.webp)

Listen To Our Podcast🎧

Introduction

The future financial crime prevention predictions taking shape for 2026-2030 point to one unavoidable conclusion: institutions that delay AI adoption will spend more, catch less, and face growing regulatory exposure. Between synthetic identity fraud reaching an estimated $6 billion in annual US losses and global AML compliance costs climbing steadily year over year, the math no longer supports incremental upgrades to legacy systems. This post lays out 10 concrete predictions grounded in current technology trajectories, regulatory signals, and the hard economics of agentic AI banking and compliance automation. Whether you are a CISO designing a five-year security roadmap or a compliance officer making the case for budget, these predictions should shape how you invest through 2030.

Between synthetic identity fraud reaching an estimated $6 billion in annual US losses and global AML compliance costs climbing steadily year over year, the math no longer supports incremental upgrades to legacy systems.

- Why These Future Financial Crime Prevention Predictions Demand Attention Now

- Predictions 1-3: Agentic AI Banking Rewrites Fraud Detection by 2027

- Predictions 4-6: The Cost of Compliance Financial Services Forces a Structural Shift

- Predictions 7-8: What Regulatory Technology Will Look Like by 2028

- Predictions 9-10: Platform Consolidation and the Future of AI in Banking

Onboard Customers in Seconds

Why These Future Financial Crime Prevention Predictions Demand Attention Now

Financial crime is growing faster than most institutions can manually detect it. The Financial Action Task Force estimates that 2-5% of global GDP is laundered annually, translating to $800 billion to $2 trillion globally. That figure has not shrunk under the prevailing model of more analysts, more rules, and more alerts. It has grown.

The problem is not effort. It is architecture. Manual compliance cost per investigation runs $40-$90 at a tier-1 bank when you factor in analyst time, case management overhead, and false positive processing. Multiply that by the millions of alerts most large institutions generate monthly, and the scale of the inefficiency is hard to ignore.

Manual compliance cost per investigation runs $40-$90 at a tier-1 bank when you factor in analyst time, case management overhead, and false positive processing.

How the Fraud Threat Environment Is Evolving

Fraudsters are adopting AI before many compliance teams are. Deepfake-based identity fraud grew 3,000% between 2022 and 2024, according to identity verification firms tracking biometric attack vectors. Synthetic identity schemes no longer require human mule networks. AI-generated personas can open accounts, build credit histories, and drain limits within days of creation.

