.webp)

Listen To Our Podcast🎧

Introduction

Know your business KYB verification has moved from a back-office formality to a front-line risk control across every regulated sector. Corporate entities account for the majority of large-scale money laundering cases precisely because shell companies, holding structures, and nominee directors obscure who is ultimately in control. For banks, fintechs, and insurers, onboarding a business client without a rigorous KYB process is not just a compliance gap: it is an open door for financial crime. This post explains the mechanics of KYB, why it is structurally different from consumer KYC, how it feeds directly into AML compliance and SAR filing workflows, and what a practical implementation looks like for teams running lean in 2026. For aml compliance fintech environments in particular, where corporate onboarding happens at scale through automated flows, getting KYB right from day one is the difference between a defensible program and a regulatory exam finding.

- What Is Know Your Business (KYB) Verification?

- KYB vs. KYC: Why Corporate Verification Is Fundamentally Different

- How KYB Directly Supports AML Compliance

- SAR Filing, CTR Rules, and the KYB Data Chain

- AML Technology and KYB Automation in 2026

Onboard Customers in Seconds

What Is Know Your Business (KYB) Verification?

Know Your Business (KYB) verification is the process of confirming a corporate entity's legal identity, active registration status, beneficial ownership structure, and financial crime risk profile before entering into a business relationship. The goal is not simply to confirm a company exists: it is to understand who controls it, what it actually does, and whether those facts are consistent with how the entity intends to use your services.

The Legal Foundation of KYB

The requirement in the United States flows primarily from the Bank Secrecy Act and the Financial Crimes Enforcement Network (FinCEN) Customer Due Diligence rule, finalized in 2018. That rule requires covered institutions to identify and verify the beneficial owners of legal entity customers: specifically, any natural person holding 25% or more of the equity interest, plus one individual with significant managerial control over the entity.

That rule requires covered institutions to identify and verify the beneficial owners of legal entity customers: specifically, any natural person holding 25% or more of the equity interest, plus one individual with significant managerial control over the entity.

The Corporate Transparency Act, effective January 2024, extended this framework by requiring most U.S. companies to file beneficial ownership information directly with FinCEN. For compliance teams, this creates a new cross-reference data source, but it also adds a reconciliation layer: the information companies file with FinCEN must be checked against what they tell you at onboarding.

