.webp)

Introduction

Configurable ai autonomy banking has become one of the most consequential decisions risk leaders are navigating this year. Banks, fintechs, and insurers are deploying AI at scale, but the question keeping CISOs and compliance officers up at night isn't whether AI works. It's how much decision-making authority to grant it, in which contexts, and with what safeguards in place. Get this wrong and you're either over-relying on black-box decisions that regulators will question, or under-using AI in ways that leave your fraud and compliance operations reactive. This post breaks down what a configurable autonomy model looks like in practice, why platform consolidation is central to making it work, and how explainability requirements should shape your architecture from day one.

- Why Configurable AI Autonomy Banking Requires a Tiered Approach

- The Hidden Cost of Point Solutions vs Platform Financial Services

- What Does Configurable AI Autonomy Actually Mean?

- How Human in the Loop AI Banking Actually Works

- Why Explainable AI Compliance Is Non-Negotiable for Regulators

Onboard Customers in Seconds

Why Configurable AI Autonomy Banking Requires a Tiered Approach

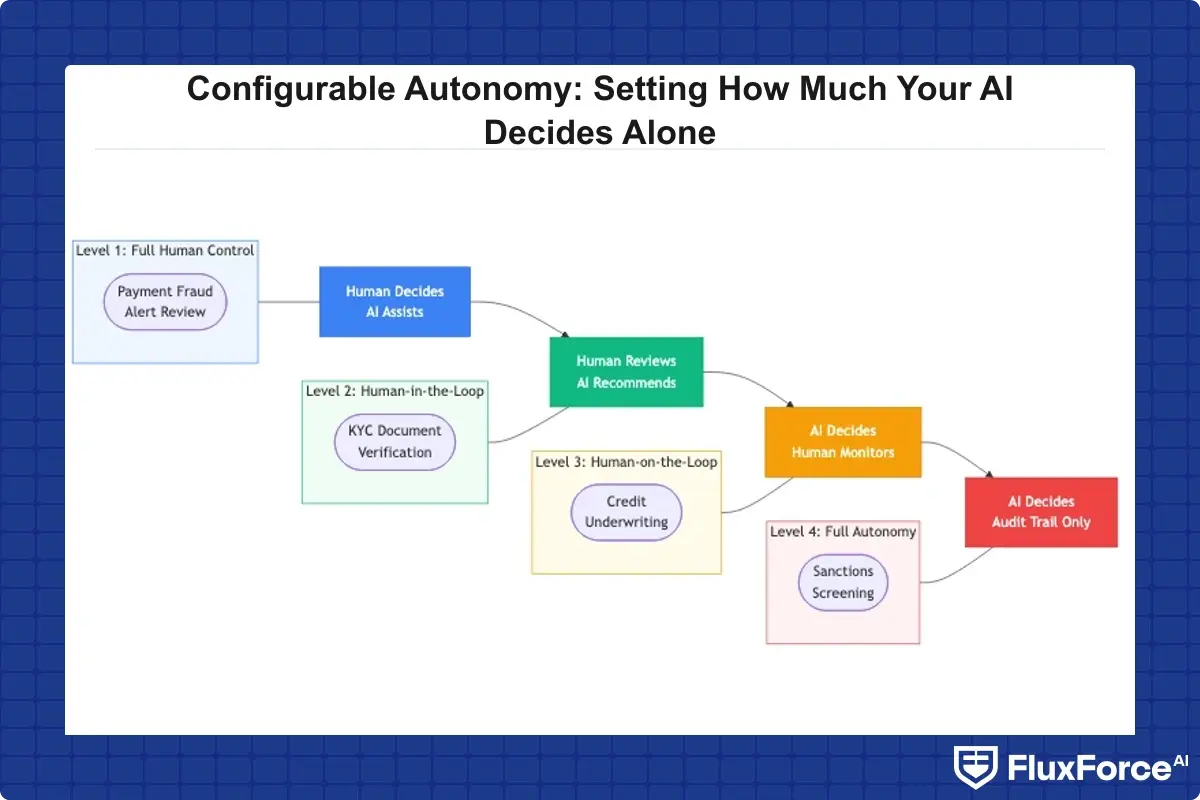

Financial institutions operate across use cases where the stakes, speed requirements, and regulatory scrutiny differ significantly. Real-time payment fraud requires sub-second decisions on millions of transactions per day. Sanctions screening operates under strict regulatory guidance where human review is often mandated. Credit underwriting sits somewhere in between: AI can inform the decision, but regulators increasingly demand that the reasoning is auditable.

A single autonomy level won't work across all these contexts. The right framework treats configurable ai autonomy as a dial, not a switch.

The Spectrum from Rule-Based to Fully Autonomous

At one end, rule-based systems offer static thresholds, deterministic outputs, and human review for every flagged case. They're auditable but slow. At the other end, fully autonomous AI agents handle millions of events per second but create accountability challenges that regulators aren't comfortable with in high-risk contexts.

A risk-stratified approach means low-risk transactions get straight-through AI processing, medium-risk cases trigger AI recommendations with analyst review, and high-risk cases escalate automatically. The challenge is configuring those thresholds correctly and keeping them auditable across the entire risk lifecycle.

Why Regulatory Pressure Complicates Full Automation