Why Traditional Defenses Fall Short

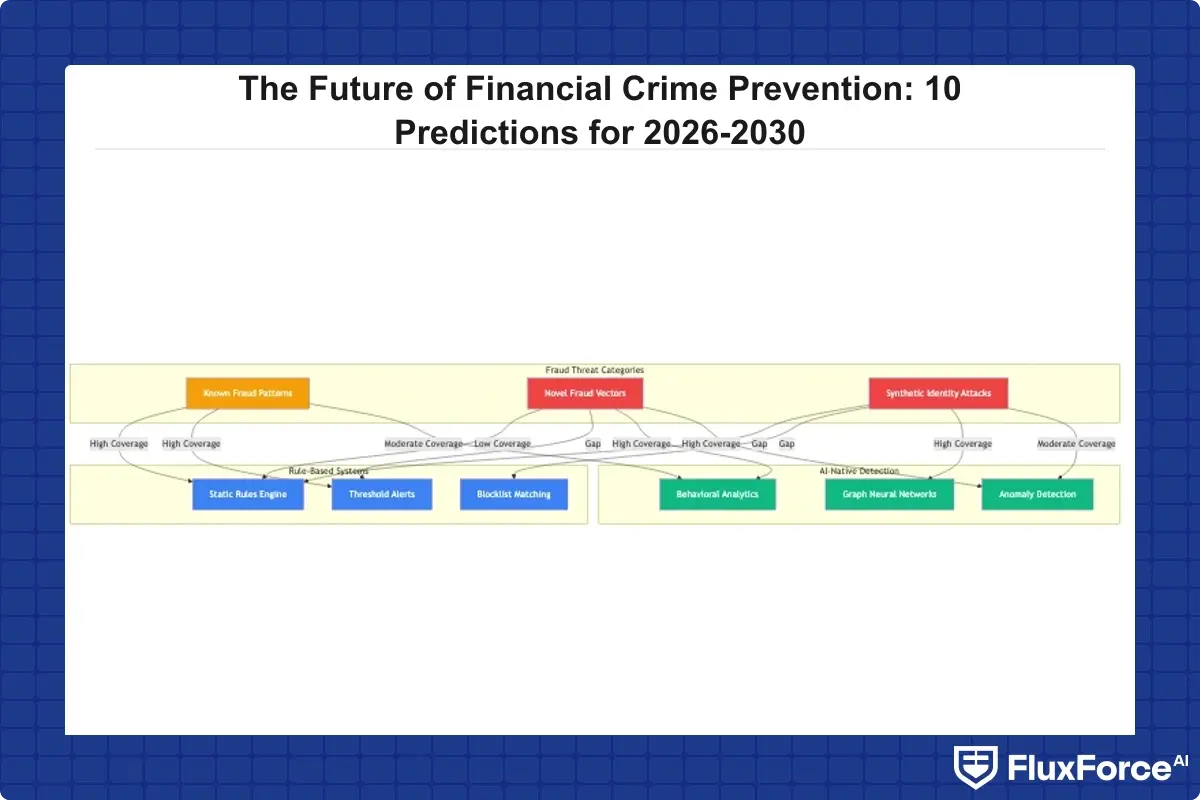

Rule-based systems catch what you have already seen. They miss novel attack patterns by design. That structural limitation, combined with false positive rates averaging 97% across legacy transaction monitoring deployments, means most alert queues are flooded with noise. Analysts burn hours processing non-events before reaching the handful of genuine threats buried in the queue. That model is not scaling into the threat environment of 2026.

That structural limitation, combined with false positive rates averaging 97% across legacy transaction monitoring deployments, means most alert queues are flooded with noise.

Predictions 1-3: Agentic AI Banking Rewrites Fraud Detection by 2027

The shift from supervised ML models to fully agentic AI financial services systems is already underway at tier-1 institutions. These three predictions address how fraud detection technology will operate by 2027 across the institutions setting the pace.

Prediction 1: Agentic AI Financial Services Automates 80% of Alert Triage

By 2027, the most advanced institutions will run agentic AI systems that autonomously triage, investigate, and resolve the majority of fraud alerts without human review. Today's best-in-class AI systems already achieve 60-70% auto-resolution on low-risk alerts. Reaching 80%+ requires full context awareness across channels: payments, identity, device behavior, and account history processed together in real time, not passed sequentially through siloed models.

How Agentic AI Fraud Agents Cut False Positives by 80% explores how multi-step reasoning agents differ from single-model ML classifiers, and why that distinction matters for institutions evaluating deployment approaches today.

Prediction 2: Real-Time Cross-Channel Fraud Correlation Becomes Standard Practice

Card fraud costs institutions billions annually, but the higher-stakes risk is multi-channel attacks where the same actor hits card, ACH, and login vectors within the same session window. By 2026, cross-channel correlation at sub-second latency will be a baseline regulatory expectation, not a competitive differentiator. Institutions still operating channel-siloed detection will face examiners asking why their systems could not connect the dots.

Our AI-powered card fraud analytics and detection strategy covers the architectural requirements for real-time multi-stream detection, including the data model changes required before any AI layer can operate at speed.

Prediction 3: AI Automation in Banking Displaces Rule-Only Detection Systems

Rule-only systems will not disappear overnight. By 2028, though, no major financial institution will run a rule-only stack as its primary detection layer. The competitive and regulatory pressure is too strong. AI automation banking gives teams the ability to adapt detection logic in near real-time rather than waiting weeks for rule update cycles. Institutions still running 2019-era rule libraries in 2026 will face a rebuild that is harder and more expensive the longer it gets deferred.

Predictions 4-6: The Cost of Compliance Financial Services Forces a Structural Shift

The compliance cost problem is well documented. According to McKinsey's financial services research, compliance costs have grown at roughly twice the rate of banking revenue over the past decade, with no sign of the gap closing under the current manual-first model. These three predictions address what happens when that cost trajectory becomes strategically untenable for boards.

Prediction 4: Manual Compliance Cost Becomes the Budget Line Boards Can No Longer Ignore

Through 2026, CFOs at mid-size and large institutions will increasingly model the total cost of manual compliance against the total cost of ownership fraud platform alternatives. Manual compliance costs scale linearly with headcount: hire more analysts to handle more alerts. AI platforms scale non-linearly: the marginal cost of processing 10x more alerts on a properly configured system approaches zero once the platform is deployed and calibrated.

The full comparison between manual compliance and AI automation approaches illustrates the cost divergence clearly once volume thresholds are crossed. The numbers favor automation decisively above roughly 500,000 alerts per month at a mid-size institution.