What KYB Checks Actually Cover

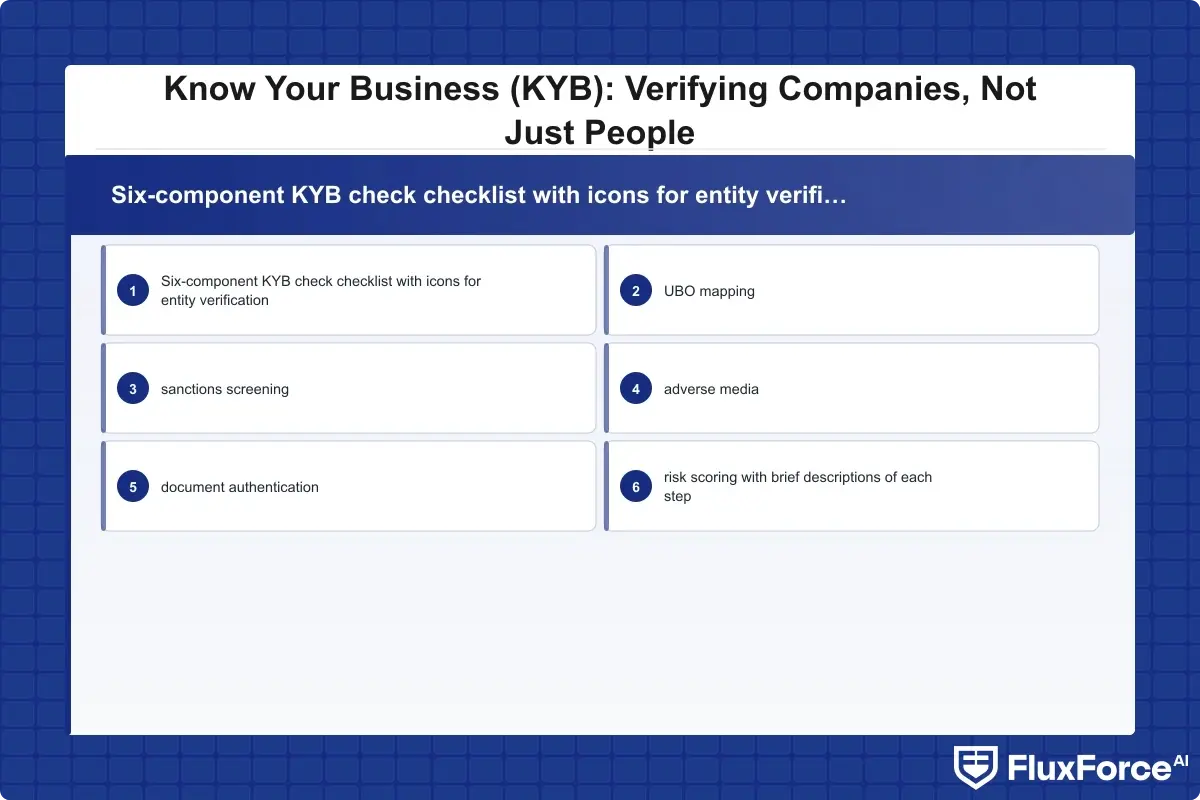

A complete KYB check for a corporate client includes six components:

- Entity verification: Confirming legal name, registration number, jurisdiction, and current active status via official company registries

- Beneficial ownership mapping: Identifying all Ultimate Beneficial Owners (UBOs) above the ownership threshold and tracing multi-layer ownership structures

- Sanctions and PEP screening: Running entity names, directors, and UBOs against OFAC, UN, EU, and other applicable sanctions lists

- Adverse media screening: Checking for negative news coverage, litigation history, regulatory actions, or reputational concerns

- Document verification: Authenticating articles of incorporation, operating agreements, and corporate documents against reliable independent sources

- Risk scoring: Assigning an initial risk tier based on industry, geography, ownership complexity, and anticipated transaction types

