.webp)

Listen To Our Podcast🎧

Introduction

The eIDAS 2.0 digital identity wallet regulation is the most significant overhaul of European digital identity infrastructure in a decade, and banks have until 2026 to be ready for it. Enacted as Regulation (EU) 2024/1183, the regulation requires all EU member states to provide citizens with a standardized digital identity wallet. For banks, this is not an abstract policy issue. It reshapes KYC workflows, introduces new biometric identity verification requirements, and opens the door to fraud vectors that most institutions have not yet tested against. Getting ahead of it now avoids the scramble that characterized PSD2 adoption.

- What Is eIDAS 2.0 and How Does It Differ from eIDAS 1.0?

- Why Banks Face New Compliance Obligations Under eIDAS 2.0

- How the eIDAS 2.0 Digital Identity Wallet Changes KYC Onboarding Speed

- Biometric Identity Verification and Liveness Detection Requirements

- Synthetic Identity Fraud Risks in a Wallet-Enabled Environment

Onboard Customers in Seconds

What Is eIDAS 2.0 and How Does It Differ from eIDAS 1.0?

eIDAS 1.0, introduced in 2014, created a framework for electronic signatures and cross-border identity recognition across EU member states. It worked in principle but struggled in practice. Adoption was fragmented, the user experience was inconsistent, and private sector reliance was voluntary. Fewer than 20% of EU citizens ever used an eID scheme under eIDAS 1.0, according to European Commission data on digital identity adoption.

Fewer than 20% of EU citizens ever used an eID scheme under eIDAS 1.0, according to European Commission data on digital identity adoption.

eIDAS 2.0 addresses those failures directly. It mandates that every EU member state issue a European Digital Identity (EUDI) Wallet to any citizen who wants one, and it requires large online platforms and regulated sectors, including banking, to accept those wallets as a valid form of identification.

