.webp)

Listen To Our Podcast🎧

Introduction

Digital identity verification in financial services has become the foundation on which banks, fintechs, and insurers build trust with customers and regulators alike. As fraud schemes grow more sophisticated and regulatory scrutiny intensifies, institutions can no longer rely on manual document checks or siloed verification tools. The gap between what legacy systems can do and what modern risk demands has widened considerably, and the institutions closing that gap are doing so with AI, platform consolidation, and explainable decision-making baked into every layer of their identity stack. This post covers the core technologies at play, the genuine challenges institutions face when scaling identity verification, and the practices that separate effective programs from box-ticking exercises.

- Why Digital Identity Verification in Financial Services Cannot Wait

- Core Technologies Powering Modern Identity Verification

- How Explainable AI Is Reshaping Compliance

- The Case for a Unified Risk Platform Over Point Solutions

- Key Challenges in Identity Verification at Scale

Onboard Customers in Seconds

Why Digital Identity Verification in Financial Services Cannot Wait

The average cost of a financial fraud incident involving identity exceeds $1,000 per case when investigation, remediation, and regulatory reporting are factored in. That number compounds quickly at scale. The more immediate pressure is regulatory: the EU's AML6 directive, the US Bank Secrecy Act, and DORA all treat identity verification as a first-line control, not a back-office formality.

The average cost of a financial fraud incident involving identity exceeds $1,000 per case when investigation, remediation, and regulatory reporting are factored in.

The Cost of Getting Identity Checks Wrong

When identity verification fails, the consequences split in two directions. False negatives let fraudulent actors through: synthetic identities, money mule accounts, and compromised credentials slip into the customer base. False positives are equally damaging, just more quietly. Legitimate customers get blocked, abandonment rates climb, and the support cost of manual reviews eats into margins.

Institutions running KYC and AML identity verification processes on disconnected point solutions often see both problems simultaneously: rigid rule sets that catch too little, and alert volumes that overwhelm analyst teams.

Regulatory Drivers Shaping Verification Standards

FATF guidance on digital identity provides the clearest international baseline, distinguishing between identity evidence strength, identity verification strength, and authentication assurance level. These are three distinct concepts that many institutions still conflate in their controls. Regulators in the UK (FCA), EU (EBA), and US (OCC) have all issued guidance referencing AI-based verification tools and the governance requirements that come with them.

