.webp)

Listen To Our Podcast🎧

Introduction

The eu amla anti money laundering authority represents the most significant restructuring of European financial crime oversight in a generation. Established under EU Regulation 2024/1620, AMLA takes direct supervisory control over the highest-risk financial institutions across the EU starting in 2026, replacing a fragmented patchwork of national supervisors that allowed compliance gaps to persist for years.

Established under EU Regulation 2024/1620, AMLA takes direct supervisory control over the highest-risk financial institutions across the EU starting in 2026, replacing a fragmented patchwork of national supervisors that allowed compliance gaps to persist for years.

For compliance officers, risk heads, and operations teams, this isn't a distant policy update. It's an operational shift that touches how you onboard customers, conduct aml compliance reviews, file suspicious activity reports, and run automated KYC checks. The rules are more specific than what preceded them, but the expectations are significantly higher. This guide breaks down what's actually changing, when it takes effect, and how banks of every size should be preparing right now.

- What Is the EU AMLA and Why Does It Exist?

- AMLA's Timeline and Key Milestones for Banks in 2026

- How AMLA Changes AML Compliance Obligations for Banks

- KYC and CDD Requirements Under the New AMLA Framework

- SAR Filing and Transaction Reporting Under AMLA

Onboard Customers in Seconds

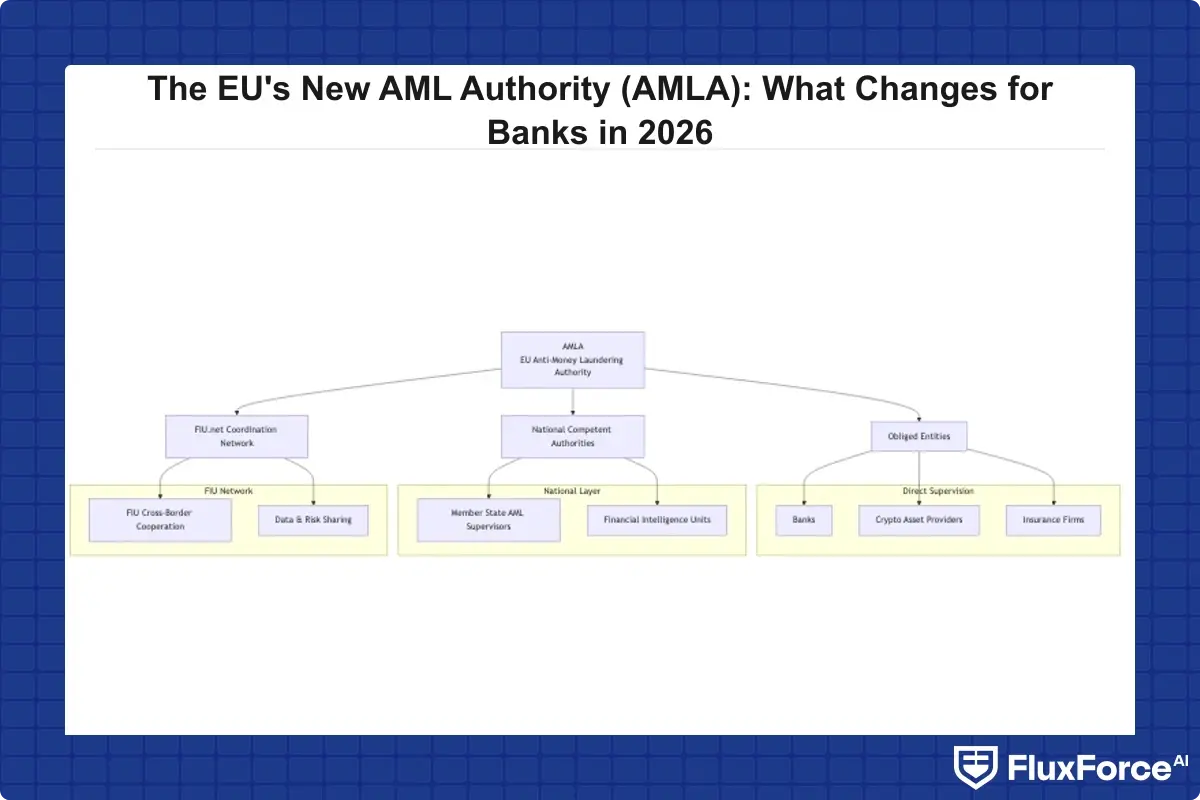

What Is the EU AMLA and Why Does It Exist?