The Architecture of the EU Digital Identity Wallet

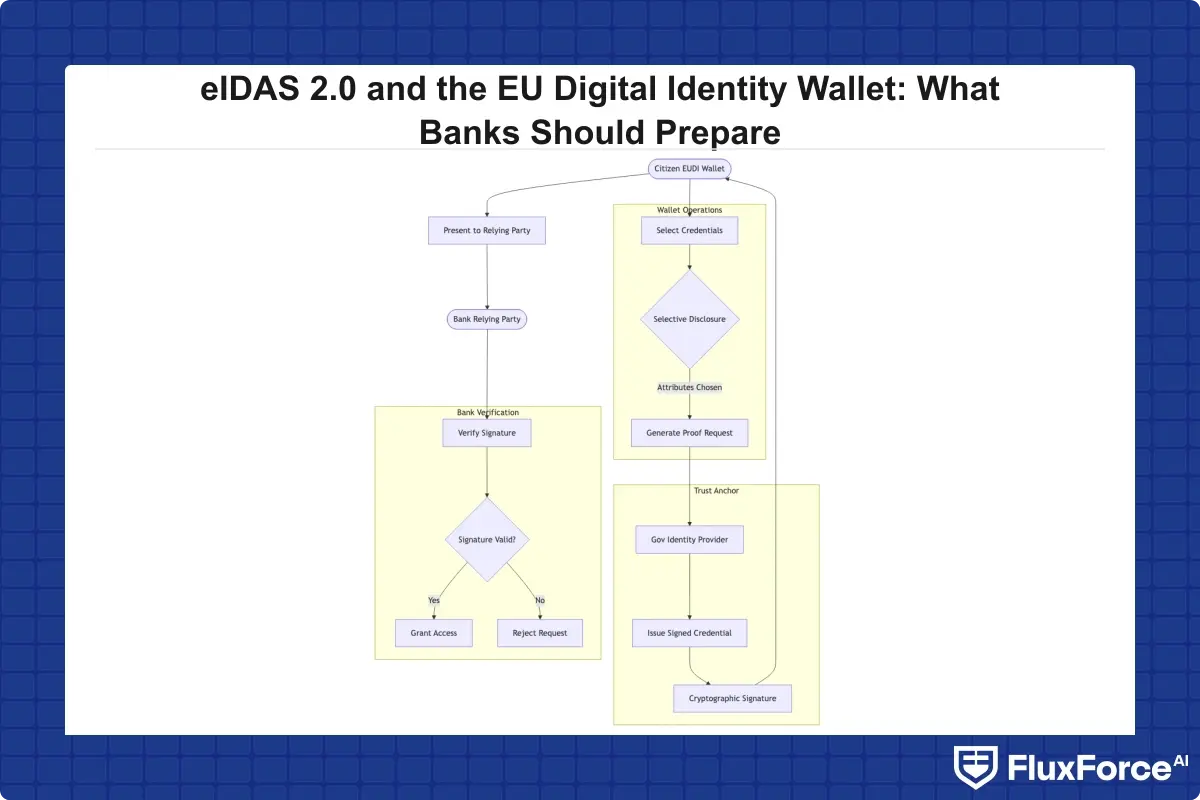

The EUDI wallet is a smartphone application that stores verifiable digital credentials: government-issued identity documents, age proofs, professional qualifications, and payment-related attributes. Each credential is issued by a trusted authority and cryptographically signed. The wallet holder controls which attributes they share with a service provider.

For a bank, this means a customer can present their identity wallet during account opening, and the bank receives a signed, government-attested assertion of the customer's legal name, date of birth, and national ID number without handling a physical document or a selfie upload. The bank does not see the underlying document; it sees a verified claim.

Key Differences Between eIDAS 1.0 and eIDAS 2.0

| Feature | eIDAS 1.0 | eIDAS 2.0 |

|---|---|---|

| Wallet issuance | Optional, state-dependent | Mandatory for all EU states |

| Private sector acceptance | Voluntary | Mandatory for regulated sectors |

| Attribute disclosure | All-or-nothing | Selective disclosure |

| Cross-border recognition | In theory | Enforced with full mutual recognition |

| Assurance levels | Low, Substantial, High | Same, with stricter High-level requirements |

The selective disclosure feature matters for financial services. A customer verifying their age for a regulated product can share only that attribute, without revealing their address or national ID number.

Why Banks Face New Compliance Obligations Under eIDAS 2.0

The regulation is explicit: banks and other credit institutions fall within the category of relying parties that must accept the EUDI wallet for identity verification. This is not optional. Once wallet deployment reaches scale across member states (expected 2026), institutions that refuse wallet-based authentication during KYC processes will be non-compliant.

There are two practical implications compliance officers need to understand now.

Mandatory Acceptance Timelines

The European Banking Authority has been aligning eIDAS 2.0 wallet acceptance with strong customer authentication requirements under PSD2. Banks will need to update their identity verification API to parse wallet credentials, verify cryptographic signatures, and confirm the assurance level of the issuing authority.

Member states have until 2026 to deploy wallets at scale. Banks technically have the same window, but integrating a new authentication method into core banking systems takes 12-18 months when done properly. Institutions starting after mid-2025 are running close to the margin.

Cross-Border Identity Verification in Fintech

For banks operating across multiple EU jurisdictions, eIDAS 2.0 removes the current patchwork of national identity schemes. A French customer opening an account with a German bank can use their French EUDI wallet, and the German bank must accept it. This is new territory. Today, cross-border identity verification fintech processes typically require a private identity proofing vendor with country-specific integrations.

The wallet standardizes that process, but it also means banks need to test their KYC workflows against wallet credentials from every member state where they operate, not just their home jurisdiction.

How the eIDAS 2.0 Digital Identity Wallet Changes KYC Onboarding Speed

One practical argument for early adoption is that the eIDAS 2.0 digital identity wallet can meaningfully improve kyc onboarding speed. Current digital onboarding in European banking averages 8-12 minutes per customer, with document upload and manual review steps accounting for most of that time.

KYC Onboarding Speed Improvements with Wallet Credentials

When a customer presents a wallet credential, the bank receives a machine-readable, pre-verified assertion. There is no OCR processing of a passport scan, no manual review of a selfie against a document photo, and the assurance level is declared upfront. For banks that have invested in KYC and AML identity verification automation, wallet credentials are a natural extension that reduces marginal cost per onboarding while maintaining compliance quality.

The honest caveat: kyc onboarding speed improvements depend entirely on how well backend systems are prepared to consume wallet credentials. If manual steps remain downstream of the credential check, such as compliance review queues and sanctions screening, the wallet removes the document handling bottleneck but not the compliance workflow itself.

Digital Identity Proofing Standards Under eIDAS 2.0

Digital identity proofing under eIDAS 2.0 is governed by three assurance levels: Low, Substantial, and High. For most banking use cases, including account opening and payment authorization, the High assurance level is required. High assurance means the identity proofing was conducted using qualified biometric means with matching against a government-issued document.

