.webp)

Listen To Our Podcast🎧

Introduction

The eu aml single rulebook marks the most significant shift in European financial crime enforcement since the first AML directive landed in 1991. Starting July 2027, a single, directly applicable EU regulation will govern how every bank, fintech, insurer, and payment institution across all 27 member states detects and reports money laundering, replacing the mosaic of national laws that have let criminals exploit regulatory gaps for decades. The practical difference between a directive and a regulation is enormous: no more gold-plating by individual countries, no more divergent national interpretations, and no more compliance advantage for institutions that shop for a lenient jurisdiction. For compliance officers and risk teams, the question is no longer whether to prepare, but how fast.

- What Is the EU AML Single Rulebook?

- Why Harmonisation Matters: The Cost of Regulatory Fragmentation

- Core Requirements: KYC and CDD Under the New Rules

- SAR Filing Requirements 2026 and Beyond

- AML Compliance for Fintechs Under the EU Single Rulebook

Onboard Customers in Seconds

What Is the EU AML Single Rulebook?

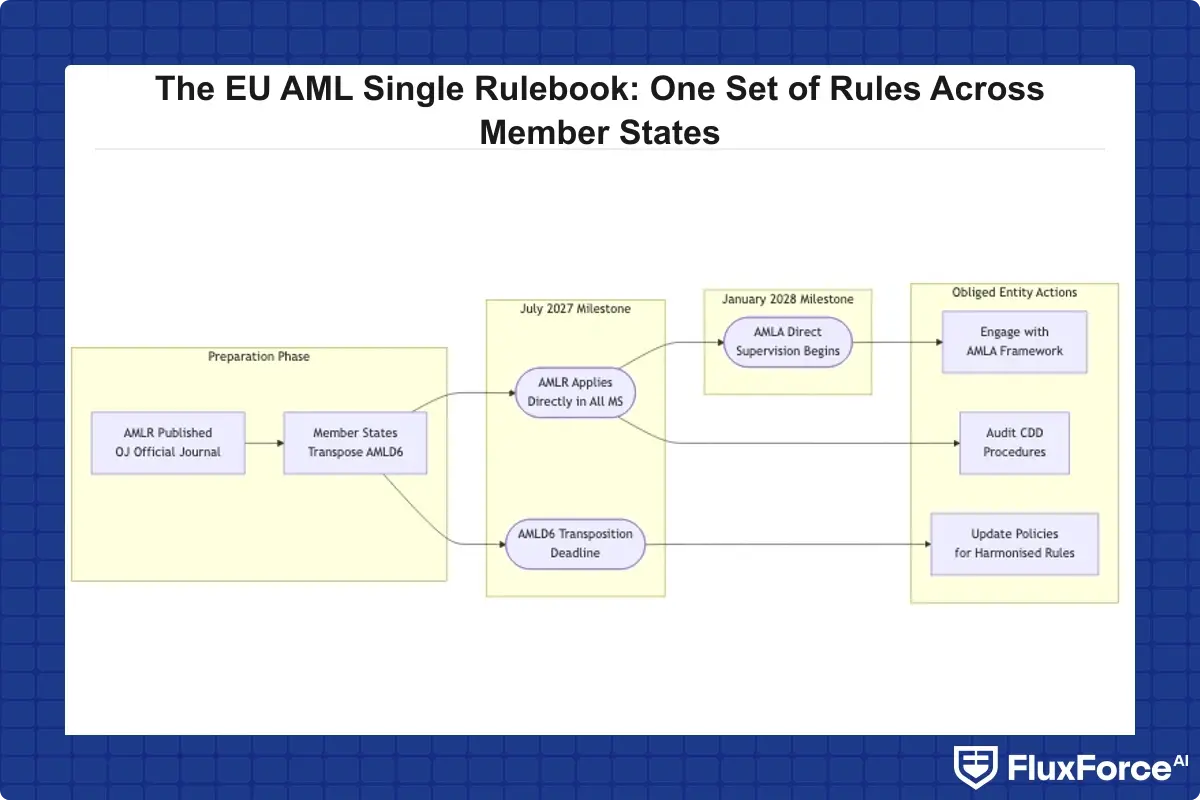

The EU AML Single Rulebook is a package of four legislative acts adopted in 2024, designed to create a true single market for financial crime prevention. The centrepiece is the AML Regulation (AMLR), published as Regulation (EU) 2024/1624, which applies directly in all member states without national transposition. Alongside it sit the sixth Anti-Money Laundering Directive (AMLD6), the regulation establishing the new European Anti-Money Laundering Authority (AMLA), and revised fund transfer rules extending crypto-asset tracing obligations to align with international standards.