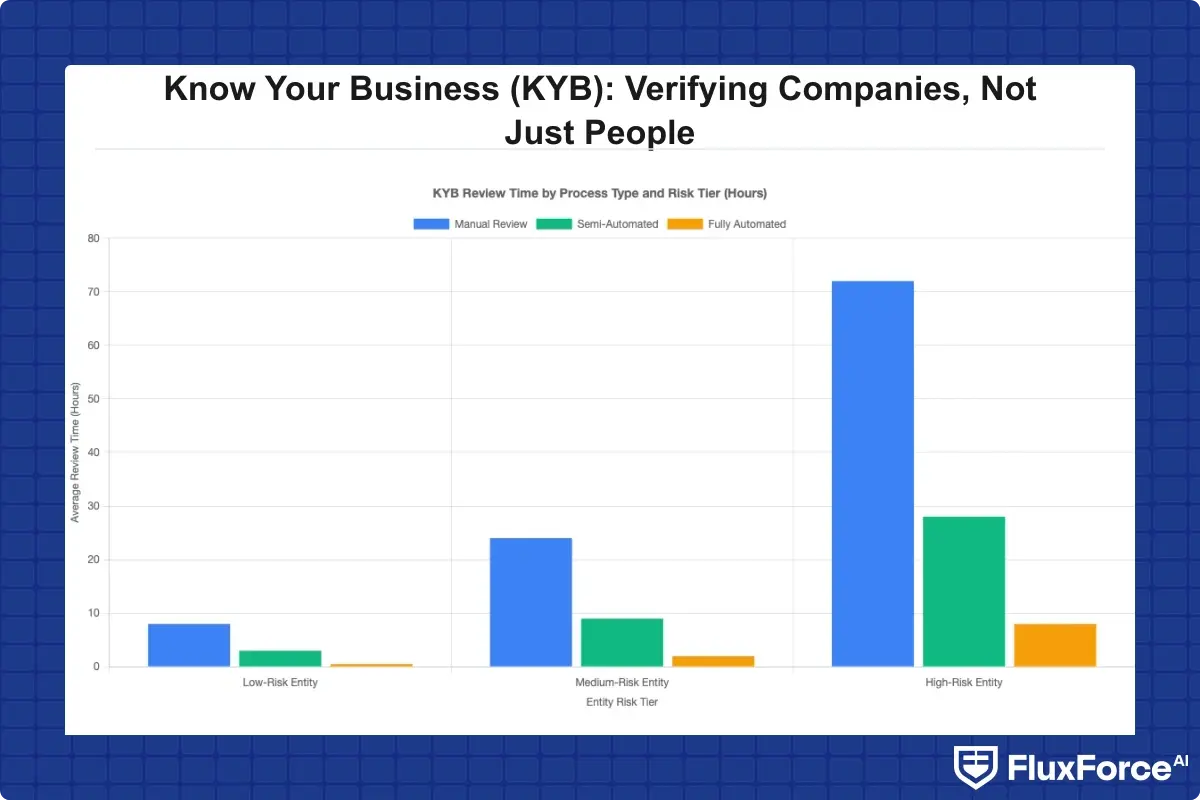

This is where kyc automation tools provide a measurable advantage. Running these checks manually for even 50 new corporate clients per month creates serious throughput and consistency problems that no compliance team can sustainably absorb.

KYB vs. KYC: Why Corporate Verification Is Fundamentally Different

Most compliance professionals have a solid grasp of consumer KYC. Corporate KYB is harder, and the reasons are structural rather than procedural.

Ownership Structures Add Layers

A natural person has one identity. A corporation can be owned by a holding company, which is owned by a trust, which names a nominee director. Tracing beneficial ownership through multi-layer structures in jurisdictions with limited public registers requires significant effort without automated tools. The Financial Action Task Force (FATF) recommends that member states maintain publicly accessible beneficial ownership registers, but implementation quality varies substantially across jurisdictions, particularly in offshore financial centers.

Beyond initial onboarding, a company's risk profile changes over time. A logistics firm that starts importing from a newly sanctioned region, or a payments provider that begins serving high-risk merchant categories, has a materially different risk profile than when it was first onboarded. Ongoing monitoring is as essential as the initial check.

KYC CDD Requirements Banks Face for Corporate Clients

Under the kyc cdd requirements banks must satisfy, corporate onboarding requires considerably more documentation than individual onboarding. Banks must collect beneficial ownership records for each entity with significant ownership stakes, verify those records against reliable independent sources, and update them when ownership changes materially. KYC automation 2026 platforms increasingly pull company registry data, UBO filings, and watchlist screening results through real-time APIs, reducing turnaround from days to minutes. For institutions managing large corporate portfolios, kyc automation is not optional: manual verification at scale introduces inconsistency and exposes the institution to BSA exam findings for documentation gaps that automated systems would have caught.

How KYB Directly Supports AML Compliance

KYB and AML compliance are inseparable in practice. Most financial crime that flows through the formal banking system uses legal entities as the vehicle, precisely because corporate structures obscure ultimate control. Without robust entity verification at onboarding, the entire anti-money laundering framework has a gap where it matters most.

Building an AML Risk Assessment at Onboarding

A practical aml risk assessment guide approach assigns each corporate client a risk tier based on four factors: industry sector (high-cash or high-anonymity industries score higher), geographic presence (entities operating in FATF high-risk jurisdictions receive elevated treatment), ownership complexity (shell layers or missing UBO information raise the score), and the nature of the anticipated relationship.

The fintech bsa aml small team challenge is real: scaling manual risk assessments across hundreds of monthly corporate onboardings is not feasible without automation. AML compliance software that automates initial risk tier assignment using live registry data and screening results closes this gap directly. For organizations building or upgrading these workflows, regulatory compliance automation platforms that bundle KYB, AML screening, and ongoing entity monitoring into a unified architecture have become a standard infrastructure choice, particularly where compliance teams need to reduce false positives without adding headcount.