Banks using commercial digital identity proofing vendors need to verify that their provider's process meets the High assurance definition. Many commercial processes meet Substantial but not High. The gap matters because wallet credentials at High assurance carry significantly more legal weight in dispute resolution. According to the European Commission's eIDAS guidance, the High assurance level is specifically required when a failure would cause significant damage to the relying party or the user, which describes nearly every banking interaction.

Biometric Identity Verification and Liveness Detection Requirements

Biometric identity verification sits at the center of eIDAS 2.0 compliance, both for the wallet issuance process and for any bank using biometric matching as part of wallet credential verification. The regulation requires that High assurance wallets be bound to the holder through biometric means, which in practice means a facial recognition match against a government record during enrollment.

Liveness Detection Fraud Prevention

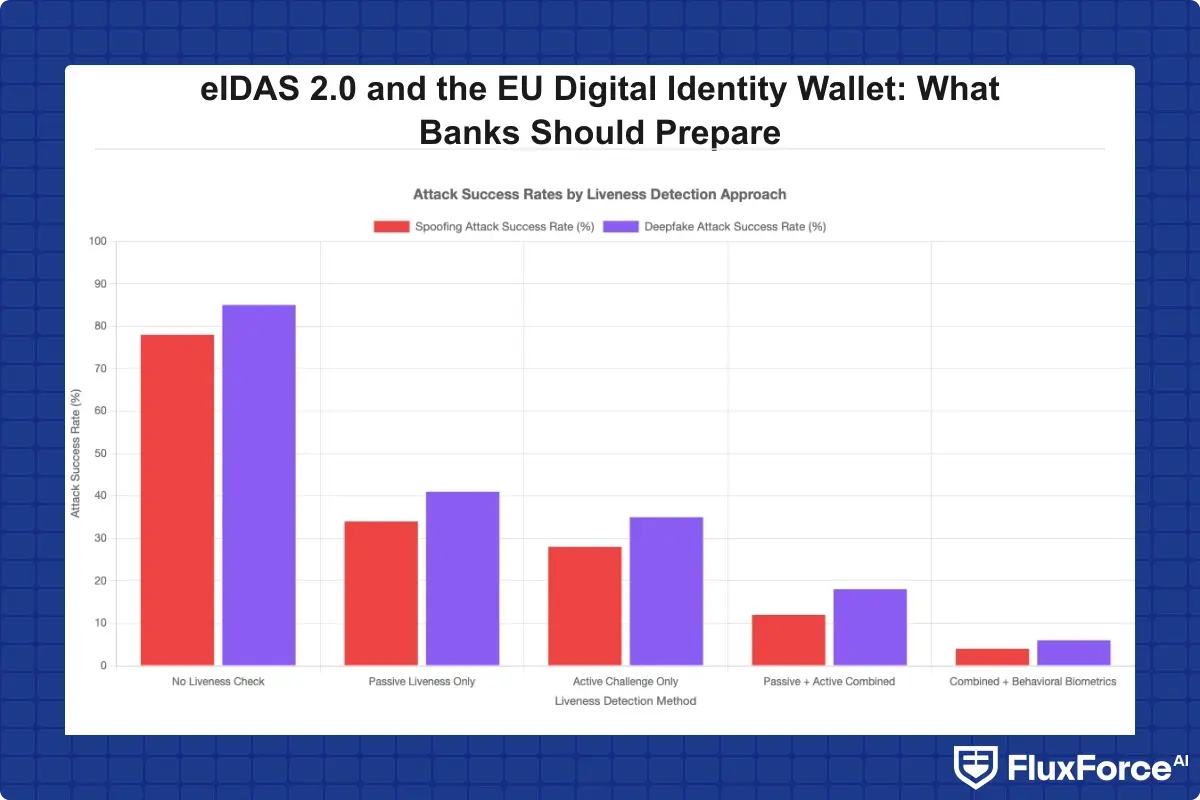

Liveness detection fraud is the attempt to spoof a biometric check using a photograph, video, or 3D mask. As biometric identity verification becomes mandatory for regulated onboarding, the financial incentive to defeat it increases proportionally. Current liveness detection fraud attacks succeed against legacy passive systems at rates that would be unacceptable under the wallet's High assurance requirements.

The NIST Special Publication 800-63B on digital authentication provides the most widely cited framework for authenticator assurance, and European standards bodies have aligned eIDAS 2.0 technical requirements closely with NIST's model. Banks should treat liveness detection as a compliance requirement now, not an optional security layer.