The Four Pillars of the Package

The legislative package rests on four instruments working together:

- AML Regulation (AMLR): Sets directly applicable rules on customer due diligence, beneficial ownership, politically exposed persons, and internal controls. This is the single rulebook in its strictest sense.

- AMLD6: Handles member-state obligations including access to beneficial ownership registers and national FIU powers that cannot be uniformly regulated at EU level.

- AMLA Regulation: Establishes the Authority for Anti-Money Laundering, headquartered in Frankfurt, which will directly supervise the riskiest cross-border financial entities from 2028.

- Revised Funds Transfer Regulation: Extends crypto-asset transfer tracing requirements consistent with FATF Recommendation 16 Travel Rule obligations.

When Does the AMLR Apply?

The AMLR applies from 1 July 2027 for most obliged entities. AMLA begins direct supervision of selected institutions from 1 January 2028. Member states have until 10 July 2027 to transpose AMLD6. Compliance programs need to be fully operational before AMLA opens its doors, because the authority will look for institutions already running compliant systems, not ones mid-implementation.

Why Harmonisation Matters: The Cost of Regulatory Fragmentation

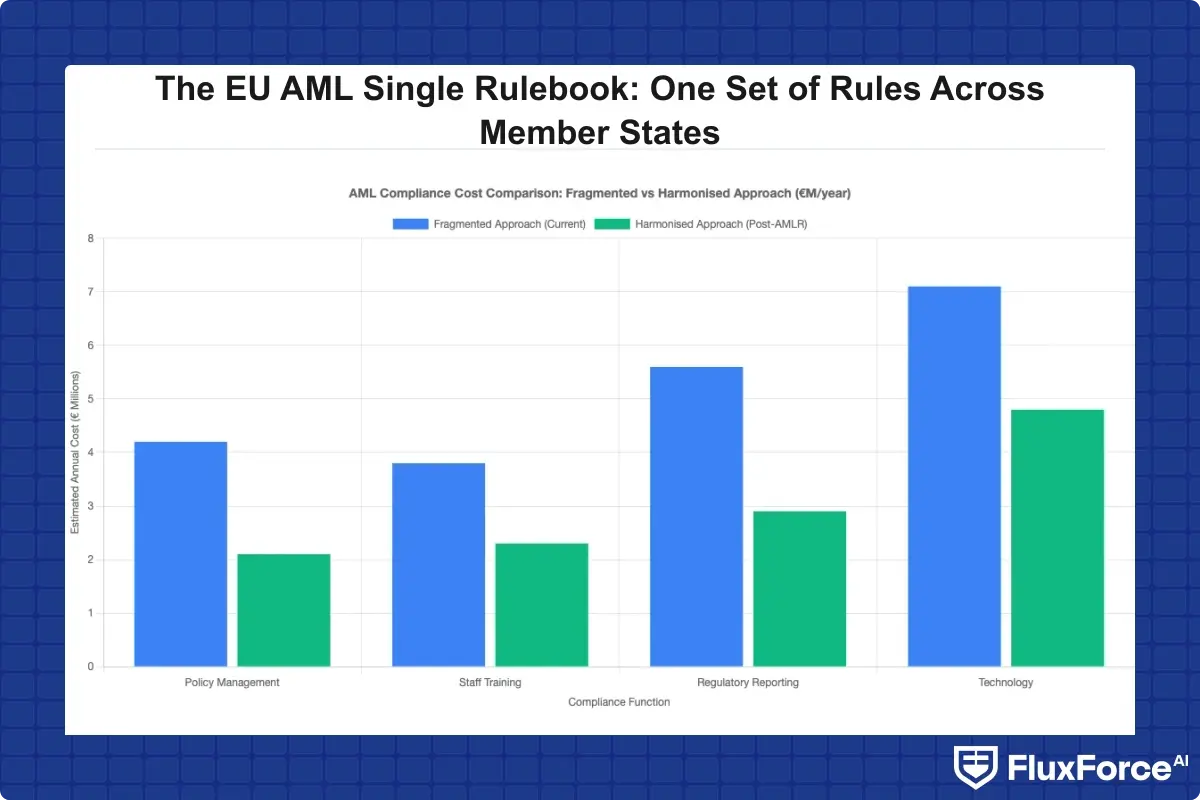

For years, EU AML rules relied on directives, which each member state transposed into national law differently. The result was at least 27 distinct compliance environments. An institution operating in Germany, the Netherlands, and Ireland was running three separate compliance programs, each with different CDD thresholds, different SAR timelines, and different beneficial ownership rules.

How Arbitrage Damaged the System

Regulatory arbitrage has been a persistent problem across the EU. The European Court of Auditors' Special Report 13/2021 found that AML supervisory quality across member states varied significantly, with some national supervisors lacking resources, independence, or clear legal powers to act effectively. Institutions with cross-border operations could exploit lighter-touch regimes in certain jurisdictions, while those operating in stricter member states faced competitive disadvantages despite identical underlying money laundering risks.

The Economic Case for a Single Rulebook

Harmonisation reduces aml compliance costs for multi-jurisdictional institutions in concrete terms. A bank with branches in eight EU countries currently needs eight sets of AML policies, eight training programs calibrated to local law, and eight different reporting formats. Under the AMLR, one policy framework, one CDD standard, and one set of sar filing rules cover the entire EU. For a fintech bsa aml small team managing compliance across multiple markets, the reduction in administrative overhead could be decisive for operational sustainability.