Regulators in the EU, UK, and US have all signaled concerns about opaque AI decision-making in financial services. The NIST AI Risk Management Framework explicitly calls out the need for human oversight and accountability in high-stakes AI systems. The European Banking Authority's internal governance guidelines require that institutions can explain how their models reach decisions during supervisory examination.

Even where full automation is technically feasible, the regulatory cost often outweighs the operational benefit. Configurable ai autonomy banking, properly implemented, lets you automate where it's safe while maintaining the human-in-the-loop controls that regulators expect.

The Hidden Cost of Point Solutions vs Platform Financial Services

Most financial institutions built their fraud, compliance, and identity stacks incrementally. One vendor for transaction monitoring. Another for KYC. A third for sanctions screening. The result is a fragmented architecture where data doesn't flow naturally between systems and configuring autonomy consistently across the stack is practically impossible.

This is the core problem with point solutions vs platform financial services. It isn't just an IT efficiency question. It's a risk management problem that directly limits how much you can trust your AI.

When Fragmentation Becomes a Risk Factor

When your fraud detection system flags a suspicious transaction but can't cross-reference it against your identity verification records or sanctions watchlist, you're creating manual handoffs where fraud slips through. According to the Bank for International Settlements, fragmented risk infrastructure is a primary contributor to operational risk events at financial institutions.

Each integration point between point solutions is a potential data loss or governance gap. When a regulator asks how a specific high-value transaction was flagged and resolved, you want a single audit trail, not log files from five different vendors.

How an AI Security Operations Platform Changes the Calculation

An ai security operations platform consolidates fraud detection, compliance monitoring, and identity verification into a single data model. The AI has complete context when making decisions, and autonomy levels apply consistently across the entire risk lifecycle rather than within a single isolated tool.

This is where vendor consolidation fintech strategies become operationally meaningful beyond cost savings. You're reducing the seams in your risk architecture where attacks and compliance failures hide, and building the data foundation that makes configurable ai autonomy banking enforceable in practice.