Deepfake Detection in Banking

Deepfake detection banking is a newer problem that deserves separate attention. Generative AI tools have made it possible to create convincing synthetic video of a real person, which can defeat video-based liveness checks. Several European banks reported deepfake-related onboarding fraud attempts in 2024, and the attack surface will grow as wallet adoption spreads.

The practical response requires multiple layers. Passive liveness detection (analyzing texture and depth cues without requiring user action) should be combined with active challenges (asking the user to perform a specific movement in real time). Neither method alone is sufficient. Adding behavioral biometrics during the onboarding session provides a secondary signal that deepfake detection banking workflows need to account for.

For teams building this defense stack, there is useful overlap with broader fraud detection infrastructure. Real-time synthetic identity fraud detection requires a similar layering of signals, and the architectural patterns translate directly to liveness defense.

Synthetic Identity Fraud Risks in a Wallet-Enabled Environment

The eIDAS 2.0 wallet solves one problem well: it makes fabricating an identity entirely much harder. Government-issued credentials with cryptographic attestation are genuinely difficult to forge. But synthetic identity fraud does not disappear. It shifts to where the wallet is weakest.

Synthetic Identity Fraud Detection at the Wallet Layer

Synthetic identity fraud detection becomes more complex in a wallet environment because the wallet credential itself may be legitimate. A fraudster who successfully obtains a government-issued credential through social engineering at a registration authority, a SIM swap during wallet enrollment, or other upstream manipulation will present a technically valid wallet. The credential passes signature verification. The assurance level checks out. The fraud happened before the bank ever saw the customer.

This means banks cannot treat wallet verification as the endpoint of the identity check. Behavioral analytics, account velocity monitoring, and correlation against known synthetic identity fraud networks remain necessary. The wallet is strong evidence of identity, not absolute proof.

Zero Trust Financial Services as a Countermeasure

Zero trust financial services architecture is the right framework for wallet-based onboarding. The core principle is that credential verification at the door is not sufficient. Every subsequent session, transaction, and API call should be evaluated against current risk signals.

A customer who presents a valid wallet credential during onboarding but exhibits unusual transaction patterns within 30 days should trigger re-verification, not continue on the trust level granted at onboarding. This is the fundamental logic behind zero trust security architecture for banking operations: trust is earned continuously, not granted once. A zero trust security framework applied to post-onboarding monitoring catches the fraud that wallet acceptance alone cannot prevent.

Building Your Identity Verification API Stack for Wallet Acceptance

The technical work of eIDAS 2.0 compliance for banks centers on the identity verification API layer. The EUDI wallet uses OpenID4VP (OpenID for Verifiable Presentations) as its primary presentation protocol, alongside OpenID4VCI for credential issuance. Banks that have not worked with these protocols need to start building that capability now.

API Integration Patterns for Wallet Credential Verification

The wallet interaction follows a structured pattern: the bank's relying party software sends a presentation request specifying which attributes it needs, the wallet holder approves the request on their device, and the wallet returns a signed verifiable presentation. The bank's backend verifies the signature against the issuer's public key, checks credential revocation status, and extracts the required attributes.

This sounds straightforward, but complications arise in practice. The bank needs to maintain a trusted issuer registry to know which government authorities' signatures to accept. Credential revocation checking requires live connectivity to a status endpoint. The presentation request format must comply with the EUDI Wallet Architecture and Reference Framework, which is still being refined ahead of 2026 deployment.

For most banks, the realistic path is to work through an identity verification fintech provider that has already implemented the OpenID4VP stack and maintains the issuer registry. Building and maintaining this in-house is expensive, and the vendor market is still forming. Evaluating providers now, before the 2026 deadline creates competitive pressure on pricing and availability, is the sensible move.

Zero Trust Security Framework for the Wallet Pipeline

The identity verification API handling wallet credentials is a high-value attack target. It receives sensitive identity data and makes trust decisions that gate account access. A zero trust security framework applied to this pipeline means mutual TLS for all connections, short-lived access tokens, full logging of every credential verification request and response, and anomaly detection on verification traffic patterns.

Zero trust security for mobile-first banks covers the broader architectural approach, and the principles apply directly to the wallet verification pipeline. Any anomalous pattern in wallet credential submissions, such as unusually high volumes from a single device or credentials from unexpected jurisdictions, should trigger automated review.