Core Requirements: KYC and CDD Under the New Rules

Kyc automation sits at the operational heart of the new framework. The AMLR codifies aml compliance obligations that were previously interpreted differently across member states, creating a clearer, and in some areas more demanding, baseline for all obliged entities. Getting these foundations right before July 2027 is the central challenge for compliance teams.

KYC CDD Requirements for Banks

The kyc cdd requirements banks must meet under AMLR include:

- Standard CDD for all customers before or at the start of a business relationship

- Simplified CDD only in genuinely low-risk situations, with explicit AMLR criteria defining what qualifies

- Enhanced due diligence mandatory for high-risk third countries, PEPs, correspondent banking relationships, and transactions flagged by the institution's own risk model

- Beneficial ownership verification to the 25% threshold, with member states able to lower that threshold for higher-risk sectors

The most significant change for many institutions is the prohibition on anonymous accounts and anonymous safe deposit boxes, which AMLR makes explicit across all member states. Several countries previously had carve-outs or delayed implementation. Those exceptions end in July 2027 with no grace period.

Enhanced Due Diligence Guide for PEPs and High-Risk Countries

An enhanced due diligence guide for AMLR compliance needs to address both PEP obligations and high-risk country requirements clearly. For PEPs, institutions must get senior management approval before establishing a relationship, apply enhanced ongoing monitoring, and continue EDD for at least 12 months after a person leaves a PEP position. For high-risk third countries, the EU maintains its own list separate from FATF, and EDD is mandatory with no waiver possible on the basis of long customer relationships or documented low transaction value.

Institutions that have been granting exceptions to high-risk country policies based on relationship tenure will need to review their entire affected portfolio before July 2027.

KYC Automation 2026: Getting Ready Before the Deadline

With the AMLR application date approaching, kyc automation 2026 investment decisions need to start now. The regulation raises the floor on due diligence quality while expecting institutions to apply it at scale. Manual processes that were adequate for simpler national frameworks will not survive AMLA's scrutiny. The areas where automation delivers the most value are identity verification at onboarding, ongoing transaction monitoring calibrated to customer risk profiles, and PEP and sanctions screening with real-time data feeds. For a detailed look at how AML checks integrate across identity workflows in regulated environments, AML risk checks in policy issuance covers the pattern well for institutions outside core banking.