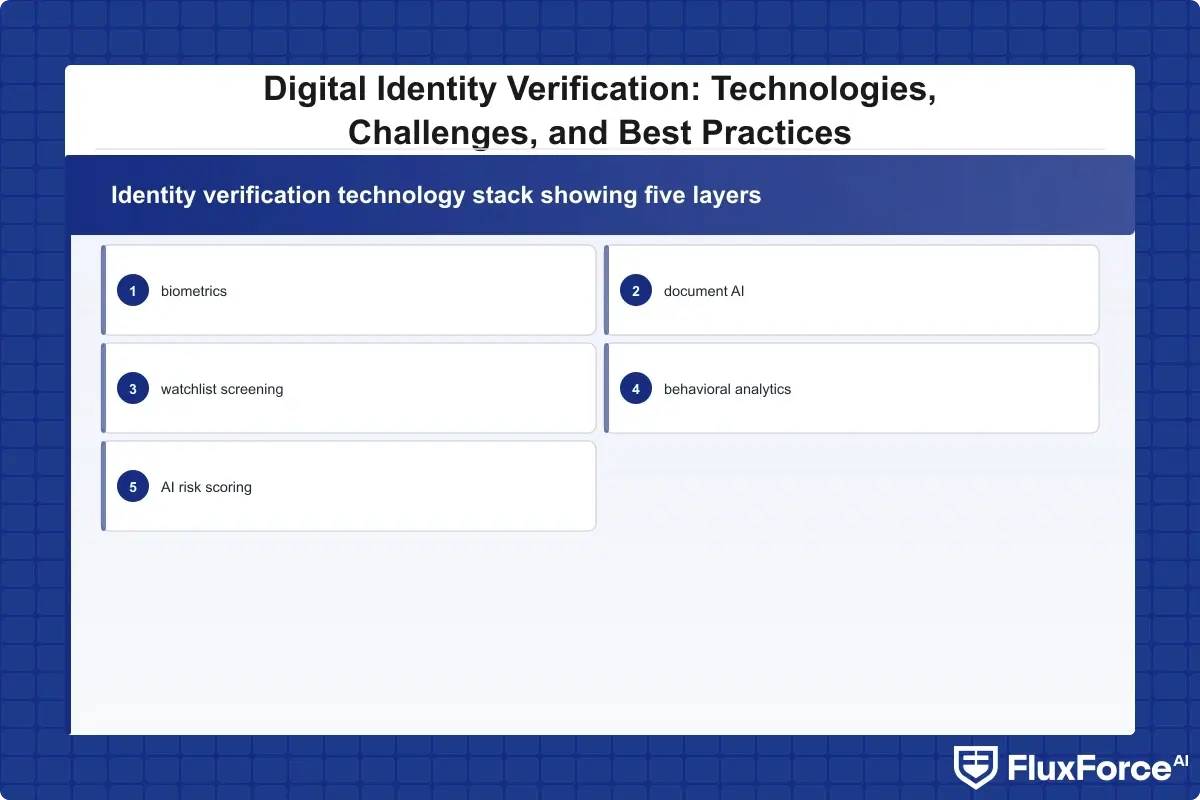

Core Technologies Powering Modern Identity Verification

Digital identity verification in financial services today is not one technology. It is a stack, and the strength of the stack depends on how well each layer integrates with the others.

Biometric Verification and Liveness Detection

Facial recognition paired with passive liveness detection is now table-stakes for onboarding. The meaningful differentiator is 3D liveness detection, which resists deepfake injection attacks that flat 2D checks miss. According to research from NIST's face recognition vendor testing program, error rates between vendors vary by an order of magnitude on demographic subgroups, which creates both compliance risk and fair-lending exposure if institutions choose carelessly.

Document Authentication and OCR

AI-powered document authentication checks for print quality, font consistency, security feature presence, and tamper indicators in under two seconds. Optical character recognition (OCR) extracts data for cross-referencing against authoritative sources. The honest limitation here: document fraud has also gotten better. Deepfake document generators can produce IDs that pass basic ML checks, which is why document authentication should never be the sole verification layer.

Database Cross-Checks and Watchlist Screening

Real-time screening against sanctions lists (OFAC, UN, EU), PEP databases, and adverse media feeds completes the picture. The challenge is data latency: sanctions lists update irregularly, and institutions that screen only at onboarding miss post-onboarding changes. Continuous monitoring is the standard now, not periodic batch checks. This continuous approach to building a fraud compliance identity platform is what regulators increasingly expect during examinations.

How Explainable AI Is Reshaping Compliance

Explainable AI in finance is not a nice-to-have. It is a regulatory requirement in practice, even where no statute uses the exact term. The EU AI Act, the FCA's Consumer Duty, and the US CFPB's adverse action notice requirements all create situations where a model's output must be explained to a human, whether that human is a regulator, a compliance officer, or a rejected applicant.

What Regulators Actually Want from AI Models

The short answer: they want to understand why a model made a decision, whether that decision was consistent, and whether it can be audited after the fact. Explainable AI compliance means the institution can answer those three questions for any individual decision. That rules out scenarios where black box AI compliance risk produces correct aggregate outcomes but cannot explain individual ones.

The practical test is this: if a regulator asks you to justify a specific declined application or a flagged transaction, can your system produce a readable explanation within minutes? If the answer involves exporting data to a separate analytics environment and running manual queries, you have a gap. AI model explainability for regulators is no longer an advanced capability. It is expected baseline functionality.

SHAP Values and Model Transparency in Practice

SHAP values (SHapley Additive exPlanations) have become the dominant technique for explaining individual model decisions. SHAP values explained to regulators means showing exactly which input features drove a risk score and by how much. For example: a document verification check scored at 0.83 risk might show that device fingerprint mismatch contributed +0.31, biometric confidence gap contributed +0.18, and document age contributed +0.21. That granularity allows compliance teams to respond to regulatory inquiries without rebuilding the analysis from scratch.

Moving Beyond Black Box AI in Compliance Risk

Black box AI compliance risk is not just a regulatory problem. It is an operational one. When models produce decisions that analysts cannot interrogate, two things happen: analysts lose confidence in the system and start overriding it arbitrarily, or they trust it too completely and miss edge cases. Neither outcome is acceptable in a regulated identity verification context. XAI fraud detection tools that surface feature attribution at the decision level give analysts the context to override intelligently. Explainable AI finance tools that embed this transparency into the compliance workflow close the gap between what models do and what compliance teams can defend in an examination.

