.webp)

Introduction

Confirmation of payee fraud prevention has moved from a regulatory checkbox to a frontline payment security control in the past three years. When someone sends a bank transfer and the destination account name does not match the account number, a name-check system flags it before the money moves. Simple in concept, but the reality is considerably messier: partial name matches, nickname variations, business trading names, and an explosion of authorised push payment (APP) scams have turned CoP into one of the most technically demanding problems in financial crime prevention.

This post breaks down how confirmation of payee works at the system level, where AI closes the gaps that rule-based checks leave open, and what compliance and operations teams inside banks and fintechs need to get right before rolling it out at scale.

- What Is Confirmation of Payee and Why It Matters Now

- How Misdirected Payments Fuel Fraud Losses

- How Confirmation of Payee Works in Practice

- Confirmation of Payee Fraud Prevention: Where AI Takes Over

- False Positives and the Cost of Getting Name-Checks Wrong

Onboard Customers in Seconds

What Is Confirmation of Payee and Why It Matters Now

Confirmation of payee (CoP) is a real-time name-verification service that checks whether the name a payer enters matches the name held against the destination account at the receiving bank. The UK's Payment Systems Regulator mandated CoP for the nine largest banks in 2020 under Specific Direction 10, and the requirement now extends to more than 400 payment service providers under the expanded framework.

The driver is APP fraud. According to UK Finance's Annual Fraud Report, UK consumers and businesses lost over £1 billion to APP fraud in 2023, with a significant share attributable to misdirected payments where a fraudster impersonates a legitimate payee. CoP directly attacks this vector by inserting a verified identity check at the exact moment a payment is initiated.

How Does CoP Differ from Traditional Account Validation?

Traditional account validation checks that a sort code and account number combination is valid and active. It tells you the account exists. CoP goes further: it confirms that the name on the account matches what the payer expects. That extra step is what stops invoice redirection fraud, where a criminal intercepts a legitimate payment instruction and swaps the bank details for their own. Without CoP, a bank has no way to distinguish a genuine payee from a criminal who has simply registered a plausible account name.

The Regulatory Push Driving CoP Adoption

The Financial Conduct Authority's Consumer Duty rules, effective from July 2023, create additional pressure. Firms must demonstrate that products cause no foreseeable harm to customers. Allowing a customer to make a payment to a fraudster's account without a name-check warning is exactly the kind of foreseeable harm regulators now expect firms to prevent. For CISOs and compliance officers, the question is no longer whether to implement CoP but how to do it in a way that holds up under scrutiny.

How Misdirected Payments Fuel Fraud Losses

Payment fraud prevention starts with understanding the loss pathways. Misdirected payments come from two sources: genuine mistakes (wrong account number typed by the payer) and deliberate manipulation (a fraudster who convinced the payer to change the destination details). CoP addresses both, but the fraud-driven version requires additional detection layers that go well beyond the name-check itself.

Authorised Push Payment Fraud: The Scale of the Problem

APP fraud is distinct from card fraud because the customer authorises the payment willingly. This makes it harder to reverse and harder to detect upstream. By the time a victim realises the payee was fraudulent, the money is often already across multiple mule accounts. A name-check that returns a mismatch at the point of payment is one of the few controls that interrupts this chain before it starts.

For banks relying on card fraud analytics and AI-powered fraud detection, adding CoP as a pre-payment gate creates a layered defence. Card-level controls catch post-authorisation manipulation; CoP catches account substitution at the initiation stage. The two layers address different points in the fraud lifecycle and should not be treated as substitutes for each other.

Why Synthetic Identity Fraud Makes Misdirected Payments Worse

Detecting synthetic identity fraud in real-time is hard enough on its own. When a fraudster opens an account using a fabricated identity, that account can pass basic validation checks because the account legitimately exists in the bank's systems. A CoP check against a synthetic identity account returns a "match" because the name on the account matches what the fraudster entered. This is where behavioural transaction monitoring, velocity checks, and network analysis must supplement the name-check layer to catch what CoP alone cannot.