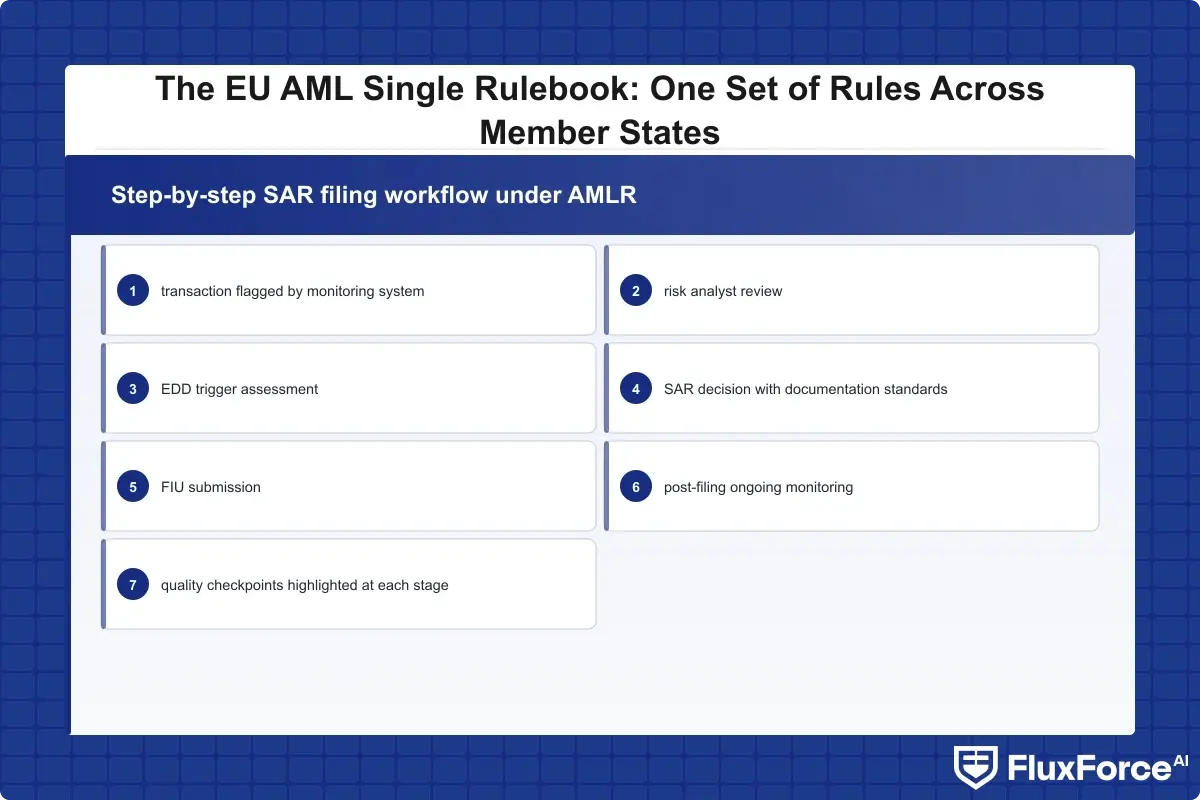

SAR Filing Requirements 2026 and Beyond

Suspicious activity report obligations are among the most technically changed areas in the AMLR. The regulation introduces a pan-EU framework for what must be reported, to which FIU, and under what quality standards. This matters significantly for cross-border institutions currently navigating inconsistent national timelines and divergent report formats.

What the AMLR Changes About SAR Filing

Current sar filing requirements vary substantially by member state. Some require reporting within 24 hours of suspicion forming; others allow several working days. The AMLR does not set a single numeric filing deadline at the regulation level, but it requires member states to publish clear, enforceable timelines and mandates that FIUs share information via FIU.net. The practical effect for institutions is that cross-border suspicious activity may increasingly flow through a single lead FIU designated for a given case, rather than requiring separate parallel reports to multiple national authorities.