The eu amla anti money laundering authority is a new EU-level supervisory body headquartered in Frankfurt, created to address a structural problem: national regulators across member states were inconsistently applying anti money laundering rules, and cross-border financial crime was exploiting those gaps.

The Problem AMLA Was Built to Solve

Before AMLA, AML supervision in Europe was fragmented across 27 national competent authorities, each with different enforcement cultures, resources, and interpretations of FATF recommendations. Major financial scandals at Danske Bank, Wirecard, and Pilatus Bank exposed how badly the existing model was failing. Cross-border structuring, trade-based money laundering, and crypto-facilitated flows were all falling through supervisory cracks that national FIUs couldn't coordinate to close.

AMLA changes this by creating a single rulebook and a single supervisor for the riskiest institutions. It operates alongside the 6th Anti-Money Laundering Directive (AMLD6) and the EU AML Regulation (AMLR), which establish the substantive rules AMLA will enforce.

What AMLA Is Actually Authorized to Do

AMLA's supervisory powers include:

- Direct supervision of selected obliged entities, initially up to 40 cross-border institutions

- Coordination of national supervisors through a joint supervisory mechanism

- Binding technical standards on beneficial ownership, risk scoring, and transaction monitoring

- Investigation and sanction powers including fines up to 10% of annual turnover or €10 million

This is meaningfully different from the European Banking Authority's previous AML coordination role. EBA had soft guidance powers; AMLA has hard enforcement teeth and direct access to institution-level data.

AMLA's Timeline and Key Milestones for Banks in 2026

Understanding what's happening when is the first step to building a credible response plan.