How Confirmation of Payee Works in Practice

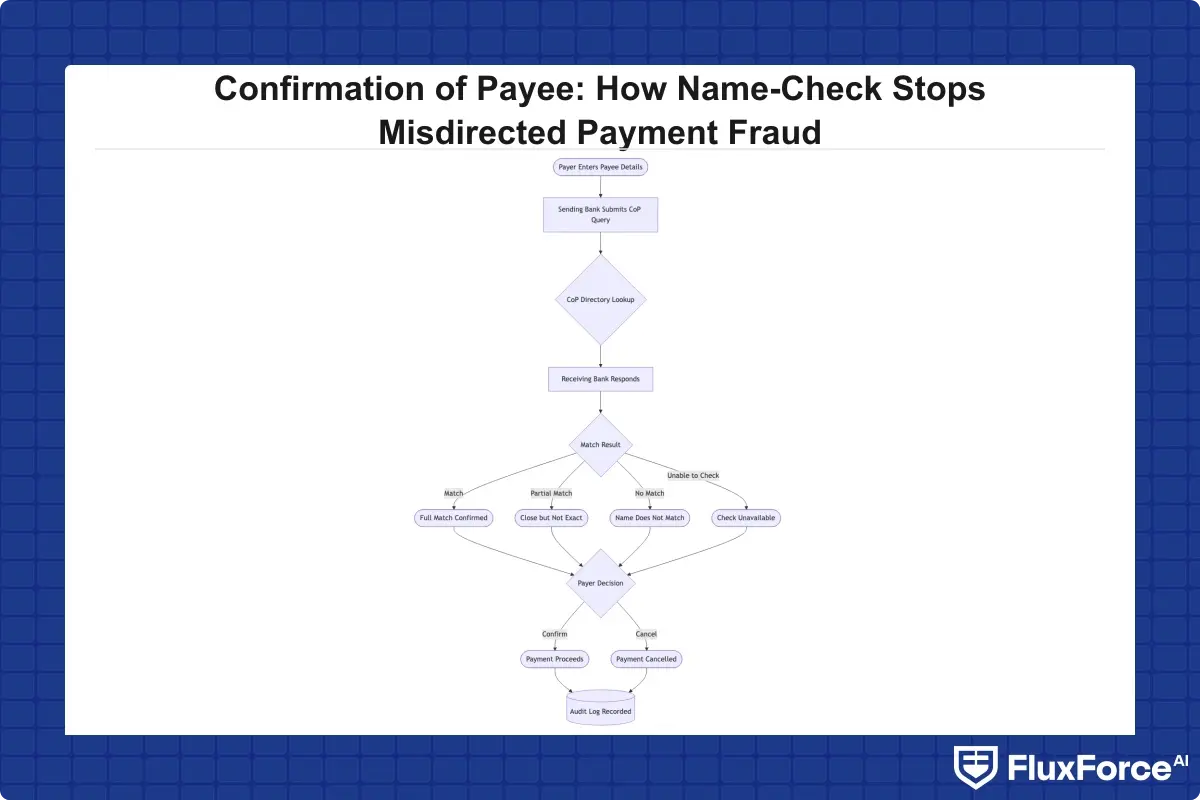

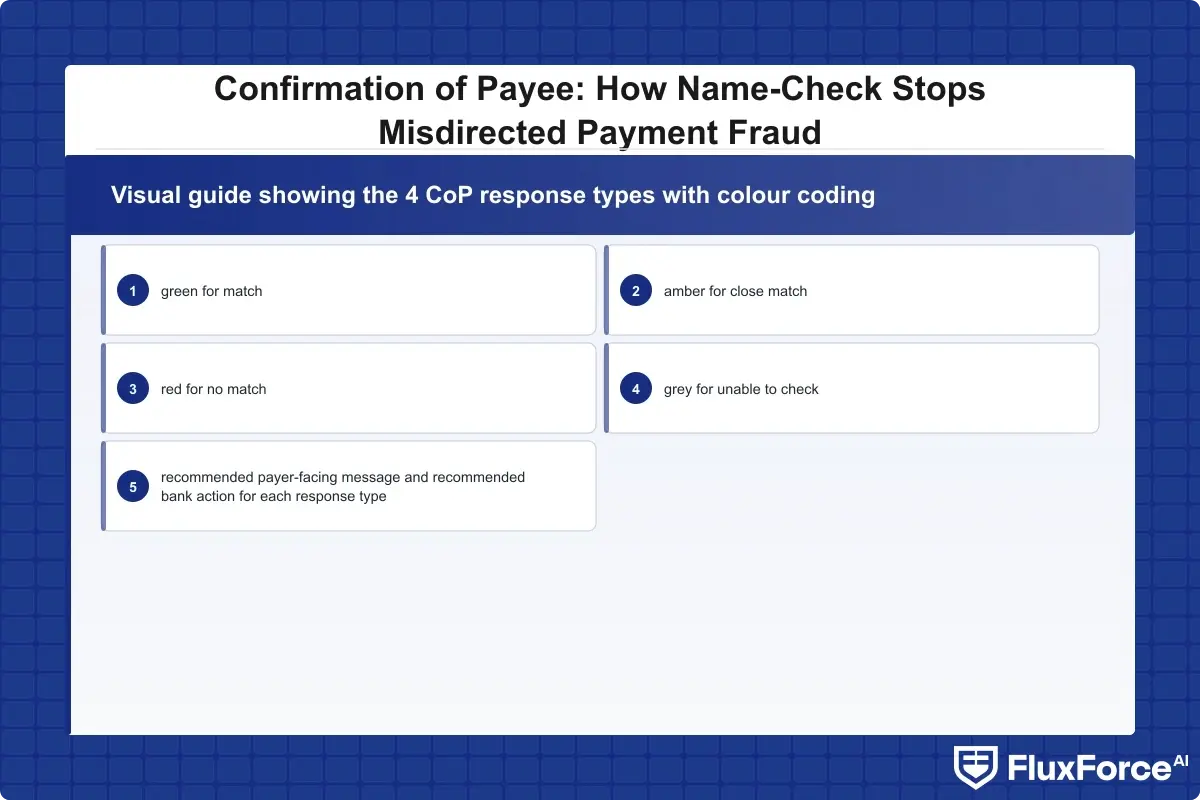

CoP runs over the infrastructure operated in the UK by Pay.UK's CoP service. When a payer submits account details in their bank's interface, the sending bank fires a lookup against the CoP directory, which routes the query to the receiving bank. The receiving bank compares the submitted name against its records and returns one of four results: match, close match, no match, or unable to check. The entire exchange is designed to complete in under two seconds.

Step-by-Step: The Name-Check Request Lifecycle

- Payer enters payee sort code, account number, and account name in the payment interface.

- Sending bank sends a CoP request to the Pay.UK central directory.

- Directory routes the request to the receiving bank.

- Receiving bank runs a fuzzy name-matching algorithm against its account records.

- Receiving bank returns match, close match, no match, or unable to check.

- Sending bank presents the result to the payer with a risk-appropriate message.

- Payer confirms or cancels the payment; both outcomes are logged for compliance purposes.

Anything slower than two seconds degrades the payment experience and generates customer complaints, so latency management is a live operational concern, not just a build-time requirement.

Partial Matches and Edge Cases in Name Verification

Close matches are where the complexity lives. A customer named "Robert Johnson" might have an account registered as "Bob Johnson." A business might trade as "Acme Consulting" but hold accounts in "Acme Consulting Ltd." The fuzzy matching logic must handle these cases without either blocking legitimate payments or passing fraudulent ones. The hit rate for partial matches at large UK banks runs between 8% and 15% of all CoP lookups, based on industry estimates from payment operations teams. Each partial match requires a human-readable explanation to the customer, creating both a UX challenge and a compliance documentation requirement that many institutions underestimated during initial deployment.

