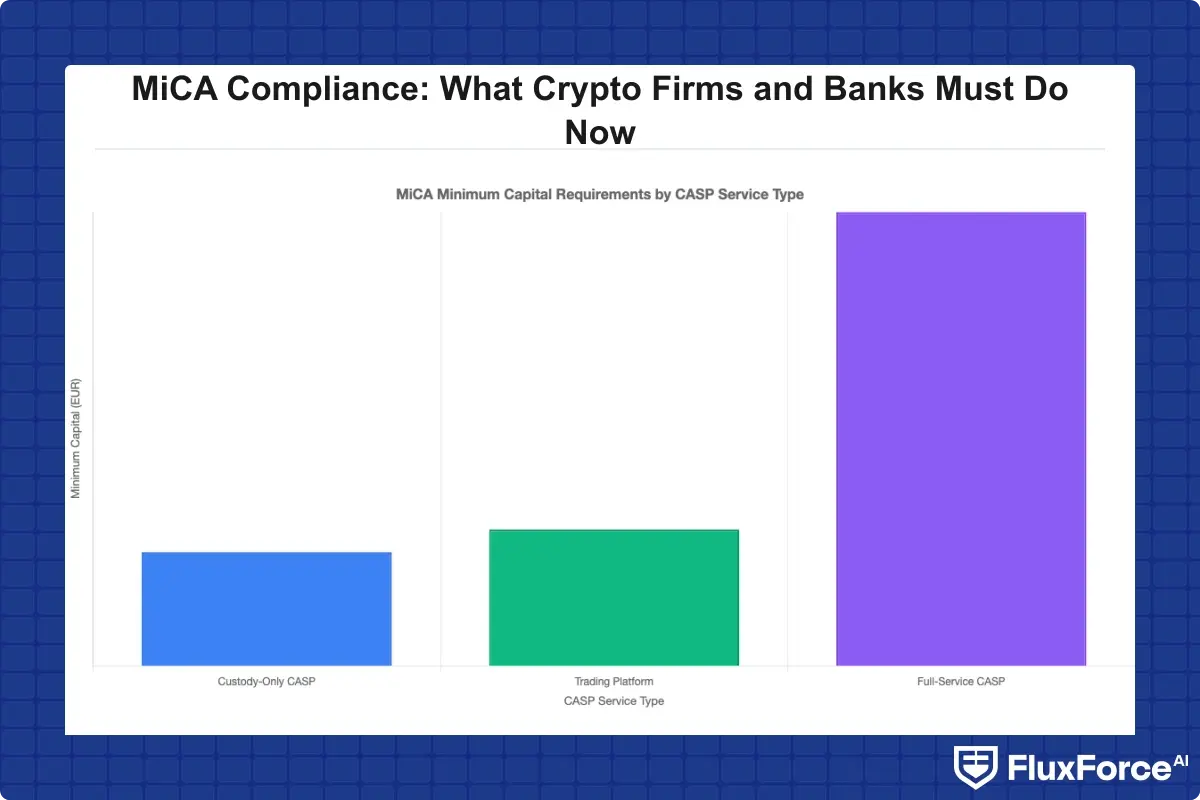

Minimum capital requirements under MiCA depend on service type: custody-only CASPs need at least €125,000; firms offering trading or exchange services need €150,000; full-service operations can require up to €500,000 depending on configuration. These numbers are modest by banking standards, but the safeguarding rules are operationally demanding. Client crypto assets must be held in segregated accounts, and any shortfall must be covered from own funds within 30 days. For banks already managing capital adequacy ratios in the hundreds of millions, the capitalization floor is easy, the operational segregation requirements are the harder lift.

AML Compliance Under MiCA: What Banks and CASPs Must Prepare

Strong aml compliance is the operational foundation of any MiCA authorization. Regulators can revoke a CASP license specifically for AML failures, and the revised Transfer of Funds Regulation adds crypto-specific requirements that go well beyond what traditional fiat AML programs address. Three requirements in particular catch compliance teams off guard.

Travel Rule Compliance for Crypto Transfers

The TFR requires CASPs to collect, verify, and transmit originator and beneficiary information for all crypto-asset transfers, regardless of amount. There is no de minimis threshold for crypto, unlike the €1,000 threshold that applies to wire transfers. Your aml compliance software must capture and transmit this information in real time, which means VASP-to-VASP communication protocols, typically via TRISA, OpenVASP, or proprietary integrations, must be live before you process your first customer transfer.

The practical challenge is unhosted wallet transfers. When a customer sends to or receives from a self-hosted wallet, the CASP must apply additional risk measures and, for transfers above €1,000, collect a written self-declaration from the customer. A documented policy on unhosted wallet handling needs to exist before regulators ask for it during a supervisory visit.