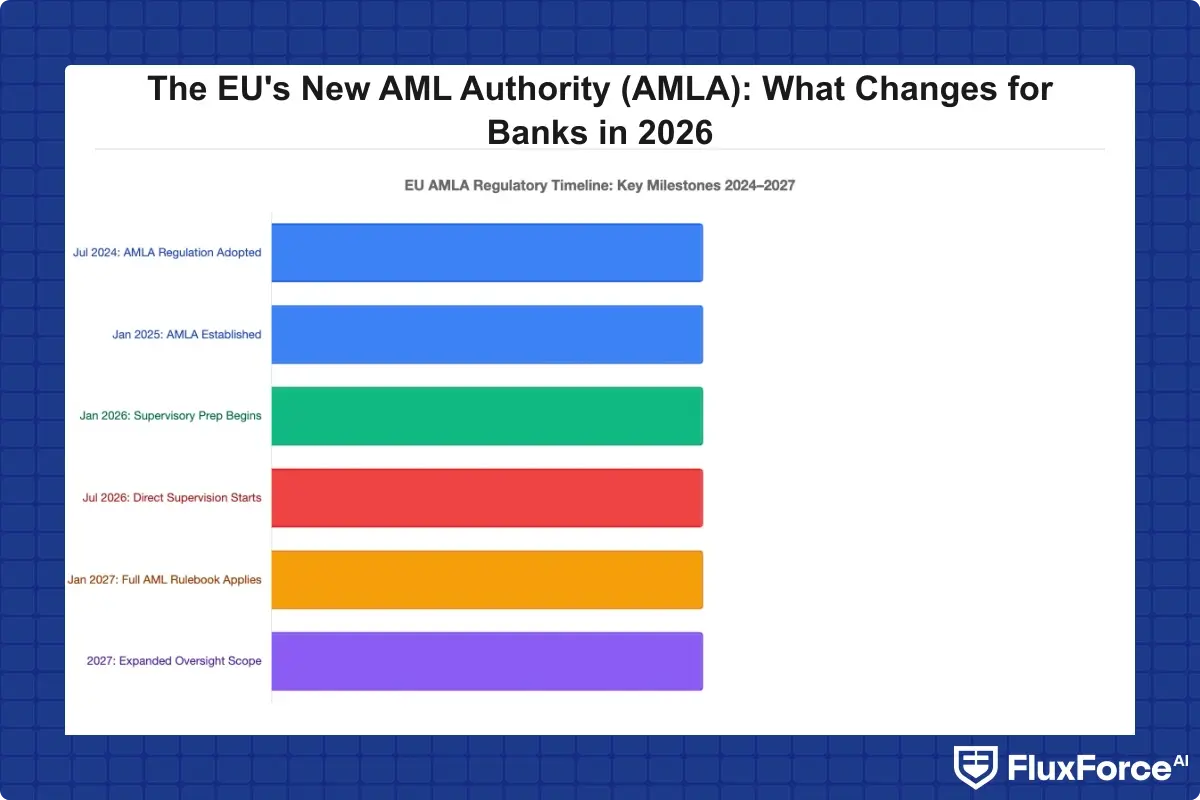

Key AMLA Deadlines: 2024 to 2027

| Milestone | Date |

|---|---|

| AMLA Regulation enters into force | July 2024 |

| AMLA becomes operational (staff, premises) | Early 2025 |

| First selection of directly supervised entities | Mid-2025 |

| Direct supervision begins | July 1, 2026 |

| Full AMLR application across member states | 2027 |

The July 2026 date is the most operationally significant. That's when AMLA assumes direct supervisory responsibility for the initial cohort of obliged entities. Banks selected for direct supervision face a transition period in 2025-2026 to bring their aml compliance programs into alignment with AMLA's technical standards.

Who Gets Directly Supervised?

AMLA's initial focus covers institutions that operate in at least 6 EU member states and are classified as high-risk based on transaction volumes, customer risk profiles, and prior compliance findings. This includes credit institutions, payment institutions, crypto-asset service providers, and certain life insurance entities.

If your institution doesn't qualify for direct supervision, indirect effects still reach you. AMLA sets the standards that national supervisors must apply consistently across all obliged entities. For smaller institutions, the question isn't whether AMLA affects you. It's how fast national supervisors converge to AMLA's standards in their own examination cycles.

How AMLA Changes AML Compliance Obligations for Banks

AMLA doesn't just create a new supervisor. It introduces substantive changes to what banks must do, documented in the AMLR and AMLD6.

AMLA doesn't just create a new supervisor.

The Single Rulebook Effect on AML Compliance

Before, a bank operating in Germany and Spain could face different interpretations of adequate transaction monitoring thresholds. The single rulebook eliminates that ambiguity. The AMLR establishes directly applicable, binding obligations covering:

- Customer due diligence procedures and documentation depth

- Beneficial ownership verification and record-keeping timelines

- PEP treatment, screening frequency, and periodic review cycles

- Enhanced due diligence triggers and evidence requirements

- Internal controls structure and compliance function independence

For institutions already running strong aml compliance programs, much of this is familiar territory. The difference is enforcement consistency and the elimination of regulatory arbitrage between member states. Institutions that relied on softer national supervision will face the sharpest adjustment.

Enhanced Risk Assessment Obligations

AMLA places significant weight on risk-based approaches grounded in documented evidence. Your aml risk assessment guide needs to reflect actual institution-specific risk factors, not a generic checklist populated once a year. AMLA's technical standards require:

- A documented methodology for customer risk scoring with explicit weightings

- Geographic risk factors mapped to specific business lines and products

- Product and channel risk assessments updated at least annually

- Integration of typologies from AMLA's central typologies database

This is a real upgrade from the informal risk assessments many institutions currently produce.