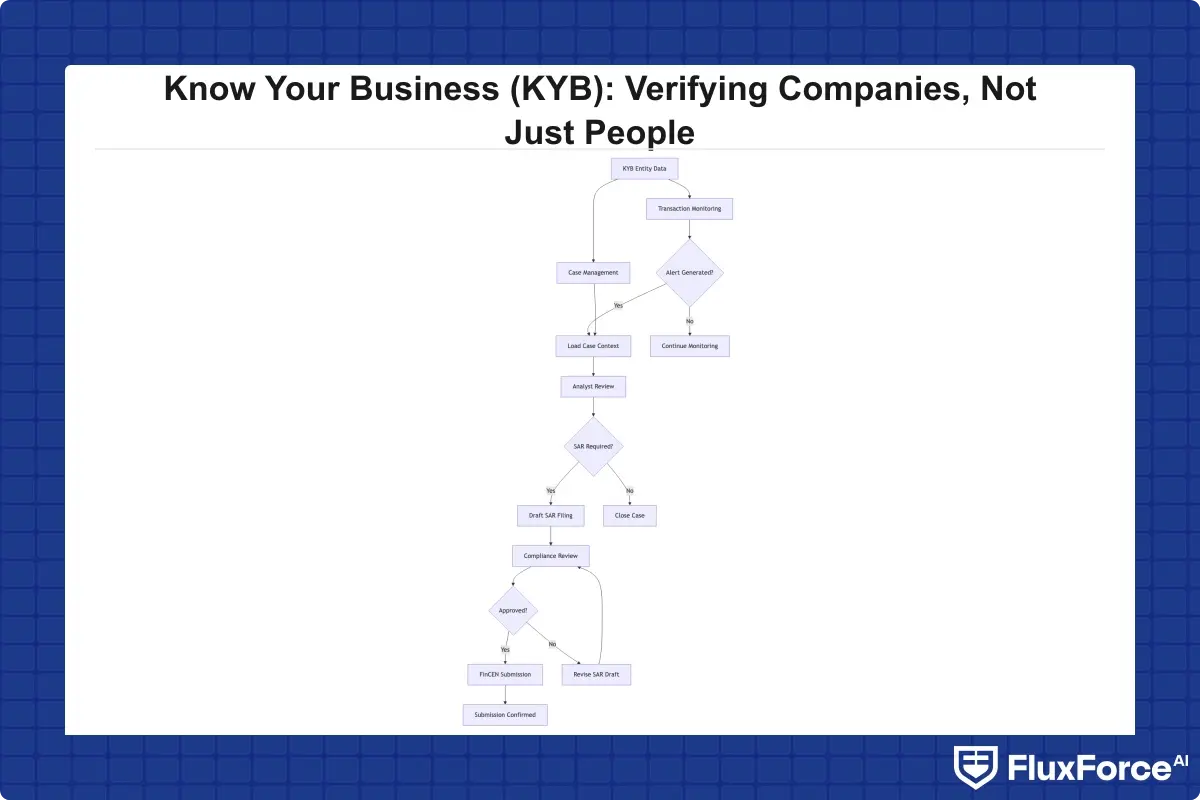

Connecting KYB to SAR Filing

A well-structured suspicious activity report guide will tell you that SAR filings begin with a transaction pattern that does not match the customer's stated business purpose. That mismatch is only detectable if the compliance function understood the business purpose at onboarding. Poor KYB means transaction monitoring has no reliable baseline. The result is either excessive false positives (because the system has no context for what is normal for that client type) or missed suspicious activity (because thresholds were set too loosely to avoid alert fatigue). Either outcome directly degrades aml compliance quality and creates exam exposure.

SAR Filing, CTR Rules, and the KYB Data Chain

Suspicious Activity Report filing is one of the most resource-intensive compliance activities for financial institutions. Understanding how KYB data feeds into the SAR investigation process reduces both filing time and the risk of under-reporting.

How KYB Data Improves SAR Filing Efficiency

SAR filing efficiency improves measurably when investigators have complete entity context at the point of case review. If a corporate account triggers a transaction monitoring alert, the reviewing analyst needs immediate answers: Is the ownership structure fully documented? Have any named UBOs appeared in recent adverse media or sanctions updates since onboarding? Does this transaction type match the industry and geography profile captured in the KYB file?