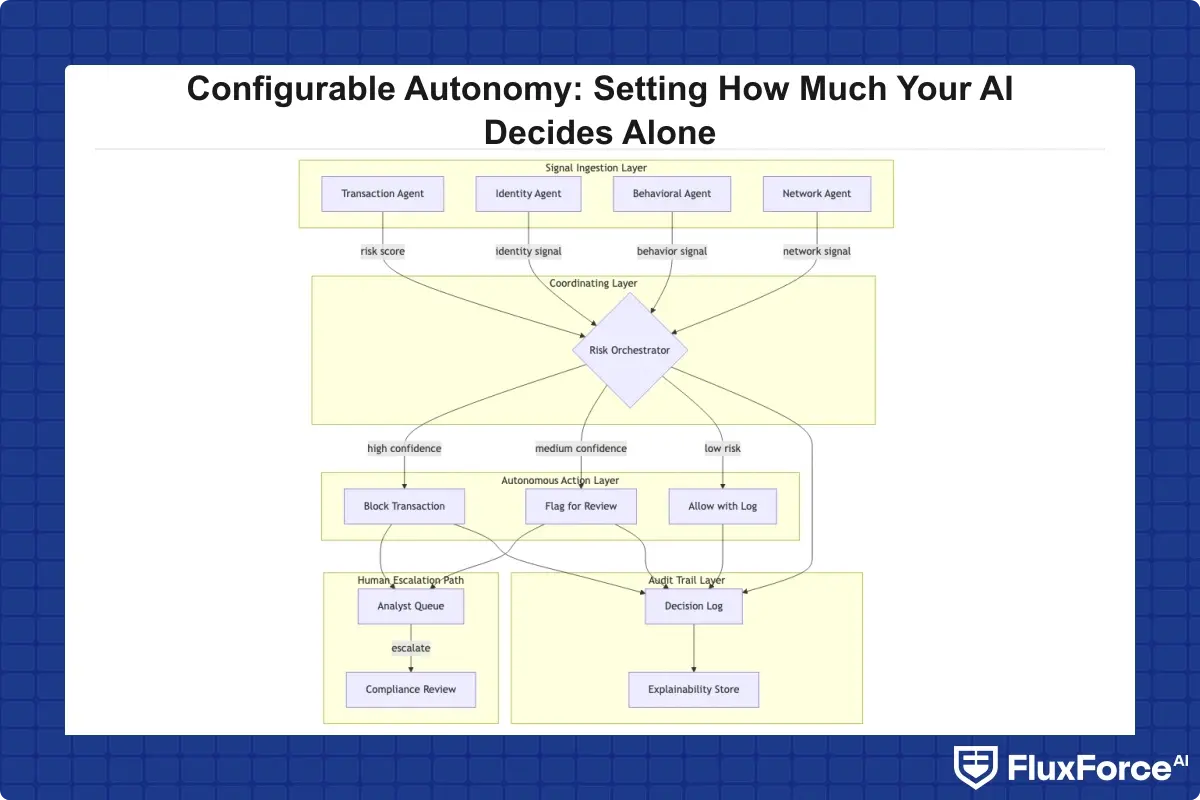

What Does Configurable AI Autonomy Actually Mean?

Configurable ai autonomy means the institution can set, per use case and risk tier, the conditions under which AI acts independently versus defers to human judgment. This isn't a toggle in a dashboard. It's a governance framework embedded in the architecture and documented for regulators.

AI Agents Financial Services: Scoping Their Mandate

AI agents financial services deployments are increasingly common, but the best implementations are precise about mandate definition. An AI agent for payment fraud screening might automatically block transactions above a certain risk score, auto-approve those below a low-risk threshold, and queue the middle band for human review.

A multi agent ai system adds another layer. Specialized agents handle different risk signals: behavioral analytics, device fingerprinting, network graph analysis. A coordinating agent synthesizes their outputs into a single risk assessment. Each agent has a defined scope and doesn't act outside it without escalation, which improves accuracy meaningfully over single-model approaches.

Thresholds, Triggers, and Human Override Protocols

Good configurable autonomy design specifies three things: the confidence threshold at which AI acts alone, the triggers that force human review regardless of score, and the override protocol when humans disagree with the AI recommendation.

Override protocols matter more than most teams realize. If analysts routinely override AI decisions without logging their reasoning, you lose the feedback loop that improves the model. If overrides require too much friction, analysts stop doing them and the AI's blind spots never get corrected.