SAR Filing Best Practices Under the New Framework

A thorough suspicious activity report guide for AMLR compliance needs to cover three things. First, quality over quantity: AMLA has signaled it will assess FIU efficiency partly by the quality of STRs received, so defensive mass-filing will attract scrutiny rather than provide protection. The expectation is risk-calibrated, substantiated reports backed by documented analysis. Second, tipping-off controls: AMLR clarifies that internal escalation to compliance does not constitute tipping off, which addresses a common concern among front-line staff who currently hesitate to escalate borderline cases. Third, cross-border coordination: where a transaction involves multiple member states, the institution needs a documented internal process for determining the appropriate lead FIU.

Sar filing efficiency is directly tied to the quality of your transaction monitoring technology. Institutions relying on manual monitoring will struggle to meet the report quality AMLA expects. AML screening in digital lending illustrates how automated screening reduces both false negatives and defensive over-reporting in practice.

CTR Filing Rules and the AMLR

Cash transaction reporting, governed by ctr filing rules, remains primarily a national competence under the AMLR framework. The regulation does not create a single EU cash reporting threshold, so existing national thresholds ranging from roughly €1,000 to €15,000 depending on the country remain in place. What changes is the expectation that institutions maintain consistent internal CTR processes regardless of which member state the cash transaction occurs in, and that CTR data feeds into broader AML risk assessment rather than sitting in a separate compliance silo.

AML Compliance for Fintechs Under the EU Single Rulebook

The eu aml single rulebook extends to fintechs operating in Europe more explicitly than previous directives. Crypto-asset service providers regulated under MiCA are now fully in scope as obliged entities. Payment institutions, e-money institutions, and buy-now-pay-later providers face the same CDD and reporting obligations as traditional banks, with national carve-outs that some regimes previously allowed now closed.

What Changes Most for AML Compliance Fintech

Three areas shift materially for aml compliance fintech operations under the new framework:

No more simplified onboarding by default. Some fintechs benefited from national rules allowing abbreviated KYC for low-value accounts. The AMLR tightens simplified CDD criteria and makes them explicitly risk-based. A flat "low-value product equals simplified CDD" approach will not pass AMLA review.

Beneficial ownership for corporate customers. Many fintechs have taken a lighter approach to beneficial ownership verification for SME accounts. The AMLR's 25% threshold and verification requirements apply with no sectoral exceptions for fintech business models.

The AMLR's 25% threshold and verification requirements apply with no sectoral exceptions for fintech business models.

Crypto CASPs in full scope. For crypto platforms, Travel Rule requirements and full AML obligations mean that transaction monitoring depth now needs to match a bank's wire transfer function. This represents a significant operational uplift for platforms previously operating under lighter national rules.

AML Compliance Software Selection for the New Framework

The right aml compliance software for AMLR must handle several things simultaneously: real-time sanctions screening against EU-maintained lists, risk-based customer segmentation, automated EDD triggers, and SAR workflow management. Anti money laundering technology 2026 has matured considerably, with machine-learning-based transaction monitoring now able to distinguish between genuinely suspicious patterns and high-volume legitimate activity far better than rule-based systems from five years ago. How agentic AI fraud agents cut false positives by 80% demonstrates what a well-calibrated AI monitoring system achieves in a regulated financial context.

How agentic AI fraud agents cut false positives by 80% demonstrates what a well-calibrated AI monitoring system achieves in a regulated financial context.

Key capabilities to evaluate in any anti money laundering technology shortlist for AMLR readiness:

- Pan-EU sanctions list integration with sub-second updates

- Risk scoring models calibrated to AMLR-specified high-risk factors

- Auditable alert management with full documentation chains for AMLA examination

- SAR workflow from alert to submission with built-in quality-check gates

- API connectivity for integration with third-party identity verification providers

The EU AI Act and AML: A Parallel Compliance Challenge

For institutions investing in anti money laundering technology as part of AMLR readiness, eu ai act financial services obligations add a second compliance layer running on roughly the same timeline. The EU AI Act, which entered force in August 2024 with phased obligations running through 2027, classifies AI systems used for fraud detection and creditworthiness assessment as high-risk. AML transaction monitoring systems that use machine-learning risk scoring likely fall into this category, which has direct consequences for procurement and model governance.