The hit rate for partial matches at large UK banks runs between 8% and 15% of all CoP lookups, based on industry estimates from payment operations teams.

Confirmation of Payee Fraud Prevention: Where AI Takes Over

The name-match result is a binary signal. Confirmation of payee fraud prevention becomes genuinely effective when that signal is fed into a broader AI scoring model that weighs account behaviour, payment pattern, and beneficiary history alongside the name-check result. Rule-based approaches simply cannot make this contextual judgement at speed.

AI Fraud Detection Explained: What the Models Actually Do

AI fraud detection explained in the context of CoP means taking the CoP response as one feature among dozens in a real-time risk score. A payment to an account that returns "close match" from CoP combined with a first-time payee flag, an unusual payment amount, and an out-of-pattern time-of-day signal scores very differently from the same "close match" on a regular payroll transfer to a long-established beneficiary.

This is the core of machine learning fraud detection: the model learns which combinations of signals predict fraud versus legitimate close-match payments, and scores new transactions accordingly. Rule-based systems cannot do this. They treat every close match the same way, which is why they generate so many unnecessary alerts and why analysts quickly develop the kind of desensitisation that lets real fraud slip through.

How Does AI Detect Fraud in Real-Time Banking Environments?

How does AI detect fraud in a live payment flow? The model runs at the moment the CoP result is returned, before the payer confirms. It ingests the CoP result, enriches it with account-level features from the transaction monitoring layer (spending history, device fingerprint, session behaviour), and outputs a probability score. High-scoring transactions can trigger step-up authentication, a call-centre alert, or an outright hold. Low-scoring transactions proceed with a standard warning message.