How Human in the Loop AI Banking Actually Works

Human in the loop ai banking can mean anything from "a human sees every decision" to "a human can intervene if they choose to." The practical definition depends on the use case and regulatory environment.

For most regulated financial institutions, the right model is tiered: automated for low-risk cases, AI-assisted for medium-risk, and human-led with AI support for high-risk cases. The hard part is defining those tiers accurately and recalibrating them as fraud patterns evolve.

Designing the AI Audit Trail Automation Layer

Every decision needs an ai audit trail automation layer capturing what the AI saw, what it decided, what a human did, and why. Regulators treat the audit trail as the primary evidence of responsible AI governance, and a fragmented trail is a material finding during examination.

The audit trail also has direct operational value. When a fraud pattern emerges that your models missed, you need to trace which cases were auto-approved and what signals were present. Without structured audit logging, that analysis takes weeks. With it, it's a query.

As explored in Manual Compliance vs. AI Automation: Pros, Cons, and Best Practices, institutions that handle this well treat automation as a structured extension of human judgment rather than a replacement for it.

When to Override, Escalate, or Accept the Decision

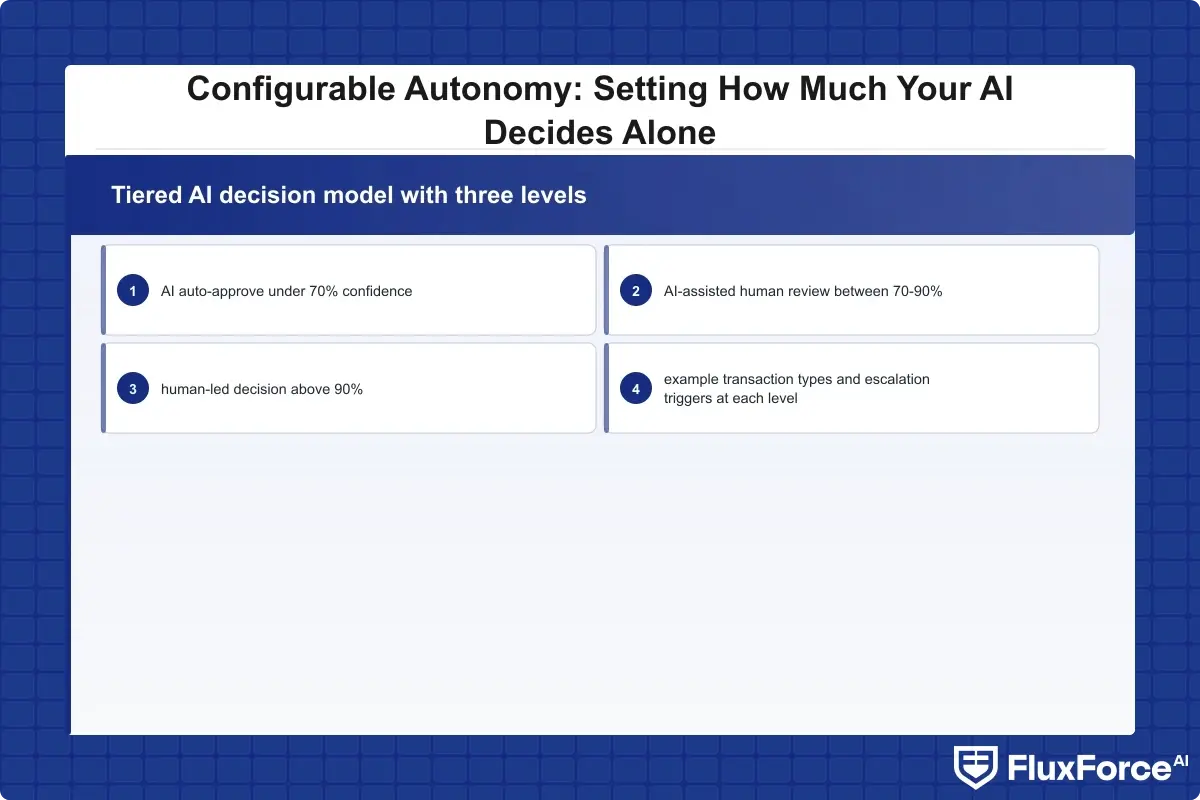

A well-designed system makes escalation logic explicit. Above 90% confidence: automatic block and queue for analyst review. Between 70-90%: flag for attention but allow the transaction to proceed with monitoring. Below 70%: approve and log. These thresholds need quarterly review. Fraud tactics evolve, and what looks like a high-risk pattern today might be normalized behavior in six months.

Above 90% confidence: automatic block and queue for analyst review.

Why Explainable AI Compliance Is Non-Negotiable for Regulators

Many banks build sophisticated AI models that perform well on accuracy metrics, then discover during a regulatory examination that they can't explain how those models reach their decisions. Explainable ai compliance isn't a feature you add later. It's a design constraint that needs to be set before the first model goes into production.

The European Banking Authority has published guidelines requiring that credit and risk models be interpretable by supervisors. Similar guidance from FinCEN and the OCC reflects an increasing expectation that explainable ai finance practices are documented and demonstrable, tied to specific model outputs rather than described only in policy documents.

The Black Box AI Compliance Risk Is Real

Black box ai compliance risk is straightforward: if your model makes a decision and nobody can explain why, you have a governance problem regulators will find. In fraud detection, that might mean a legitimate customer gets blocked with no explainable basis. In credit underwriting, it might mean a loan denial that can't be defended against a discrimination claim.

If your analysts can't understand why the AI is flagging cases, they can't calibrate their reviews effectively. They start treating AI recommendations as either gospel or noise, both of which erode the value of your AI investment over time.