Prediction 5: Compliance Automation ROI Clears the Board-Level Business Case Hurdle

Compliance automation ROI has been difficult to quantify credibly because it requires baseline data most institutions do not track well: cost per alert, analyst FTE ratios, false positive processing time. That is changing. By 2026, standardized ROI frameworks from industry bodies and technology vendors will make it possible to model cost savings, false positive reduction, and regulatory exposure reduction on a single scorecard. FluxForce AI, for example, provides pre-built ROI templates that compliance teams use to build internal business cases, cutting the time from vendor evaluation to executive approval from months to weeks. Published FluxForce reviews from enterprise compliance teams consistently highlight these templates as the highest-value part of the initial engagement, ahead of the technology features themselves.

Prediction 6: Total Cost of Ownership for Fraud Platforms Drops 40-60% by 2028

Cloud-native deployment, shared infrastructure, and modular pricing are already compressing the total cost of ownership fraud platform market. By 2028, a tier-1 capable fraud intelligence platform will be within budget reach of regional banks and fintechs currently relying on vendor-managed shared models. This shift will change competitive dynamics significantly: institutions that once could not afford enterprise fraud infrastructure will operate at near-parity with institutions three times their size.

Predictions 7-8: What Regulatory Technology Will Look Like by 2028

Regulators have been watching AI adoption in financial services with interest and increasing specificity. These two predictions address where the regulatory environment is heading based on signals from the Basel Committee, FATF, and major national regulators across the EU, UK, and US.

Prediction 7: Regulators Will Mandate Explainable AI Models for Adverse Decisions

The Basel Committee on Banking Supervision has been clear that AI systems making decisions affecting customer accounts must be explainable and auditable. By 2027, expect formal mandates in the EU and UK requiring institutions to document model reasoning for any adverse decision. This makes explainable AI a compliance requirement, not just a best practice. Institutions investing in XAI-ready platforms today are buying a regulatory head start worth 12-18 months. Those still running black-box models will face a costly retroactive transparency project when the mandates land.

Prediction 8: Cross-Border AML Frameworks Converge on AI-Native Standards

The current patchwork of AML reporting standards across jurisdictions creates compliance arbitrage opportunities for sophisticated criminal networks. By 2028-2029, expect significant harmonization effort from FATF and regional bodies to align on AI-native transaction monitoring standards. This will simplify cross-border compliance for multinational banks while raising the minimum threshold for institutions currently operating below the emerging baseline.

Institutions already navigating cross-border trade compliance automation understand this complexity firsthand. AI-native platforms built for multi-jurisdiction workflows will be far better positioned when those standards converge and less-prepared institutions face urgent retrofit projects.

Predictions 9-10: Platform Consolidation and the Future of AI in Banking

The final two predictions address market structure and the long-term operating model for financial crime prevention technology as the industry moves through 2030.

Prediction 9: Vendor Consolidation Resets the Fraud Prevention ROI Equation

Financial institutions currently manage an average of 7-12 point solutions for fraud and compliance: separate tools for transaction monitoring, KYC, sanctions screening, case management, and regulatory reporting. By 2028, the market will consolidate around unified platforms. Fraud prevention ROI improves significantly when case data, model outputs, and workflow automation share a single system rather than requiring custom integrations across siloed tools. Institutions investing in core banking modernization as a unified architecture rather than a patchwork of point solutions will see the strongest returns as this consolidation plays out.

Prediction 10: Self-Healing Compliance Systems Emerge by 2030

The most ambitious prediction in this set: by 2030, leading institutions will operate compliance systems that automatically detect regulatory changes, assess the gap against current controls, generate remediation recommendations, and deploy configuration updates without manual process redesign. The building blocks exist today in agentic AI systems combining document understanding, multi-step reasoning, and workflow automation. Connecting them into a closed operational loop is the key engineering challenge of the next five years.

Deploying regulatory compliance agents in 90 days outlines the deployment path that gets institutions meaningfully close to this capability faster than most teams expect.

AI in Banking Hype vs Reality: What Risk Officers Should Actually Track

The future of AI in banking is real, but timeline matters more than the technology itself. The most common mistake in financial technology roadmapping is confusing capability demonstrations in controlled environments with production readiness at scale. AI in banking hype vs reality follows the pattern every technology adoption cycle does: early adopters prove the concept, mainstream uptake happens faster than skeptics predicted but slower than vendors claimed.