AML Compliance Fintech Considerations

Fintechs offering crypto rails or embedded crypto features face aml compliance fintech complexity that pure CASPs do not. If your fintech already holds a payment institution license under PSD2, you carry both payment AML obligations and MiCA CASP obligations simultaneously. Customer risk profiles built for fiat transactions do not automatically map to crypto behavior, a customer with a clean payment history may use a mixing service for crypto, which creates a fundamentally different risk profile that your existing scoring models will miss.

For teams managing AML risk checks across digital payment and lending contexts, the lesson applies directly: customer risk profiles need crypto-specific data points added explicitly, not just a bolt-on checkbox in your existing onboarding form.

Building a BSA AML Compliance Checklist for MiCA

A bsa aml compliance checklist adapted for MiCA should include:

- Customer identification program (CIP) with crypto-specific ID verification steps

- Beneficial ownership verification for legal entity customers

- Transaction monitoring rules tuned for crypto typologies, including blockchain analytics integration

- Travel Rule data collection and transmission procedures with tested VASP-to-VASP workflows

- Unhosted wallet handling policy with documented risk thresholds

- SAR filing procedures for suspicious crypto activity

- Annual BSA/AML training updated with MiCA-specific scenarios

- Independent AML audit at least annually for licensed CASPs

For bsa aml compliance community banks considering crypto custody or brokerage services, this checklist is the starting floor. Community banks face the additional challenge of mapping crypto risk into an existing BSA program without a dedicated crypto compliance specialist on staff.

How KYC Automation in 2026 Meets MiCA's Identity Requirements

MiCA's authorization requirements set a high bar for identity verification. CASPs must verify customer identity before onboarding, conduct ongoing monitoring, and apply enhanced due diligence for high-risk relationships. Doing this manually at any meaningful transaction volume is not viable, the question is which kyc automation approach fits your risk profile and operational budget.

KYC Automation 2026: What Changes Under MiCA

kyc automation 2026 under MiCA goes beyond document scanning. The regulation's alignment with AMLD6 requires:

- Liveness detection to prevent spoofed identity documents submitted remotely

- Sanctions screening at onboarding and on an ongoing basis as lists update

- Politically Exposed Person (PEP) screening combined with adverse media monitoring

- Beneficial ownership verification for corporate customers, not just individuals

The kyc cdd requirements banks are already familiar with from fiat operations carry over directly, but crypto adds wallet address screening as a mandatory component. A customer may pass KYC with clean identity documents but present elevated risk because their registered wallet address received funds from a sanctioned exchange. Your automation stack needs to combine identity verification with on-chain analytics from day one, not as a retrofit.

Enhanced Due Diligence Guide for High-Risk CASPs

Enhanced due diligence (EDD) under MiCA applies to customers identified as high risk through your risk assessment process. The enhanced due diligence guide principle is direct: collect more information, obtain senior management approval for onboarding, and increase monitoring frequency. For crypto specifically, EDD triggers include:

- Customers from jurisdictions flagged on FATF's grey and black lists

- Customers who frequently transact with unhosted or anonymized wallets

- Businesses dealing in high-anonymity assets such as privacy coins

- Politically exposed persons and their close associates

EDD does not mean refusing the customer, it means documenting your decision to accept the risk and putting proportionate controls in place. Compliance teams frequently fail EDD audits not because their controls are weak but because their documentation is thin or inconsistent across case files.

SAR Filing Requirements and CTR Filing Rules Under MiCA

SAR filing is where mica compliance crypto moves from paperwork to operational reality. MiCA routes through national FIU reporting channels rather than creating a new regime, but it adds crypto-specific context that traditional financial crime teams must understand before the first suspicious transaction hits their queue.

SAR Filing Best Practices for Crypto Firms

sar filing best practices for crypto differ from traditional finance in one significant way: on-chain evidence. When you file a SAR (or the EU equivalent, a Suspicious Transaction Report), include blockchain transaction hashes, wallet addresses, and blockchain analytics findings where available. This makes the report far more actionable for law enforcement and demonstrates your technical monitoring capability to regulators reviewing your program quality.

A suspicious activity report guide for crypto operations should address:

- When blockchain analytics findings alone are sufficient to trigger a SAR, even without conventional financial red flags

- How to identify structuring patterns specific to crypto, multiple small transfers designed to stay below Travel Rule thresholds

- Whether a transaction blocked for sanctions reasons also requires a concurrent SAR filing, which is typically yes depending on jurisdiction

- sar filing efficiency: building workflows that move from detection to submission without exceeding reporting deadlines, which typically run 30 days from suspicion formation across EU jurisdictions

One critical note on sar filing requirements 2026: ESMA's supervisory guidance confirms that tipping-off prohibitions apply to crypto exactly as they apply to traditional finance. You cannot disclose to a customer why their transaction was blocked if that disclosure would compromise a pending SAR.