SHAP Values Explained for Regulators

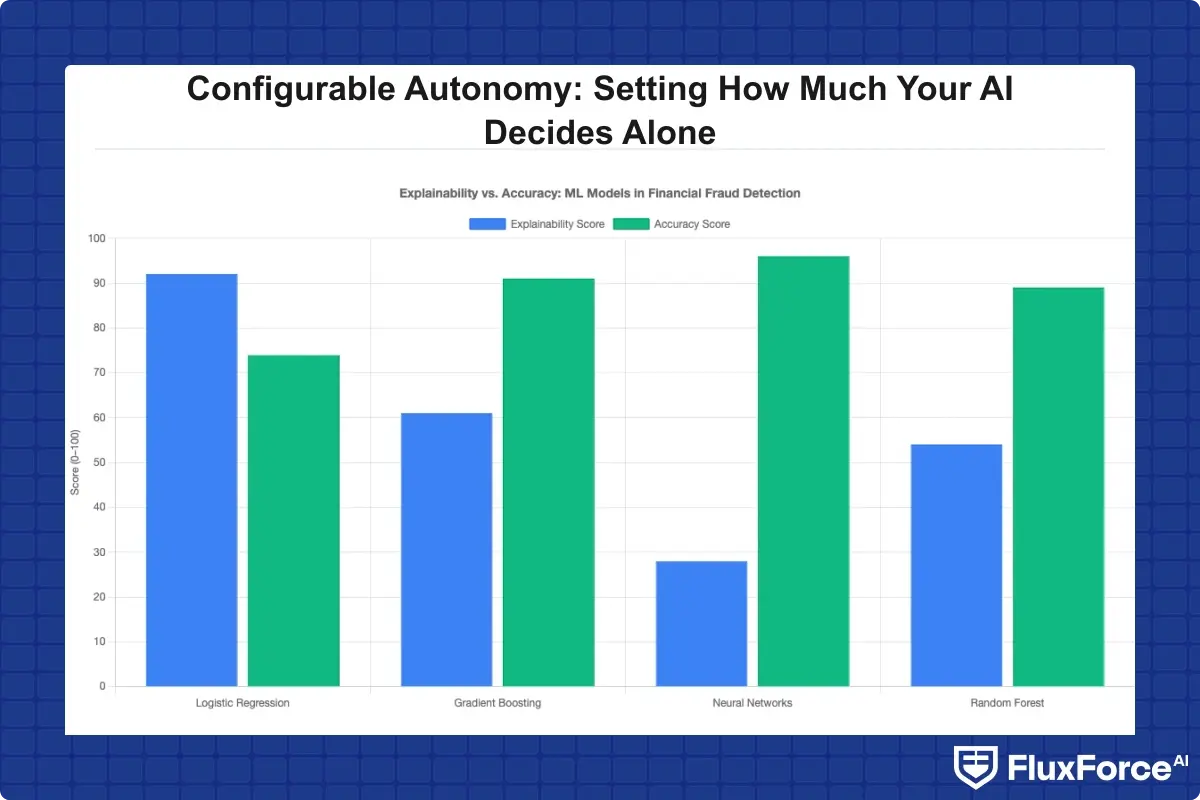

AI model explainability is what regulators want documented: concrete evidence of which factors drove a specific decision, not abstract architecture diagrams. SHAP values explained regulators is one of the most common topics compliance teams raise when implementing explainable AI. SHAP (SHapley Additive exPlanations) assigns each input feature a contribution score for a specific prediction. For a fraud detection model, it can show that device mismatch contributed 40% of the risk score, the unusual merchant category 30%, and the transaction timing 20%.

For a fraud detection model, it can show that device mismatch contributed 40% of the risk score, the unusual merchant category 30%, and the transaction timing 20%.

That output gives analysts something concrete to work with and gives regulators something concrete to examine. The answer to "why did your model flag this transaction?" becomes a structured, defensible explanation.

XAI Fraud Detection in Practice

XAI fraud detection implementations that work well share one characteristic: explainability is built into model selection from the start, not retrofitted after deployment. Teams that try to add explainability after the fact often find that their highest-performing models are also the least interpretable.

The practical approach is to evaluate models on a combined metric: predictive performance plus explainability score. A model that is 97% accurate but uninterpretable may be less operationally valuable than one at 94% accuracy that produces SHAP outputs regulators can work with. For a detailed look at how these tradeoffs play out, AI vs. Traditional Fraud Detection: Key Differences Every Risk Officer Should Know covers the practical implications across model types.