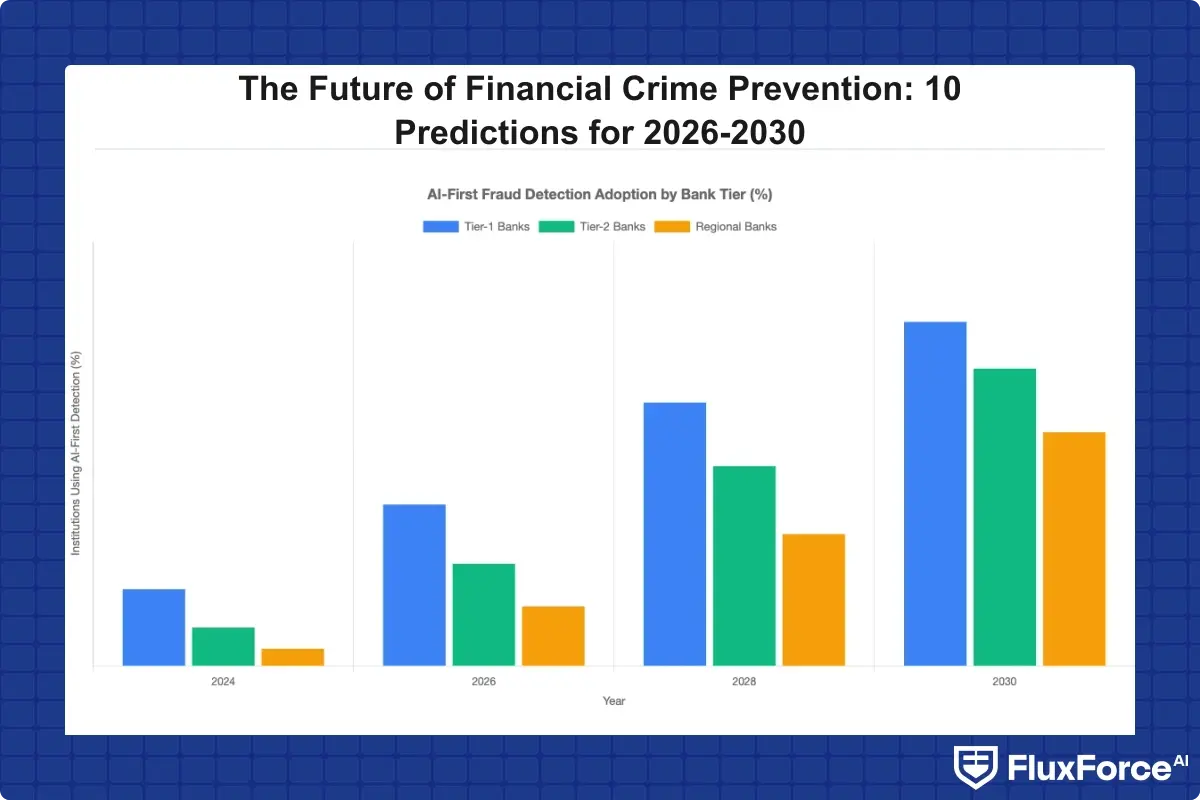

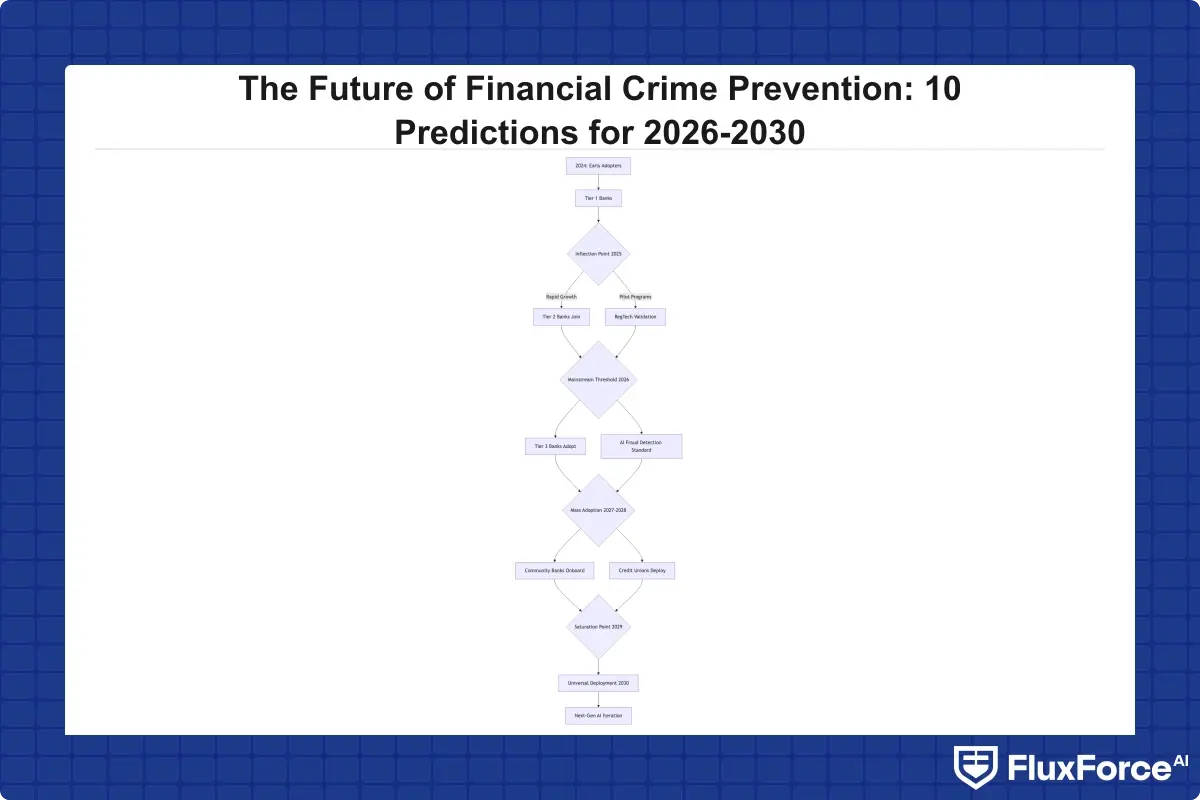

Here is what the state of ai in banking 2026 actually looks like across tiers: large tier-1 banks have deployed AI models in transaction monitoring production environments. Agentic AI banking pilots are live at roughly 20-30 major global institutions. The majority of mid-market banks are evaluating rather than deploying. Community banks are largely observing. A common theme across FluxForce AI reviews and independent competitive evaluations is that institutions consistently underestimate the data preparation required before any platform can perform at advertised benchmarks. Clean, unified entity data is the prerequisite no vendor prominently advertises.

The gap between what is technically proven and what is operationally deployed today is approximately 2-3 years. The predictions in this post reflect that lag: what tier-1 production environments are running today reaches mid-market deployment by 2027-2028.

How Should Institutions Prepare for These Future Financial Crime Prevention Shifts?

Knowing what is coming is useful. Acting on it before the curve peaks is the strategic advantage. A few concrete actions institutions can take now:

Start with data infrastructure. Every prediction in this list depends on clean, unified data. Institutions running fragmented data lakes with inconsistent entity resolution will struggle to deploy AI effectively regardless of which platform they select. Fix the data model before buying the AI layer.

Pilot agentic AI on a bounded use case. Alert triage is the ideal first deployment: measurable outcomes, clear fraud prevention ROI, and limited blast radius if the system makes an error. Getting a team familiar with how agentic systems behave in production is worth more than months of additional vendor evaluation.