CTR Filing Rules for CASPs

ctr filing rules vary by jurisdiction. Most EU member states have transaction reporting equivalents for large crypto transactions, with thresholds generally aligned to AMLD6 requirements. In the US, FinCEN's BSA requirements apply to crypto exchanges registered as money services businesses, with CTR thresholds at $10,000 per transaction. For CASPs operating across multiple jurisdictions, your aml compliance software needs country-specific CTR thresholds mapped and automated to avoid missed filings that create examination findings.

In the US, FinCEN's BSA requirements apply to crypto exchanges registered as money services businesses, with CTR thresholds at $10,000 per transaction.

Anti-Money Laundering Technology for MiCA Readiness

The anti money laundering technology landscape in 2026 looks different from what compliance teams built their stacks on five years ago. Rule-based transaction monitoring systems designed for traditional payment flows struggle with crypto's transaction velocity, cross-chain complexity, and rapidly evolving typologies. MiCA creates hard deadlines that force the technology decision.

What AML Compliance Software Must Do Under MiCA

aml compliance software for MiCA-regulated CASPs needs four core capabilities working together:

- On-chain transaction monitoring with blockchain analytics integration, Chainalysis, TRM Labs, Elliptic, or equivalent, providing entity risk scores in real time

- Travel Rule data exchange with other CASPs via TRISA or a comparable interoperability protocol

- Real-time sanctions screening against OFAC, EU consolidated list, UN sanctions, and HM Treasury lists running simultaneously

- Case management and SAR generation with complete audit trails that satisfy NCA inspection requirements

Platforms offering regulatory compliance automation that consolidate these capabilities reduce the manual operational burden significantly. Connecting four separate point solutions instead creates data gaps that appear during regulatory audits as unexplained monitoring blind spots, an examiner finding you do not want to field.

Anti-Money Laundering Technology 2026 Trends

anti money laundering technology 2026 is moving toward graph analytics and behavioral AI at scale. Rule-based monitoring catches known patterns; graph analytics surfaces unknown ones by mapping relationship networks across wallets, entities, and multi-chain transaction flows. Three developments worth tracking now:

- Federated learning for AML models: financial institutions sharing model improvements without sharing raw transaction data, improving detection quality without privacy violations

- Cross-chain monitoring: as crypto activity migrates between blockchains via bridges and wrapped assets, monitoring limited to a single chain misses substantial risk exposure

- AI-assisted SAR drafting: reducing per-SAR preparation time from 45 minutes to under 10 minutes while maintaining narrative quality, a genuine sar filing efficiency gain for teams handling high SAR volumes

For teams evaluating how AI is cutting false positives in AML transaction monitoring, the underlying principle is the same: behavioral machine learning at transaction scale consistently outperforms static rule sets, particularly for crypto typologies that rules have not yet been written to catch.

What Community Banks and Fintechs Must Do Differently

Large banks have compliance departments that can absorb MiCA requirements across multiple parallel workstreams. The harder question is what fintech bsa aml small team operations and community banks should do when they have three compliance staff and a board pushing for crypto product expansion.

Fintech BSA AML Small Team Strategy

For a fintech bsa aml small team, MiCA compliance is achievable only if you scope your crypto exposure tightly at the start. Offering one crypto-adjacent service, crypto-backed lending or stablecoin settlement rails, for example, under an existing payment institution license is operationally very different from running a full CASP with 10 service types. Before expanding:

- Get a written legal opinion on whether your existing license covers the specific crypto activity you are planning

- Map each proposed service against MiCA's 10 defined CASP service types

- Identify which AML obligations are additive versus already covered by your payment AML program

- Decide whether to build internal compliance capability or contract a managed compliance service provider for crypto-specific functions

The manual compliance versus AI automation trade-off is particularly sharp for small teams. Manual workflows that handle 1,000 onboardings per month collapse under 10,000. Plan for automation before you hit that threshold, not after the first examination finding.

BSA AML Compliance Community Banks Roadmap

bsa aml compliance community banks entering crypto face a specific challenge: existing BSA examiners may lack crypto subject matter expertise, making exam outcomes harder to anticipate. A practical roadmap:

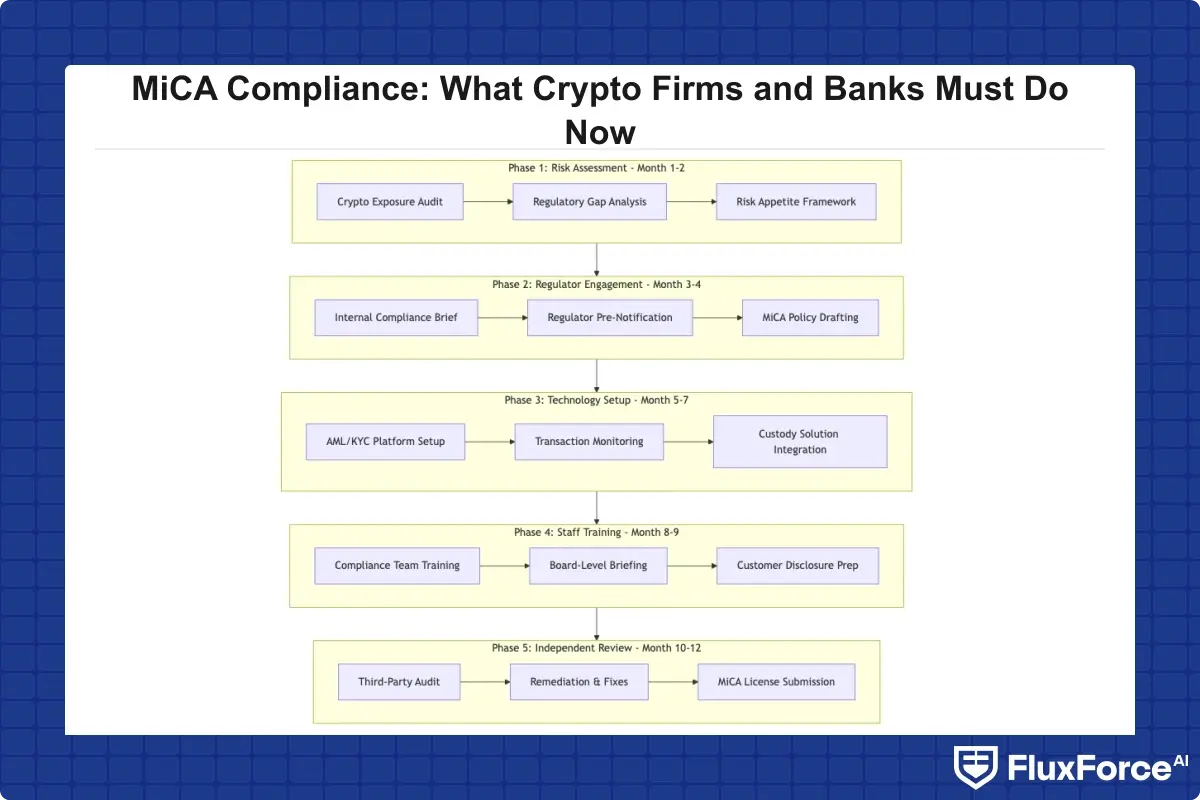

- Months 1-2: Complete a crypto risk assessment using your aml risk assessment guide adapted for digital assets. Identify which customer segments are actively requesting crypto services.

- Months 3-4: Engage your primary federal regulator proactively before filing any CASP-related documentation. Request pre-application supervisory guidance in writing.

- Months 5-6: Select and implement aml compliance software with blockchain analytics capability. Test Travel Rule data exchange workflows end-to-end before going live.

- Months 7-8: Train all BSA staff on crypto-specific typologies. Formally update your BSA program to document crypto risks and controls.

- Months 9-12: Commission an independent review of your crypto AML program before accepting the first live customer transaction.

For compliance teams also working through DORA requirements alongside crypto obligations, sequencing these two workstreams together is more efficient than treating them in isolation. DORA's ICT risk requirements overlap substantially with MiCA's operational resilience provisions. The anti money laundering technology selections you make in this roadmap should account for both frameworks' audit trail and incident reporting requirements from day one.

- MiCA (Markets in Crypto-Assets Regulation) is the EU's first comprehensive licensing and conduct framework for crypto-asset service providers (CASPs).

- MiCA compliance crypto starts with authorization, not policy.

- Strong aml compliance is the operational foundation of any MiCA authorization.

- MiCA's authorization requirements set a high bar for identity verification.

- SAR filing is where mica compliance crypto moves from paperwork to operational reality.

Onboard Customers in Seconds

Conclusion

MiCA compliance crypto is specific, not ambiguous. The regulation tells you which licenses to obtain, which aml compliance controls to implement, which kyc automation standards to meet, and which sar filing procedures to follow. Firms treating MiCA as a documentation exercise rather than an operational redesign will find gaps during NCAs' first rounds of supervisory review.

Start with your aml risk assessment. Map your crypto exposure, identify where your existing BSA/AML program has gaps, and work backward from MiCA's specific requirements to close them. The sanctions screening and identity verification capabilities that form the core of sound AML compliance do not change under MiCA, they need crypto-specific extensions applied to what you have already built.

The window for methodical preparation is still open in mid-2026. Firms that act now, before enforcement patterns become clear across EU jurisdictions, will be in a structurally stronger position than those waiting for a supervisory finding to set their timeline for them.

Share this article