What Changes for Internal Compliance Functions

AMLA's binding technical standards specify requirements for the AML compliance function itself, including minimum qualifications for the Money Laundering Reporting Officer, independence requirements separating compliance from business lines, mandatory internal audit cycles for high-risk customer portfolios, and extended record-keeping periods of 10 years for directly supervised entities.

For teams building a bsa aml compliance checklist, these AMLA standards provide a useful framework even for non-EU institutions. They signal where global regulatory expectations are heading across jurisdictions, including the US.

KYC and CDD Requirements Under the New AMLA Framework

KYC automation becomes more critical under AMLA, not less. The AMLR codifies explicit requirements for ongoing monitoring that can't be met manually at any reasonable scale.

KYC CDD Requirements Banks Must Meet by 2026

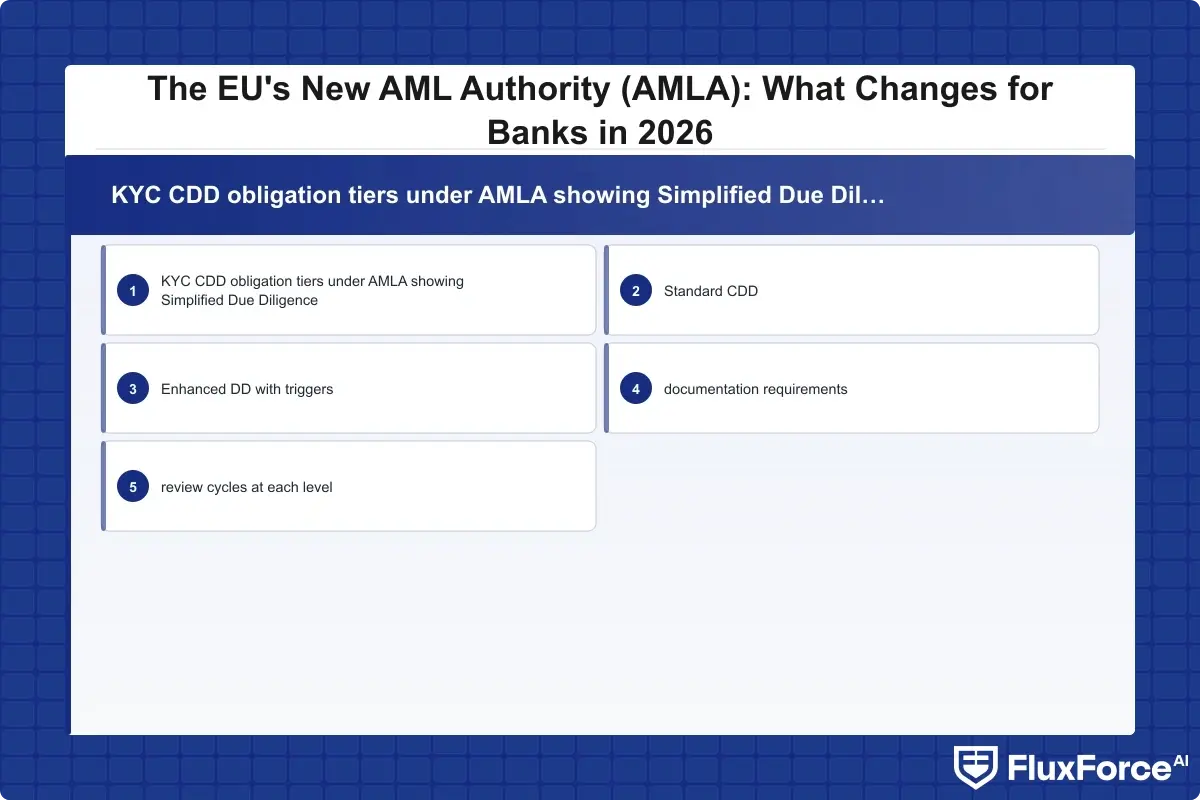

The kyc cdd requirements banks face under AMLA cover four distinct obligation layers:

- Initial CDD: Identity verification, beneficial ownership identification, and purpose-of-relationship documentation before establishing any business relationship

- Ongoing monitoring: Continuous transaction monitoring calibrated to each customer's risk profile, with documented review triggers for alerts

- Periodic review: High-risk customers reviewed at least annually; standard-risk customers every 3-5 years

- Trigger-based refresh: Any material change in customer behavior, geography, or ownership structure triggers immediate review

The periodic review requirements are new in their specificity. Previous AMLD frameworks defined "regular" monitoring loosely. AMLA gives it a concrete, auditable meaning.

Enhanced Due Diligence Guide for High-Risk Relationships

This enhanced due diligence guide covers a broader set of EDD triggers than most institutions currently apply. Under AMLA, EDD is mandatory when:

- The customer is a PEP, a family member of a PEP, or a known close associate

- The transaction involves a third country on the European Commission's high-risk list

- The relationship is conducted entirely non-face-to-face with no prior in-person verification

- The transaction is unusually large or complex without a clear economic rationale

For banks with kyc automation 2026 programs already running, the key question is whether your tools generate the documentation trail AMLA will require during examinations. Automated KYC isn't just about speed; it's about producing audit-ready evidence of every decision made.

AML screening workflows in digital lending face the same documentation pressure, and the integration patterns for automated review trails translate directly to AMLA-compliant onboarding flows.

SAR Filing and Transaction Reporting Under AMLA

Suspicious activity reporting gets a material upgrade under AMLA. The authority is building a centralized FIU.net system connecting national Financial Intelligence Units across all member states, meaning your SAR filing now has pan-European visibility and enables cross-border typology matching that wasn't possible before.

SAR Filing Requirements 2026

The sar filing requirements 2026 under AMLA introduce two changes that affect existing reporting systems:

Standardized SAR format: AMLA mandates a common template across all member states. For cross-border institutions, this simplifies operations. For banks currently using country-specific portal exports, it requires system updates before the standard becomes binding.

Tighter timelines for high-risk events: The suspicious activity report guide will require 24-hour reporting for transactions linked to terrorism financing or sanctions evasion. Standard SAR timelines remain at existing national standards until AMLA issues specific technical standards, expected in 2025.

The CTR filing rules context matters for institutions with US operations: just as FinCEN's CTR filing rules require consistent threshold application across branches, AMLA expects consistent SAR decision-making across all member states. Institutions managing both frameworks should align internal decision standards now to avoid running two separate logic systems indefinitely.

SAR Filing Best Practices for AMLA Readiness

Strong sar filing best practices under AMLA go well beyond format compliance:

- Narrative quality: AMLA guidance prioritizes factual, specific narratives that support FIU analysis. Template-heavy SARs with minimal factual detail will attract scrutiny during examinations

- Correlation to monitoring alerts: Every SAR must trace back to a specific alert with documented escalation rationale

- Consistency across segments: Institutions must demonstrate that similar patterns produce similar SAR decisions across customer types and geographies

- Volume discipline: Both systematic under-reporting and defensive over-filing create exam risks under AMLA

Good sar filing efficiency means better-quality SARs with stronger evidentiary trails, not just faster submission. The connected FIU network makes cross-border structuring detectable at the EU level for the first time, changing the risk calculus for institutions whose SAR quality has been inconsistent across jurisdictions.

The same alert-to-decision pipeline discipline that drives sanctions screening automation applies directly to AMLA-compliant SAR workflows.