For banks evaluating AI fraud detection in banking, the key metric is not just detection rate but false positive rate. An AI model that blocks 95% of fraud but also blocks 10% of legitimate payments will destroy customer trust faster than it stops fraud losses, which is why model calibration on institution-specific data matters more than off-the-shelf accuracy claims.

An AI model that blocks 95% of fraud but also blocks 10% of legitimate payments will destroy customer trust faster than it stops fraud losses, which is why model calibration on institution-specific data matters more than off-the-shelf accuracy claims.

AI Fraud Detection Software and the CoP Integration Point

Integrating CoP with purpose-built AI-powered fraud detection software requires an API architecture that can receive the CoP response in real time and pass it to the scoring model within the sub-second window available before the payer sees the result. The technical requirement is low latency: the AI model must return a score in under 200 milliseconds to stay within the two-second total CoP round-trip target. Any solution that cannot meet this latency threshold degrades to a post-payment review tool rather than a pre-payment prevention control.

False Positives and the Cost of Getting Name-Checks Wrong

False positive rate fraud detection is the metric that determines whether a CoP deployment is operationally sustainable. Every false positive is a legitimate payment blocked or a customer subjected to an unnecessary friction step. At scale, even a 1% false positive rate across millions of daily payments generates tens of thousands of unnecessary interventions per day, each one costing analyst time, customer service handling, and goodwill.

At scale, even a 1% false positive rate across millions of daily payments generates tens of thousands of unnecessary interventions per day, each one costing analyst time, customer service handling, and goodwill.

How to Reduce False Positives in AML and Name-Check Workflows

How to reduce false positives in AML when CoP is in scope starts with improving the name normalisation logic before the match is even attempted. Names with common abbreviations, honorifics, or Unicode characters create noise that the fuzzy matcher cannot resolve cleanly. Standardising input names against a canonical form before sending the CoP query reduces unnecessary close-match results without changing the fundamental check.

Beyond input quality, reduce false positives in transaction monitoring by contextualising the CoP result. A "no match" against a first-time beneficiary in a high-risk category should score differently from a "no match" on a payee the customer has paid successfully 30 times in the past. Transaction monitoring software that maintains beneficiary relationship history can provide this context automatically, removing the need for an analyst to manually check payment history on every flagged transaction.

Fraud Alert Fatigue: What Happens When Too Many Checks Fire

Fraud alert fatigue is the operational equivalent of crying wolf. When analysts receive too many alerts that turn out to be false positives, they start approving them faster and less carefully. Research consistently shows that analysts who review more than 400 alerts per day have significantly lower true positive identification rates than those reviewing fewer than 150. The agentic AI approach to cutting false positives addresses this directly by filtering low-risk alerts before they reach human reviewers, keeping analyst queues focused on genuinely ambiguous cases.

This is not a theoretical concern. Several UK banks reported during the initial CoP rollout that the volume of close-match alerts overwhelmed their fraud operations teams in the first weeks of deployment, forcing them to either relax alert thresholds or hire additional headcount. Neither outcome is acceptable at steady state.

False Positive Cost Fraud: The Numbers That Change Boardroom Conversations

False positive cost fraud is underreported because it sits in operational budgets rather than fraud loss lines. A conservative estimate for a mid-size UK bank processing 500,000 daily payments puts the annual cost of CoP-related false positives at between £2 million and £5 million in analyst time, customer service calls, and payment delays. That cost rises sharply if the false positive rate is not actively managed through smarter models.

The comparison between rule-based systems and AI-driven solutions for false positive reduction consistently shows AI models reducing false positives fraud detection rates by 40% to 80% in production environments when properly trained on institution-specific data. The investment in model development is almost always recovered within the first year of operation.

Real-Time Fraud Detection: Integrating CoP With Transaction Monitoring

Real-time fraud detection banks need is not just a name-check in isolation. It is a coordinated signal from CoP, account-level behavioural analysis, and network-level mule detection, all resolved within the payment authorisation window. Getting these systems to talk to each other in real time is the integration challenge that separates a CoP deployment that reduces fraud from one that merely demonstrates regulatory compliance.

Transaction Monitoring Software Requirements for CoP Integration

Transaction monitoring software used alongside CoP must expose a real-time API endpoint. Batch-mode systems that process transactions overnight cannot contribute to pre-payment decisions. The integration pattern is: CoP result arrives, transaction monitoring API called with account ID and CoP result as parameters, transaction monitoring returns risk score, combined score fed to decision engine.