What High-Risk AI Classification Means for AML Systems

High-risk AI classification under the EU AI Act requires technical documentation before deployment, conformity assessment, human oversight mechanisms that constitute genuine review rather than a rubber stamp, data governance controls on training datasets, logging of system decisions for post-hoc review, and registration in the EU database for certain use cases. For compliance officers, this creates a direct intersection: the aml compliance software you deploy to meet AMLR obligations must itself comply with EU AI Act requirements if it uses machine learning for risk scoring. The documentation and model governance requirements are significantly more formal than most institutions' current practices.

The DORA compliance automation strategy for financial institutions offers a practical framing for managing AMLR, DORA, and the EU AI Act as a single integrated governance program through regulatory compliance automation, rather than treating them as three separate projects competing for the same compliance team bandwidth.

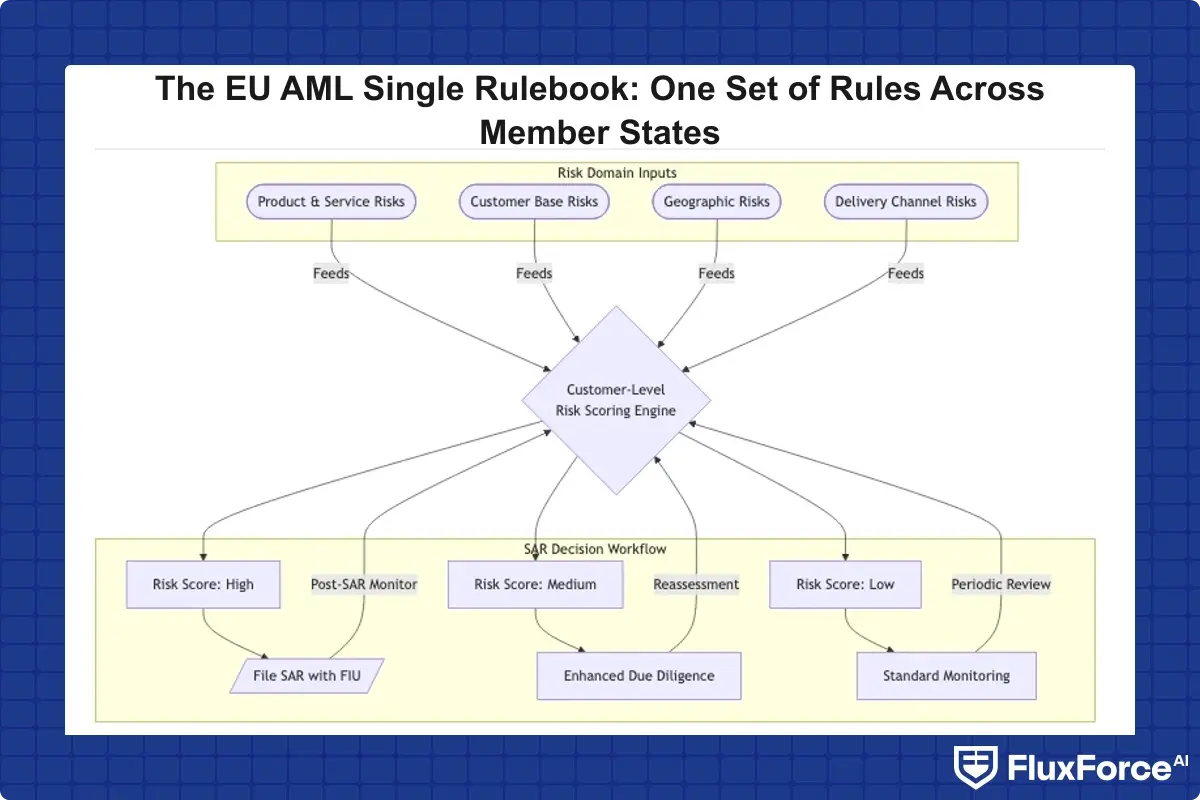

Building an AML Risk Assessment Guide for the AMLR Framework

The AMLR requires institutions to produce a documented aml risk assessment guide at both entity and customer levels. This is not conceptually new, but AMLR is considerably more prescriptive about content, documentation standards, and review frequency than the directives it replaces. Supervisors will expect to see a defensible, internally consistent assessment, not a template filled in once and left unchanged.