A model that is 97% accurate but uninterpretable may be less operationally valuable than one at 94% accuracy that produces SHAP outputs regulators can work with.

How a Unified Risk Platform Enables Configurable Autonomy

The architecture argument for a unified risk platform comes down to control. When fraud detection, compliance screening, and identity verification live in a single platform, you configure AI autonomy consistently and monitor it from one interface. When they live in separate systems, every change to your autonomy settings requires coordination across multiple vendor roadmaps and coverage gaps are almost guaranteed.

A fraud compliance identity platform that integrates these functions gives risk teams a single place to set thresholds, review AI decisions, manage exceptions, and generate the audit evidence that regulators expect.

Fraud Compliance Identity Platform: One View, One Control Layer

The practical advantage of a consolidated fraud compliance identity platform shows up most clearly during regulatory examinations. Instead of pulling data from three or four systems and reconciling them, your team generates a complete case history from a single interface. AI decisions, human review notes, outcome data, and model versions all live in the same record.

This also simplifies the internal governance conversation. When your CISO and chief compliance officer need to agree on autonomy thresholds for a new product launch, they're working from the same data model with the same risk signals rather than comparing outputs from incompatible systems.

Vendor Consolidation Fintech: Fewer Seams, Fewer Risks

Vendor consolidation fintech has gained momentum not just for cost reasons but because reducing integration complexity directly reduces your risk surface. Every API call between separate systems is a potential failure point, a latency issue, or a data fidelity problem.