Model total cost of ownership now. The cost comparison between scaling analyst headcount and scaling AI becomes more favorable to AI the longer it runs across a 3-5 year horizon. Run the numbers against your current alert volume and cost-per-alert baseline before the next budget cycle.

Engage regulators early on AI governance. Institutions participating in regulatory sandboxes and consultation processes around AI in financial services are better positioned to shape reasonable standards than those that wait and react after mandates are finalized. This is particularly pressing for institutions facing new DORA obligations or expanding sanctions screening requirements arriving through 2026.

- Financial crime is growing faster than most institutions can manually detect it.

- The shift from supervised ML models to fully agentic AI financial services systems is already underway at tier-1 institutions.

- The compliance cost problem is well documented.

- Regulators have been watching AI adoption in financial services with interest and increasing specificity.

- The final two predictions address market structure and the long-term operating model for financial crime prevention technology as the industry moves through 2030.

Onboard Customers in Seconds

Conclusion

The future financial crime prevention predictions through 2030 converge on one direction: AI-native platforms, agentic automation, and consolidated technology stacks will define the competitive and compliance frontier. Institutions that invest now in ai automation banking infrastructure, unified data foundations, and AI governance frameworks will process more alerts at lower cost, catch more genuine threats, and satisfy regulators with less friction. Those treating this period as a watch-and-wait phase will face a more expensive catch-up by 2027-2028, when platform switching costs peak and competitive gaps become visible to customers and examiners alike. The technology is proven. The business case is quantifiable with today's data. The variable that remains is execution speed.

Share this article