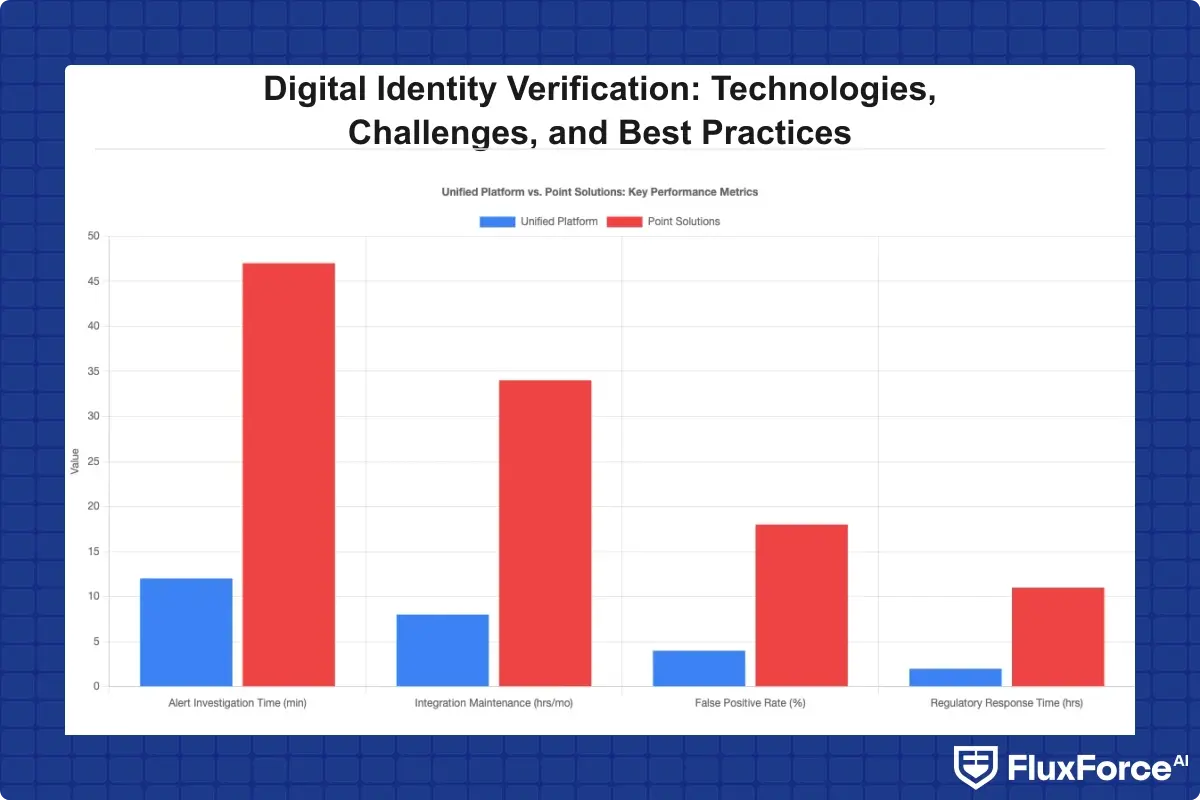

The Case for a Unified Risk Platform Over Point Solutions

The point solutions vs. platform financial services debate has largely been settled by the economics. Institutions running eight, ten, or twelve separate vendors for identity verification, fraud detection, sanctions screening, and compliance monitoring face integration costs that compound annually. More importantly, they face a data coherence problem: each tool operates on its own view of a customer, and reconciling those views is manual, slow, and error-prone.

The Hidden Costs of Vendor Sprawl

Vendor consolidation in fintech is not primarily about reducing license fees, though that matters. The deeper cost is the analyst time spent context-switching between dashboards, the engineering overhead of maintaining integrations, and the latency introduced when fraud signals from one system have to be manually imported into another. One fraud analyst managing three separate tools is effectively working with fragmented context that a unified system would present automatically.

This is the core argument for a unified risk platform approach: a single system that holds fraud detection, identity verification, and compliance controls in the same data model, with shared signals and a single audit trail.

How Platform Consolidation Reduces Operational Friction

A fraud compliance identity platform that covers KYC, AML screening, and behavioral fraud detection in one place gives compliance teams something point solutions cannot: correlated alerts. When a customer's identity verification passes but their transaction behavior over the next 48 hours matches a mule account pattern, a platform with shared data surfaces that connection automatically. Disconnected tools cannot.

The AI security operations platform pattern, borrowed from cybersecurity's SIEM model, applies the same logic to financial crime. All signals flow into a single engine. Decisions are centralized. The audit trail is complete and queryable in one place. Vendor consolidation in fintech is not just about cost. It is about coherence.

Key Challenges in Identity Verification at Scale

Getting identity verification right in a proof-of-concept environment is one thing. Getting it right at 50,000 applications per day is different. These are the challenges that actually matter at scale.

