.webp)

Listen To Our Podcast🎧

Introduction

Building a compliance culture financial institution leaders can rely on starts long before the first policy is written or the first SAR is filed. Most compliance failures in banking don't trace back to missing software or outdated rules. They trace back to people who saw something suspicious, weren't sure what to do, and stayed quiet. Culture is the gap between what your policies say and what your team actually does at 4pm on a Friday.

This post walks through what a compliance-first culture actually looks like in practice, covering everything from the foundational BSA/AML compliance checklist that satisfies regulators to the KYC automation tools that make daily due diligence manageable. If you run a regional bank, a fintech startup, or a credit union with a small compliance team, the principles here apply directly to your operation.

- What Does a Compliance-First Culture Mean for Financial Institutions?

- The BSA/AML Compliance Checklist Every Institution Needs

- How AML Compliance Software Accelerates Compliance at Financial Institutions

- SAR Filing Efficiency: From Manual Process to Automated System

- KYC Automation and CDD Requirements in 2026

Onboard Customers in Seconds

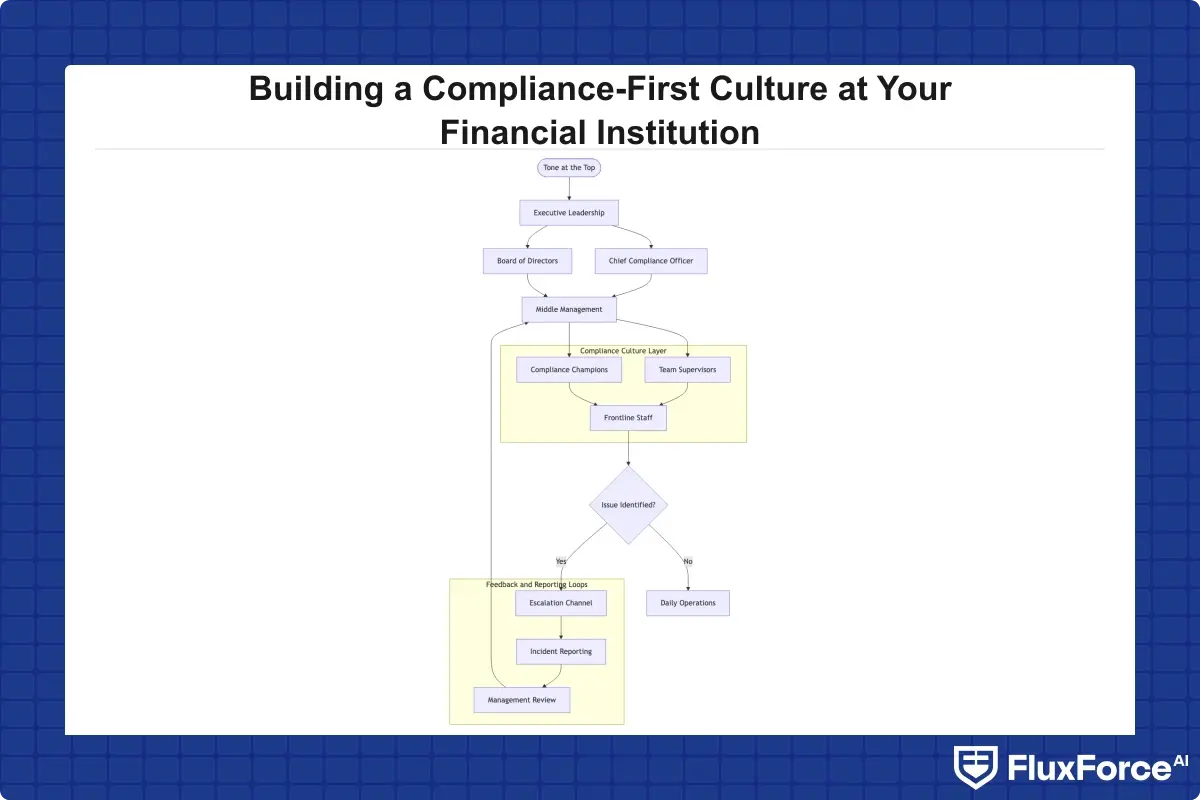

What Does a Compliance-First Culture Mean for Financial Institutions?

A compliance culture financial institution environments need is one where compliance is treated as an operational standard rather than a legal obstacle. The difference shows up in how teams handle edge cases: does a frontline employee escalate a suspicious transaction, or does the customer leave and the moment pass?