AML Compliance Software and Technology Requirements

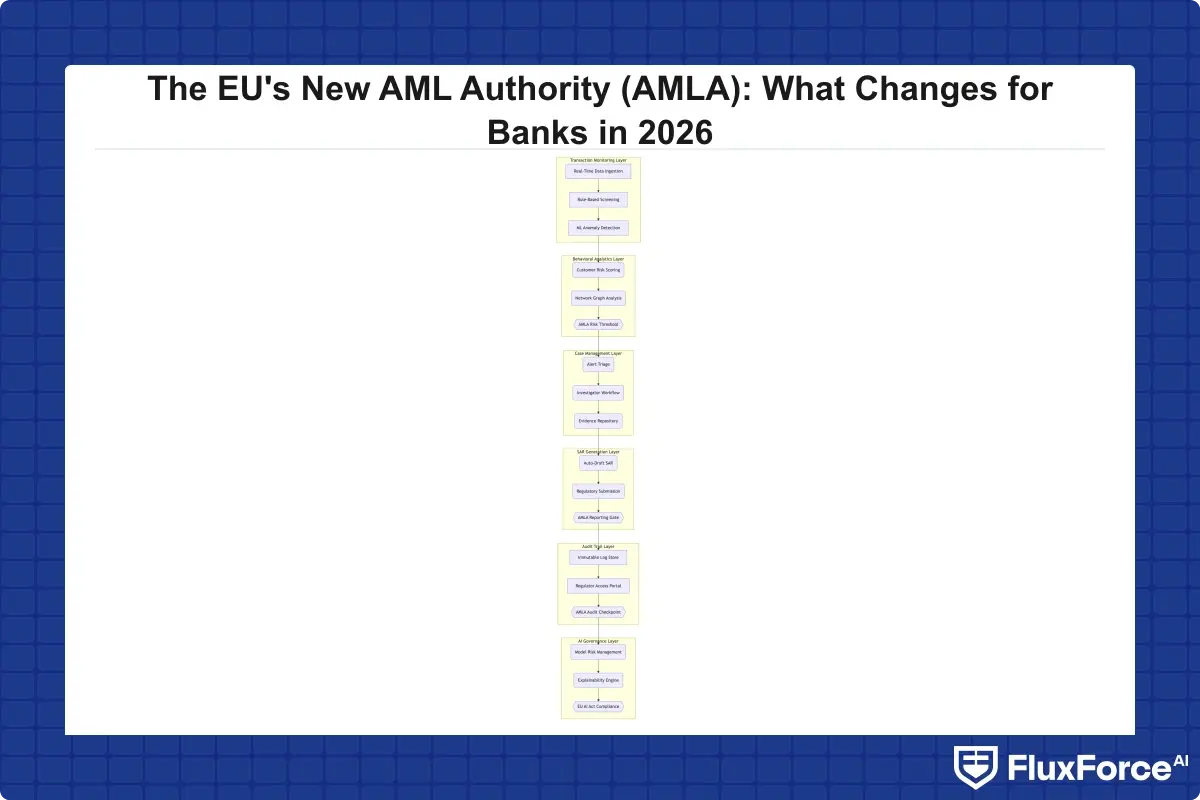

AMLA doesn't mandate specific technology, but its requirements make certain capabilities non-negotiable in practice. Anti money laundering technology 2026 must support documentation depth, auditability, and monitoring scale that manual processes cannot deliver.

AMLA doesn't mandate specific technology, but its requirements make certain capabilities non-negotiable in practice.

Core Technology Capabilities Required

Transaction monitoring at scale: AMLA's risk-based approach requires monitoring calibrated to each customer's individual profile. Rule-based systems with static thresholds fail this structurally. Banks need systems capable of behavioral baselining, dynamic threshold adjustment, and alert prioritization by risk tier.

Audit trail generation: Every compliance decision, from alert dismissal to SAR submission, requires documentation with recorded rationale. AML compliance software that doesn't generate complete, retrievable audit logs will create examination failures regardless of how experienced the underlying team is.