Balancing False Positives Against Customer Friction

Optimizing purely for fraud prevention creates a problem on the other side. Tightening thresholds reduces fraud but increases false positives, which means more legitimate customers get declined or stuck in manual review queues. The right answer is not a single global threshold but a tiered model: low-risk applications auto-approve, high-risk ones route to human review, and the middle tier gets additional verification steps rather than a hard decline.

Human in the loop AI banking is most valuable in that middle tier, where a trained analyst can make a judgment call the model cannot. For a detailed look at how AI fraud agents reduce false positives without sacrificing detection rates, see how agentic AI cuts false positives by 80%.

For a detailed look at how AI fraud agents reduce false positives without sacrificing detection rates, see how agentic AI cuts false positives by 80%.

Cross-Border Identity Complexity

Cross-border identity verification introduces a different class of problem: document standards, ID formats, and data privacy rules differ by jurisdiction. A verification flow designed for UK passport holders does not work cleanly for applicants from jurisdictions where national ID cards use non-Latin characters or where address verification relies on informal reference systems. Institutions operating globally need configurable AI autonomy that allows jurisdiction-specific rules without rebuilding the entire verification stack per market.

When AI Needs Human Judgment

Human in the loop AI banking is a design choice, not a fallback position. The question is not whether humans should be involved but at which decision points their involvement adds more value than cost. AI agents in financial services contexts should handle routine decisions at speed and route ambiguous cases to analysts with full context: model confidence scores, feature attributions, and the customer's historical behavior. An analyst reviewing a case with that context can resolve it in minutes. An analyst reviewing a raw document image with no model context takes much longer and makes more errors.

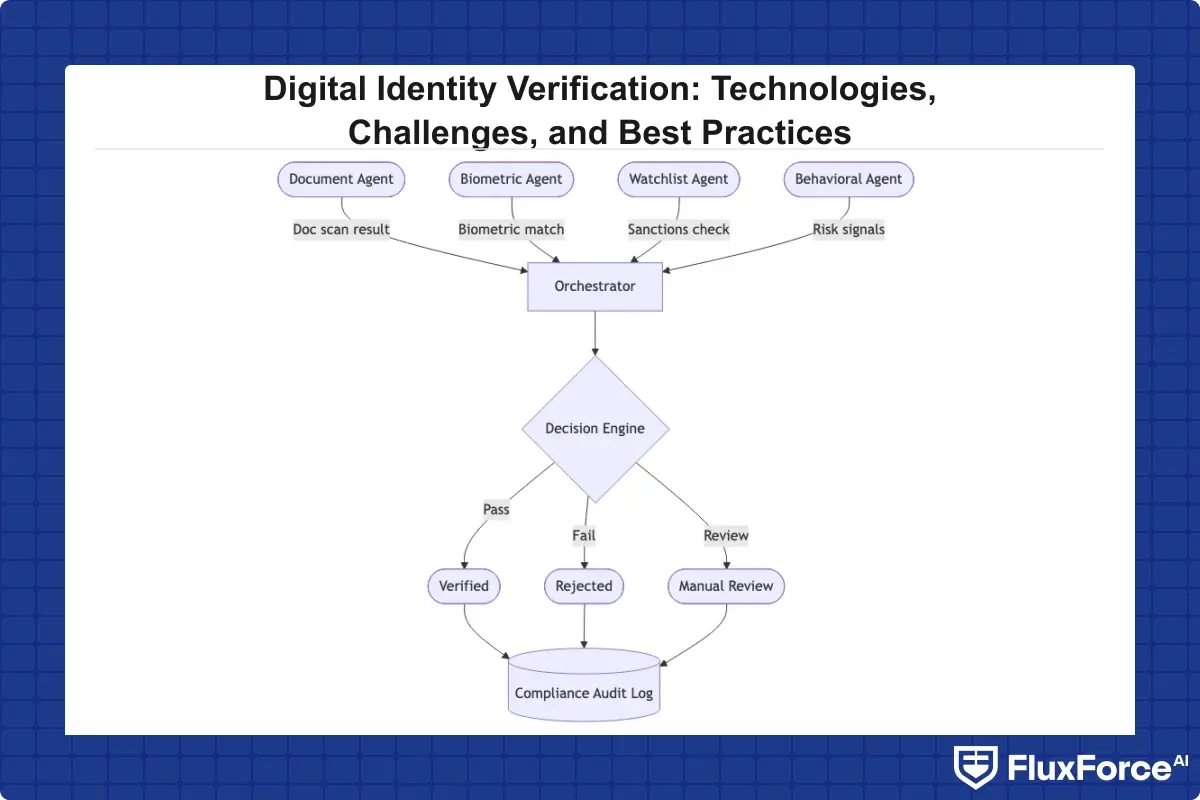

What Multi-Agent AI Systems Bring to Identity Verification

The move toward multi-agent AI systems in financial services reflects a practical limitation of single-model approaches. A single model trained on fraud patterns may not transfer cleanly to KYC decisions. A single model trained on document authentication may not generalize to behavioral anomaly detection. Multi-agent architectures assign specialized models to specific tasks and coordinate their outputs through an orchestration layer.