When comparing transaction monitoring platforms, including widely-benchmarked pairs like Sardine vs Unit21 or established enterprise systems, real-time API support and CoP result ingestion are the features that separate viable from non-viable options for pre-payment risk scoring. A platform that cannot ingest a CoP response as a live event is effectively a post-payment audit tool, regardless of how sophisticated its ML models are.

Automated Transaction Monitoring and CoP: A Combined Workflow

Automated transaction monitoring in this context means the transaction monitoring system acts autonomously on most decisions, escalating only genuinely ambiguous cases to human analysts. A CoP "no match" combined with a high-risk transaction monitoring score triggers an automatic hold. A CoP "match" with a low-risk score proceeds automatically. Only the middle band of cases, where CoP returns "close match" and the transaction monitoring score is in the uncertain range, reaches a human reviewer.

For a detailed view of how real-time fraud detection works across the payment stack, this AI vs. traditional fraud detection overview covers the architectural differences between legacy rule engines and modern ML-based systems that matter when designing the CoP integration layer.

Transaction Monitoring Cost Versus Fraud Loss Avoidance

Transaction monitoring cost is a legitimate concern for every operations head. A system that requires analyst review of every CoP close-match result costs more than the fraud it prevents at low fraud rates. The business case for AI-enriched CoP is that the model handles 80% to 90% of close-match cases automatically, reducing analyst workload to the genuinely complex cases.

When evaluating vendors, including options in the Sardine vs Unit21 tier and enterprise alternatives, the per-transaction monitoring cost must be weighed against the analyst headcount reduction that automated decisioning delivers. The transaction monitoring cost calculation then shifts from a linear "alerts per analyst" model to a tiered model where AI handles volume and humans handle judgement, which almost always produces a better unit economics outcome.

What Banks and Fintechs Must Get Right Before Deployment

Getting CoP live is not just a technical task. The operational and data requirements are where most deployments run into delays, and where institutions that cut corners during implementation pay the price in elevated false positive rates and regulatory scrutiny six months later.

Data Quality and Name Standardisation

The receiving bank's name records are only as reliable as the onboarding data collected at account opening. If the account name field was populated inconsistently (sometimes first name first, sometimes surname first, sometimes initials), the CoP response will generate excessive close matches and no-matches even for legitimate payers. A data quality audit of account name records is a prerequisite for a reliable CoP service, not an optional follow-on task.

For compliance officers dealing with similar data quality issues in identity verification workflows, the challenges around KYC and AML identity verification for financial institutions follow the same pattern. Bad input data cannot be compensated for by better algorithms; it has to be fixed at source before the matching layer will perform reliably.

API Design and Payment Fraud Prevention at Scale

At high payment volumes, the CoP lookup adds latency. The architecture must handle peak load without degrading the payment experience. Most UK banks now run CoP over asynchronous APIs with fallback handling: if the CoP response takes longer than 1.5 seconds, the payment proceeds with a customer-visible warning that the check could not be completed. This is a regulatory risk that needs to be documented and managed, not silently accepted as a performance limitation.

Payment fraud prevention at scale also means logging every CoP result and the subsequent payer decision. A customer who receives a "no match" warning and proceeds anyway is a data point. If that payment later results in a fraud report, the decision trail matters both for reimbursement disputes and for model retraining. Institutions that log CoP outcomes systematically build a proprietary dataset that improves model accuracy over time. Those that discard the data are leaving their most valuable training signal on the floor.

- Confirmation of payee (CoP) is a real-time name-verification service that checks whether the name a payer enters matches the name held against the destination account at the receiving bank.

- Payment fraud prevention starts with understanding the loss pathways.

- CoP runs over the infrastructure operated in the UK by Pay.UK's CoP service.

- The name-match result is a binary signal.

- False positive rate fraud detection is the metric that determines whether a CoP deployment is operationally sustainable.

Onboard Customers in Seconds

Conclusion

Confirmation of payee fraud prevention is one of the clearest examples of a control that is straightforward to mandate but technically difficult to execute well. The name-check itself is table stakes. The real work is in the AI layer that interprets the result in context, the data quality foundation that makes name matches reliable, and the transaction monitoring integration that turns CoP from a yes/no signal into a risk-weighted decision.

Banks and fintechs that treat CoP as a compliance checkbox will find that their false positive rates erode customer trust and their fraud losses remain high. Those that build CoP into a coherent, AI-enriched payment fraud prevention architecture will see both outcomes improve. The technology to do this is available today; the challenge is the integration discipline and the organisational commitment to maintaining model quality as fraud patterns evolve. Start with the data quality audit, design the real-time API integration before procuring software, and set false positive rate targets alongside fraud detection rate targets from day one.

Share this article