Regulatory reporting automation: Both CTR filing rules for US operations and AMLA-compliant SAR standardization for European operations benefit from automated report generation tied directly to monitoring outputs. Manual reporting from spreadsheets is no longer viable at the documentation depth AMLA requires.

The EU AI Act Intersection

The eu ai act financial services provisions add a compliance layer that runs in parallel with AMLA and doesn't replace it. Any AML transaction monitoring model making consequential decisions about customers qualifies as a high-risk AI system under the EU AI Act, requiring transparency, explainability, bias testing documentation, and human oversight mechanisms, independently of AMLA obligations.

Banks deploying machine learning for AML need to map their models to EU AI Act risk categories now. The two frameworks will be enforced simultaneously with no grace period for AI governance gaps.

For teams evaluating aml compliance software, the capability checklist should include model explainability outputs, bias documentation, and human override mechanisms satisfying both frameworks. Platforms built for regulatory compliance automation that address this dual-framework reality package AML enforcement with AI governance documentation in a single workflow, which reflects where the market is heading.

What Community Banks and Fintechs Need to Know About AMLA

The headlines focus on large cross-border institutions, but bsa aml compliance community banks and smaller fintech operators face real indirect effects worth planning for now.

How AMLA Affects Smaller Institutions

Smaller institutions won't face direct AMLA supervision in 2026, but two indirect pressures are immediate and concrete:

National supervisor convergence: AMLA issues binding technical standards that national supervisors must apply consistently. If your national supervisor has historically been lenient on documentation requirements or monitoring calibration specificity, that period is ending.

Correspondent banking pressure: If your institution maintains correspondent relationships with larger EU banks, those counterparts will apply AMLA-consistent due diligence to you as a respondent institution. A weak AML program creates friction in those relationships and can affect access to correspondent services.

Fintech-Specific Considerations

Aml compliance fintech requirements under AMLA deserve specific attention. Fintechs and payment institutions face the same AMLR obligations as traditional banks, without the compliance infrastructure banks have spent decades building.

The common gaps for a fintech bsa aml small team include: beneficial ownership verification gaps for business customers, adverse media screening without documented review rationale, and PEP screening that doesn't consistently cover non-obvious family and associate connections.

The practical priority order is: get KYC onboarding documentation right first, then build ongoing monitoring with documented alert rationale, then address SAR consistency. The compounding effect of AML risk gaps at customer origination creates downstream compliance problems that are harder to fix than the original gap.

The lesson from DORA compliance preparation cycles is instructive here: institutions that waited until the final months retrofitted systems under examination pressure rather than building them correctly from the start. AMLA's July 2026 deadline is closer than most compliance calendars currently reflect.

- The eu amla anti money laundering authority is a new EU-level supervisory body headquartered in Frankfurt, created to address a structural problem: national regulators across member states were inconsistently applying anti money laundering rules, and cross-border financial crime was exploiting those gaps.

- Understanding what's happening when is the first step to building a credible response plan.

- AMLA doesn't just create a new supervisor.

- KYC automation becomes more critical under AMLA, not less.

- Suspicious activity reporting gets a material upgrade under AMLA.

Onboard Customers in Seconds

Conclusion

The eu amla anti money laundering authority changes the compliance calculus for every financial institution operating in Europe. Direct supervision begins July 2026, and the preparation window that determines whether your institution is ready is closing now.

The priorities are clear: update your aml compliance program to reflect AMLA's risk-based documentation requirements, review your kyc automation tools against the new CDD timelines and EDD triggers, standardize SAR processes ahead of the common format deadline, and map your AML technology against the EU AI Act's parallel requirements. Institutions that treat this as a box-checking exercise will struggle through examinations. Those that use the AMLA transition to genuinely modernize their anti money laundering technology infrastructure will come out with a more defensible, more auditable compliance operation.

If your team is still navigating these changes manually, now is the time to evaluate how AI automation compares to manual compliance approaches for closing the gap before AMLA examiners arrive. The preparation window is open. Use it.

Share this article