According to the Financial Crimes Enforcement Network (FinCEN), financial institutions must establish internal controls, conduct independent testing, train personnel, and designate a compliance officer, the four pillars of a BSA/AML program. These pillars are administrative. Culture is what makes them functional.

Why Tone at the Top Drives AML Compliance

Senior leadership sets the signal. If your Chief Compliance Officer is treated as a cost center and compliance questions get bumped from board meetings, your team notices. Institutions where the CEO references aml compliance outcomes in all-hands meetings, not just during exam prep, consistently score better on regulatory reviews.

Concrete signals matter more than mission statements. Promote someone who flagged a compliance issue even when it disrupted a sales target. Build compliance metrics into performance reviews, not just risk assessments.

How Middle Management Becomes the Compliance Multiplier

Middle managers are where compliance culture either takes root or stalls. A branch manager who responds to employee questions with "just process it, we'll deal with it later" effectively overrides your entire policy framework. Training middle managers on escalation procedures and the personal liability implications of BSA/AML violations changes this dynamic significantly.

One regional bank reduced its suspicious activity report (SAR) backlog by 34% after implementing a manager-specific compliance training track separate from general employee training. The difference wasn't technology. It was accountability at the supervisory level.

One regional bank reduced its suspicious activity report (SAR) backlog by 34% after implementing a manager-specific compliance training track separate from general employee training.