When that context is embedded in the case management system, a SAR decision takes minutes rather than hours. Without it, the investigator re-runs KYB checks manually, introduces inconsistency between reviewers, and creates documentation gaps that regulators flag during BSA examinations. For a practical look at how automation changes the underlying detection math, the analysis in AI vs. Traditional Fraud Detection: Key Differences Every Risk Officer Should Know applies directly to entity-level SAR investigations as well.

SAR Filing Requirements in 2026

The sar filing requirements 2026 environment reflects several compounding regulatory shifts. The Anti-Money Laundering Act of 2020's phased implementation has expanded the categories of reportable activity, tightened narrative requirements, and extended mandatory filing obligations to additional institution types. Institutions now face 30-day filing windows from the date suspicious activity is detected (60 days when the suspect is unidentified), and FinCEN has signaled heightened scrutiny of narrative quality in examination cycles. Following sar filing best practices means documenting the full beneficial ownership chain in the SAR narrative for legal entity subjects, not just recording the company name and account number. Institutions that complete thorough KYB at onboarding are simply better positioned to file complete, defensible SARs because the ownership data already exists in structured form.

CTR Filing Rules and Corporate Accounts

CTR filing rules for corporate accounts differ from consumer accounts in one important respect: corporate clients often handle high transaction volumes as a routine part of operations. A manufacturing company depositing large cash proceeds from a trade show may require a Currency Transaction Report, but that does not make the transaction suspicious. CTR exemptions are available for certain qualifying business customers with established cash-handling patterns, but granting those exemptions correctly depends on having solid KYB documentation on file. The bsa aml compliance checklist for community banks should include a dedicated section for corporate CTR exemption decisions, with each determination linked directly to the KYB file for the eligible client so examiners can trace the basis for the exemption.

AML Technology and KYB Automation in 2026

Anti money laundering technology 2026 is shaped by three shifts that compliance and technology teams both need to track closely.

AI-Driven Entity Resolution

Modern anti money laundering technology platforms use AI-driven entity resolution to match company names across different data sources, handling transliterations, name variations, and alternative corporate structures that rule-based systems miss entirely. For KYB, this capability matters when verifying entities with names registered differently across jurisdictions, or when cross-referencing directors against PEP databases that use different naming conventions. These improvements make kyc automation 2026 solutions fundamentally different from the static watchlist screening tools of five years ago: the system understands entity context and relationship patterns, not just name string matches.

Graph-Based UBO Mapping

Graph databases have become the standard architecture for modeling corporate ownership structures in KYB platforms. Rather than storing ownership as a flat list of shareholders, a graph model represents each ownership relationship as an edge between nodes, enabling automated traversal of multi-layer chains and calculation of effective ownership percentages through complex holding structures. This approach surfaces circular ownership, cross-shareholdings, and other indicators of intentional obfuscation that flat-file database systems cannot reliably detect.

The EU AI Act and KYB Systems

EU AI act financial services implications are now a practical consideration for any KYB platform selection in 2026. Under the EU AI Act, which entered into force in 2024 with a phased implementation timeline, high-risk AI systems used in customer due diligence and credit-related decisions must meet explainability and human oversight requirements. AML compliance software operating in EU markets cannot function as a black box: risk scores must be traceable, model logic must be auditable, and human review must be integrated into the decision workflow for elevated-risk determinations. For procurement teams evaluating KYB tools, EU AI Act conformance is a specification requirement today, not a future roadmap consideration.

KYB for Community Banks and Fintechs: The Practical Gap

BSA AML compliance community banks face a different problem from large institutions. Technology budgets are smaller, compliance teams run leaner, and the regulatory expectations are identical. Getting KYB right on a constrained budget requires a clear process before any software decision.