From a configurable autonomy standpoint, consolidation means your AI models access richer, more complete data. A fraud model that can see KYC status, transaction history, device profile, and behavioral analytics simultaneously will outperform one that sees only transaction data, regardless of model architecture. The right fraud detection software handles all of these signals in a unified context rather than forcing your team to stitch together outputs from separate tools.

Teams dealing with AML and identity verification at scale, like those described in AML Screening in Digital Lending: KYC/AML & Identity Verification Strategy for Payments Risk Officers, consistently find that platform consolidation is a prerequisite for making configurable autonomy work in practice.

Multi-Agent AI System Design for Banking Fraud Detection

Multi agent ai system design is where configurable autonomy gets genuinely complex. In a single-model setup, you configure one system's decision thresholds. In a multi-agent setup, you configure the autonomy of each individual agent, the handoff rules between agents, and the coordinating layer that synthesizes their outputs.

The upside justifies the complexity. Production deployments using this approach have shown false positive reductions of up to 80% compared to rule-based systems, as documented in FluxForce's analysis of agentic AI fraud agents in production environments.

AI Agent Fraud Detection: How Agents Coordinate

In a well-designed ai agent fraud detection system, each agent has a defined input scope, an output format that feeds the coordinating layer, and a confidence threshold that determines whether it passes a recommendation upward or escalates for human review. The coordinating agent synthesizes individual agent outputs, weights them by historical accuracy for the case type, and produces a final risk assessment.

The configurable autonomy question here is: at what combined confidence score does the system act without human review? That threshold should differ by transaction value, customer segment, and product type. A $50 card payment can tolerate more automation than a $500,000 wire transfer.

Building Guardrails into Multi-Agent AI Systems

Guardrails in a multi agent ai system prevent agents from acting outside their defined mandate, even when confidence scores are high. This includes rate limits on automated actions, mandatory human review for specific case types regardless of score, and circuit breakers that pause automated processing when anomaly rates spike above baseline.

These guardrails need to be configurable in the same interface as your autonomy thresholds. If your security team identifies a new fraud vector on a Friday afternoon, you want to adjust the relevant guardrail within minutes, not wait for a deployment cycle. The Zero Trust + Agentic AI: The New Normal for Banking Security framework shows how access controls and agent mandates interact in a production system.

- Financial institutions operate across use cases where the stakes, speed requirements, and regulatory scrutiny differ significantly.

- Most financial institutions built their fraud, compliance, and identity stacks incrementally.

- Configurable ai autonomy means the institution can set, per use case and risk tier, the conditions under which AI acts independently versus defers to human judgment.

- Human in the loop ai banking can mean anything from "a human sees every decision" to "a human can intervene if they choose to." The practical definition depends on the use case and regulatory environment.

- Many banks build sophisticated AI models that perform well on accuracy metrics, then discover during a regulatory examination that they can't explain how those models reach their decisions.

Onboard Customers in Seconds

Conclusion

Configurable ai autonomy banking is not a product you buy. It's an architecture you design, a governance model you enforce, and a calibration process you run continuously. The institutions getting this right share three characteristics: they've consolidated their risk stack onto a unified risk platform that gives AI complete data context; they've built explainable ai compliance into their models from the start rather than retrofitting it; and they've designed human-in-the-loop controls that are specific, auditable, and calibrated to regulatory expectations.

The shift from point solutions vs platform financial services isn't just about operational efficiency. A consolidated fraud compliance identity platform is the infrastructure prerequisite for making configurable autonomy real. Without a unified data model, consistent AI governance across fraud, compliance, and identity simply isn't achievable.

If your team is working through how to set AI decision thresholds that satisfy both operational requirements and regulatory scrutiny, start with three things: your audit trail architecture, your explainability framework, and your escalation logic. Those three elements determine whether your configurable ai autonomy banking implementation holds up under examination or falls apart at the first supervisory review.

Share this article