Entity-Level Risk Assessment Requirements

At the entity level, the AMLR requires assessment of product and service risks including new products and delivery channels, customer base risks covering geographic distribution and PEP concentration, geographic risks tied to countries of operation and high-risk third-country transaction corridors, transaction channel risks across correspondent banking and crypto, and delivery channel risks including non-face-to-face onboarding and third-party CDD reliance. The assessment must be reviewed at least annually and updated whenever material changes occur to the institution's business model or risk profile.

For bsa aml compliance community banks and smaller institutions, this documentation burden is often where external expertise or purpose-built technology adds the most value. The skills to produce an AMLA-ready risk assessment are not always available in-house, and getting it wrong during a supervisory examination under the new benchmarked standards carries real consequences.

Customer-Level Risk Scoring and the AML Compliance Checklist

At the customer level, risk scores must be determined at onboarding, recalculated when material risk indicators change, reviewed periodically across the full customer base at frequencies proportionate to risk category, and documented in a way that supports the SAR decision if suspicion later arises. A bsa aml compliance checklist adapted for AMLR would verify that your risk scoring model covers all AMLR-specified factors, that your EDD trigger thresholds are documented and defensible, and that your technology stack generates the audit logs AMLA expects during examination. If your current system cannot produce a complete decision trail from customer onboarding through to SAR filing, that is a gap to close before July 2027.

What AMLA Supervision Means in Practice

AMLA will directly supervise approximately 40 of the riskiest cross-border obliged entities from January 2028. For other institutions, national competent authorities remain primary supervisors, but AMLA has coordination and benchmarking powers that will effectively raise supervisory standards across the EU regardless of whether your institution falls into the direct supervision cohort.

How AMLA Assesses AML Compliance

AMLA's supervisory methodology is expected to focus on the quality of the institution's own AML risk assessment, the effectiveness of transaction monitoring measured by alert-to-SAR conversion rates and the quality of reports filed with FIUs, governance evidence that senior management genuinely owns AML risk rather than delegating it entirely to compliance, and technology adequacy confirming that anti money laundering technology is calibrated to the institution's actual risk profile rather than deployed as a generic off-the-shelf solution.

Preparing for AMLA-Style Examinations

The shift toward AMLA-benchmarked supervision is a practical prompt to assess whether your current sanctions screening automation and broader AML technology stack would withstand rigorous examination. Institutions that have under-invested in technology because their national supervisor lacked examination depth will find the AMLA era significantly more demanding. Preparation should include a gap analysis against AMLR's CDD and record-keeping requirements, a structured review of sar filing efficiency metrics from the past 12 months, and a stress test of your risk assessment documentation against the criteria AMLA has publicly signaled it will apply.

- The EU AML Single Rulebook is a package of four legislative acts adopted in 2024, designed to create a true single market for financial crime prevention.

- For years, EU AML rules relied on directives, which each member state transposed into national law differently.

- Kyc automation sits at the operational heart of the new framework.

- Suspicious activity report obligations are among the most technically changed areas in the AMLR.

- The eu aml single rulebook extends to fintechs operating in Europe more explicitly than previous directives.

Onboard Customers in Seconds

Conclusion

The eu aml single rulebook is not simply another directive to transpose. It is a structural change in how aml compliance operates across Europe. Direct applicability means the same rules apply in Tallinn as in Madrid. AMLA's supervisory role means enforcement quality converges upward across all 27 member states. For banks, fintechs, insurers, and payment institutions, the organisations that manage this transition without disruption are the ones investing now in aml compliance software capable of handling pan-EU requirements, kyc automation that scales with AMLR's due diligence demands, and sar filing workflows that produce the report quality AMLA expects.

The application date is July 2027. That sounds distant until you factor in procurement cycles, systems integration, staff training, and a parallel EU AI Act compliance program running on nearly the same timeline. Institutions treating this as a 2026 problem will be scrambling. If you want to understand how regulatory compliance automation can help your team build a compliant program ahead of the AMLR timeline rather than behind it, the tools and frameworks to move quickly already exist.

Share this article