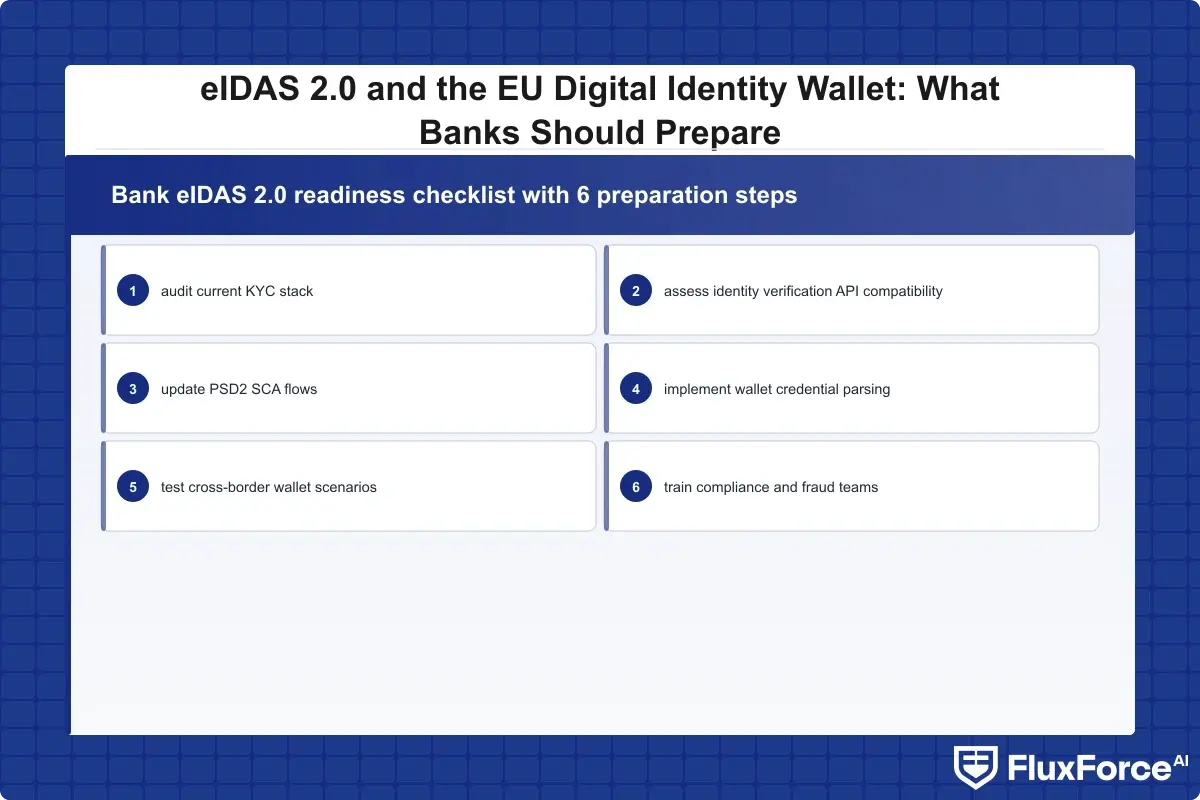

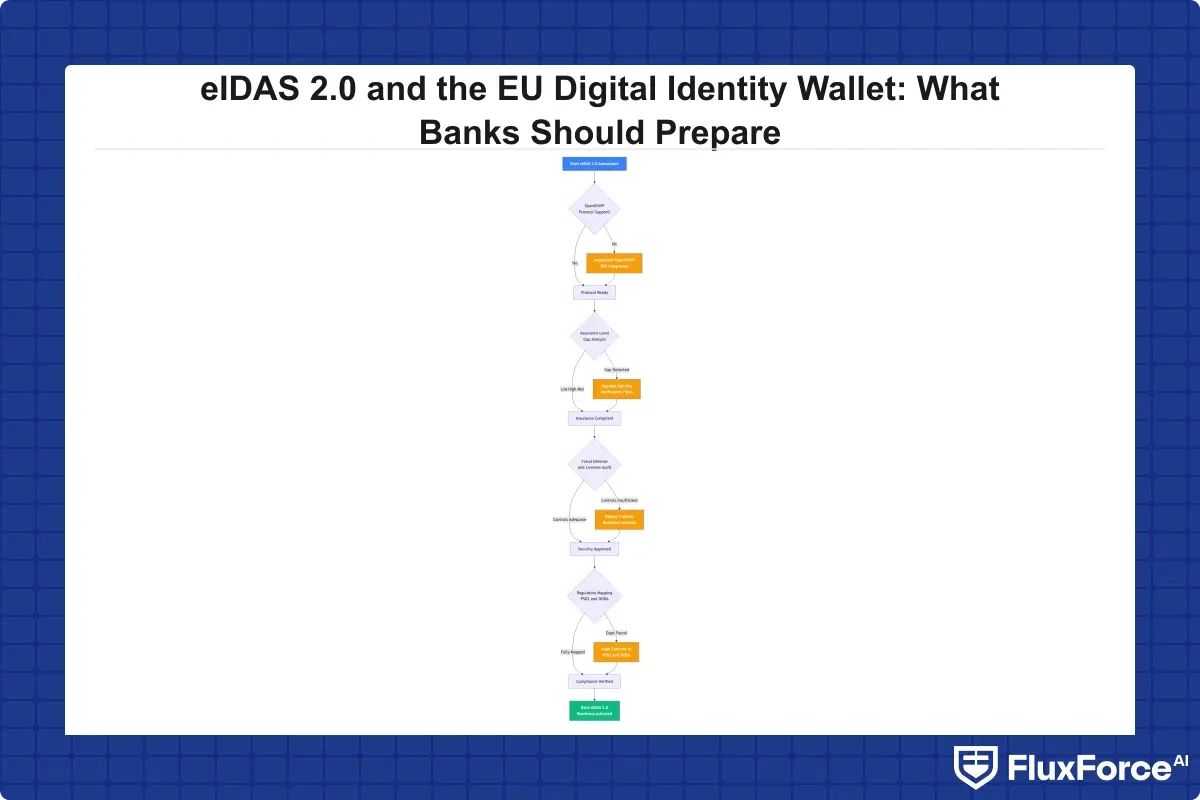

The 4 Core Readiness Areas Banks Should Address Now

Most banks are not starting from zero. They have existing KYC infrastructure, identity verification vendors, and biometric matching already deployed. The preparation work is largely about assessing gaps against eIDAS 2.0 requirements and closing them before the deadline. The 4 core readiness areas are:

Protocol compatibility: Does your identity verification API support OpenID4VP and OpenID4VCI? If not, identify which vendor or internal project will deliver that support, and set a firm delivery date.

Assurance level alignment: Does your current digital identity proofing process meet the High assurance standard under eIDAS 2.0? Obtain a formal gap analysis against the EUDI Wallet Architecture and Reference Framework, either from your vendor or an independent auditor.

Fraud defense uplift: Have you updated your liveness detection stack within the last 18 months and tested it against deepfake attacks? Synthetic identity fraud detection procedures need to account for wallet credentials appearing technically valid while being obtained fraudulently.

Regulatory coordination: eIDAS 2.0 intersects with PSD2, GDPR, and DORA. Your compliance team needs a consolidated view of how wallet acceptance changes your obligations under each regulation. Teams working through DORA compliance automation for financial institutions will find relevant overlap in the technical resilience and access control requirements.

- eIDAS 1.0, introduced in 2014, created a framework for electronic signatures and cross-border identity recognition across EU member states.