AI Agents Coordinating Across Fraud, KYC, and Compliance

A multi agent AI system for identity verification works when separate agents handle distinct tasks: one agent assesses document authenticity, another evaluates biometric confidence, a third checks watchlist matches, and a fourth scores behavioral risk. An orchestrator combines their outputs into a final risk decision. This division of labor means each agent can be trained, tested, and updated independently, which is critical for compliance because it allows targeted model updates when regulatory requirements change without retraining the entire system.

AI agent fraud detection operating within this architecture surfaces correlations across channels that single-model systems miss. When document confidence is borderline but device reputation is poor and the session shows scripted behavior, the orchestrator catches the combination even if no individual signal crosses a threshold alone.

Configurable AI Autonomy for Regulated Environments

Institutions using AI underwriting agents for lending decisions face the same governance question as those deploying identity agents: how much decision authority should the system hold, and under what conditions should it escalate? Configurable AI autonomy means the institution decides this through policy, not through engineering change requests. For applicants in tier-1 jurisdictions with document confidence above 95%, auto-approve. For applicants in high-risk jurisdictions or with confidence between 70-95%, route to review. Below 70%, decline or escalate. That policy is auditable, explainable, and adjustable without touching the underlying models.

For applicants in tier-1 jurisdictions with document confidence above 95%, auto-approve.

Teams that build fraud detection software on a configurable agent framework can apply this same autonomy logic across fraud, KYC, and compliance workflows without building separate governance layers for each product line.

Best Practices for Deploying AI-Driven Identity Systems

Building an AI Audit Trail That Satisfies Regulators

An AI audit trail for automation must capture four things: what data the model received, what decision it produced, why it produced that decision (feature attribution), and who reviewed or overrode it. Systems that capture only the decision output cannot satisfy a regulatory inquiry. Systems that capture everything but store it in an inaccessible data warehouse create a compliance theater problem rather than solving one.

The audit trail should be queryable by case ID in under 60 seconds by a compliance analyst without engineering support. This is directly relevant to DORA requirements for digital operational resilience, where documentation of automated decision-making is an explicit expectation. For a breakdown of what that documentation looks like in practice, see DORA compliance automation for risk heads in banking.

Continuous Monitoring and Adaptive Controls

Identity verification is not a point-in-time event. Customers change. Fraud patterns shift. A customer who passes onboarding verification can still become a risk months later if their behavior changes or if they appear on a newly updated sanctions list. Continuous monitoring means the identity and risk profile updates in real time as new signals arrive, not just when the customer initiates a new product application.

Adaptive controls take this further: when the system detects a pattern shift, such as an uptick in a specific document type failing biometric checks, it should automatically tighten verification thresholds for that document type without requiring a manual policy change. This is where configurable AI autonomy and continuous monitoring intersect to create a system that keeps pace with fraud rather than perpetually chasing it.

- The average cost of a financial fraud incident involving identity exceeds $1,000 per case when investigation, remediation, and regulatory reporting are factored in.

- Digital identity verification in financial services today is not one technology.

- Explainable AI in finance is not a nice-to-have.

- Getting identity verification right in a proof-of-concept environment is one thing.

- The move toward multi-agent AI systems in financial services reflects a practical limitation of single-model approaches.

Onboard Customers in Seconds

Conclusion

Digital identity verification in financial services has moved past the point where document checks and basic database screening constitute a complete program. Regulators expect explainability, institutions need operational efficiency, and fraudsters are using the same AI tools that compliance teams are deploying against them. The institutions getting this right are consolidating onto unified risk platforms, deploying explainable AI compliance frameworks that produce auditable decisions, and building human-in-the-loop workflows that route AI outputs to analysts with full context rather than raw data.

The technology exists. The regulatory framework is increasingly specific. What separates effective programs from inadequate ones is the architectural decisions made early: unified platform or point solutions, explainable or opaque models, static rules or adaptive controls. Make those decisions deliberately, document them thoroughly, and build a system your compliance team can interrogate when regulators come asking.

Share this article