The BSA AML Compliance Checklist for Small Teams

A practical bsa aml compliance checklist for community banks and small fintechs running the fintech bsa aml small team model covers six core elements:

- Define minimum KYB documentation requirements for each client risk tier (low, medium, high)

- Establish a data source hierarchy for verification: official company registry first, then licensed third-party data providers, then client-provided documents as a last resort

- Map beneficial ownership collection requirements to Corporate Transparency Act reporting thresholds

- Set KYB refresh intervals by risk tier: annually for low-risk clients, more frequently for elevated-risk relationships

- Configure automatic refresh triggers for material events: change of control, entry into a newly sanctioned geography, or an adverse media alert on a named UBO

- Link KYB risk scores directly to transaction monitoring alert thresholds so higher-risk entities face proportionally lower detection thresholds

The aml compliance fintech environment adds a specific constraint: fintechs often onboard corporate clients through automated API flows at scale. KYB checks must be low-latency and fully automated for the initial screening tier, with human review reserved for edge cases and elevated-risk escalations that genuinely require analyst judgment.

Enhanced Due Diligence for High-Risk Entities

The enhanced due diligence guide principle for corporate clients is straightforward: higher risk requires deeper verification and closer ongoing monitoring. For legal entity clients flagged as high-risk at onboarding, EDD typically involves source of funds documentation for the entity itself, direct verification contact with beneficial owners, review of audited financial statements, and reduced alert thresholds in transaction monitoring.

EDD is not a one-time event. It should be triggered automatically whenever a client's risk tier changes materially: if a UBO becomes a politically exposed person following an election, if the company enters a new high-risk sector, or if adverse media surfaces after initial onboarding. For organizations that already handle KYC and AML identity verification for high-risk counterparties, the same EDD framework applies directly to corporate banking clients with elevated ownership complexity or cross-border operating structures.

KYB in Supply Chain and Insurance

KYB obligations extend well beyond banking and fintech. Insurance underwriters and supply chain finance teams face the same fundamental need: understanding who is behind a corporate counterparty before accepting risk or extending credit.

KYB in Trade Finance and Insurance

For insurers, beneficial ownership visibility matters at the underwriting stage. A commercial policy covering a logistics firm that turns out to be majority-owned by a sanctioned individual creates significant regulatory and financial liability. AML risk checks in policy issuance for compliance officers in insurance require the same depth of entity verification that banking onboarding demands, particularly for large commercial policies or clients operating across multiple jurisdictions.

Supply chain finance introduces additional complexity because counterparties span multiple regulatory environments with inconsistent corporate registry quality. The principles driving cross-border trade compliance for high-risk supply chains require compliance teams to verify not just the direct counterparty but also key sub-suppliers in elevated-risk regions. KYB tools that integrate with global company registers and sanctions databases have become standard infrastructure for procurement and trade finance teams managing high-value supplier relationships. The aml compliance fintech principles around automated ongoing monitoring apply equally in these non-banking contexts, since the underlying risk (obscured beneficial ownership, sanctioned principals) is identical.

- Know Your Business (KYB) verification is the process of confirming a corporate entity's legal identity, active registration status, beneficial ownership structure, and financial crime risk profile before entering into a business relationship.

- Most compliance professionals have a solid grasp of consumer KYC.

- KYB and AML compliance are inseparable in practice.

- Suspicious Activity Report filing is one of the most resource-intensive compliance activities for financial institutions.

- Anti money laundering technology 2026 is shaped by three shifts that compliance and technology teams both need to track closely.

Onboard Customers in Seconds

Conclusion

Know your business KYB verification is the compliance function that makes everything else work properly. Without verified entity data at onboarding, transaction monitoring generates noise, SAR filings lack the context investigators need, and the entire aml compliance architecture rests on an incomplete foundation. The technical tools have improved substantially: AI-driven entity resolution, graph-based UBO mapping, and automated refresh triggers mean a KYB program that once required weeks of analyst time can now run in hours with the right platform.

If you are building or upgrading a KYB program, start with the risk-tiering model and work backward to data requirements. Define what enhanced due diligence looks like for your highest-risk entity clients, then automate verification for lower tiers. Institutions that invest in this foundation in 2026 will be better positioned to meet sar filing requirements, satisfy examiner expectations on BSA AML compliance, and keep false positive rates low enough that the compliance function can focus on genuine risk rather than administrative backlogs.

Share this article