- The regulation is explicit: banks and other credit institutions fall within the category of relying parties that must accept the EUDI wallet for identity verification.

- One practical argument for early adoption is that the eIDAS 2.0 digital identity wallet can meaningfully improve kyc onboarding speed.

- Biometric identity verification sits at the center of eIDAS 2.0 compliance, both for the wallet issuance process and for any bank using biometric matching as part of wallet credential verification.

- The eIDAS 2.0 wallet solves one problem well: it makes fabricating an identity entirely much harder.

Onboard Customers in Seconds

Conclusion

The eIDAS 2.0 digital identity wallet changes how identity verification works in European banking in ways that will be difficult to reverse once they become standard practice. Banks that treat this as a compliance checkbox will find themselves with rushed integrations and untested fraud defenses in 2026. Institutions that start now have 12-18 months to audit their existing identity verification fintech stack, close assurance level gaps, uplift their liveness and deepfake detection capabilities, and prepare their identity verification API for OpenID4VP.

The fraud picture matters as much as the compliance one. Biometric identity verification requirements raise the barrier for attackers, but liveness detection fraud and deepfake attacks will intensify as the wallet becomes a more valuable target. A zero trust security framework applied to the wallet verification pipeline, combined with continuous post-onboarding behavioral monitoring, is the right countermeasure for the threat environment ahead. The banks that prepare carefully now will find the transition much less disruptive than those that wait.

Share this article