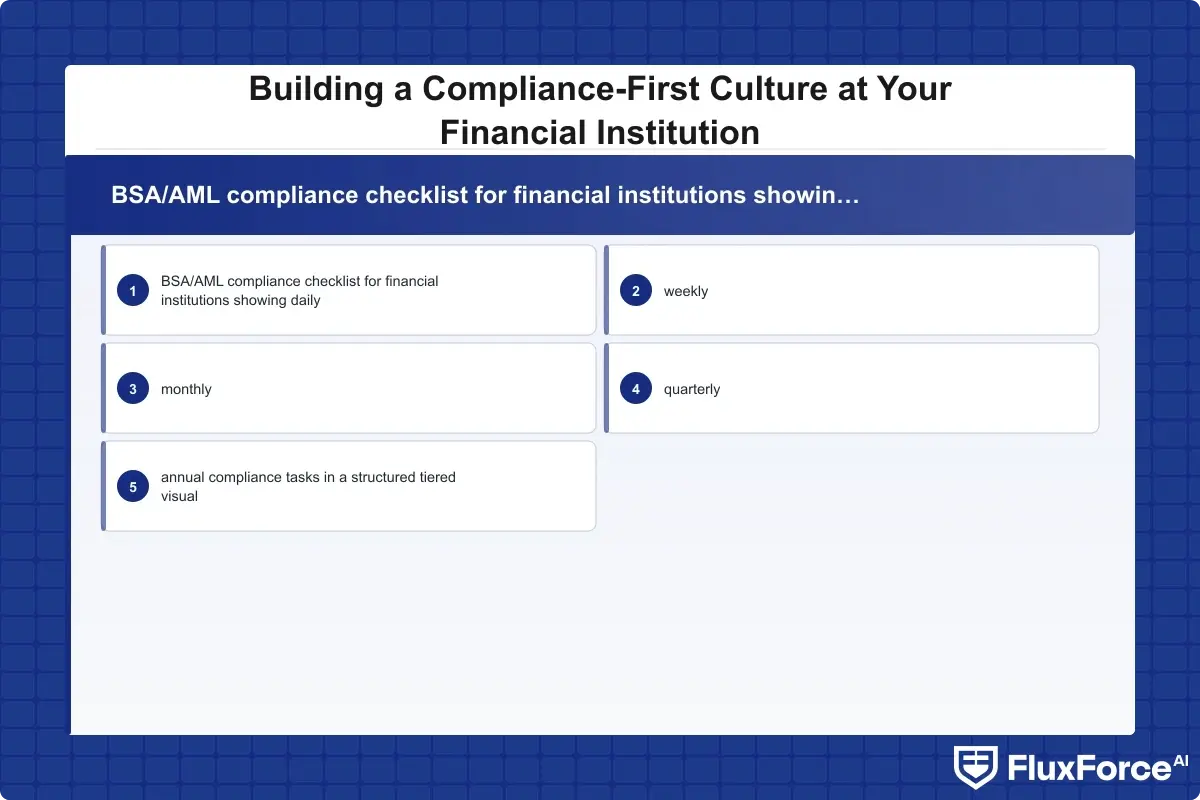

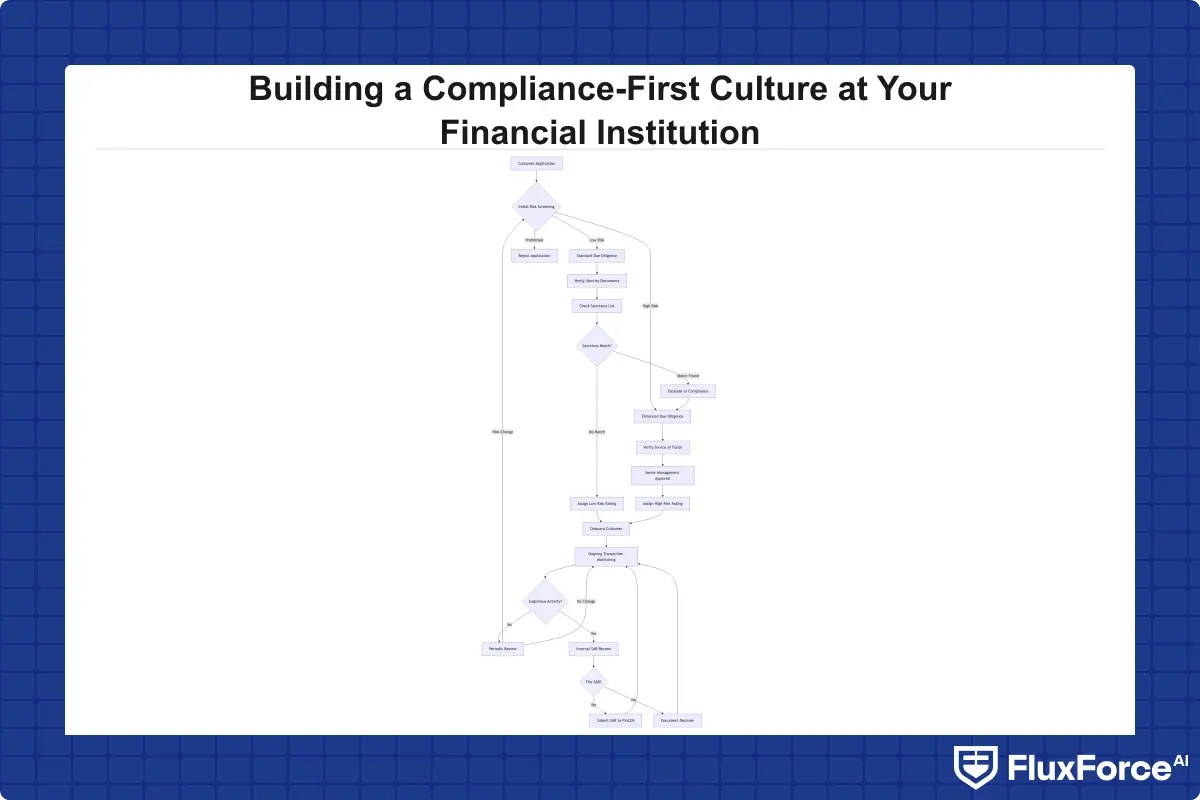

The BSA/AML Compliance Checklist Every Institution Needs

A practical bsa aml compliance checklist covers more than what you hand regulators during an exam. It's a living document your compliance team uses to verify that controls are functioning week to week.

The FFIEC BSA/AML Examination Manual provides the framework examiners use. Your internal checklist should map directly to those examination objectives, so there are no surprises when your exam cycle arrives.

BSA AML Compliance for Community Banks

Bsa aml compliance community banks face a specific challenge: they often have one or two compliance staff members covering functions that larger institutions dedicate entire departments to. A rolling daily, weekly, and monthly structure works better at this scale than a single monthly review:

- Daily: Review transaction alerts from your monitoring system. File CTRs for transactions over $10,000 per CTR filing rules. Log any customer due diligence (CDD) updates.

- Weekly: Review open SAR investigations. Check watchlist screening hits. Verify new accounts have completed KYC documentation.

- Monthly: Run independent testing on a sample of alerts. Review risk ratings for high-risk customers. Update the institution risk assessment with any new products or geographies.

- Quarterly: Board or audit committee reporting on AML program metrics. Review training completion rates.

- Annually: Full program audit. Update policies. Refresh the enterprise-wide risk assessment.

This structure keeps nothing stale for long. A finding that would have been minor in week one becomes an exam observation if it sits unreviewed for six months.

Fintech BSA AML Requirements for Small Teams

For a fintech bsa aml small team, often three to five people covering compliance for a payment app or digital lender with hundreds of thousands of users, the checklist focuses on system health rather than individual transactions:

- Are automated alert thresholds calibrated correctly, not generating 95% false positives?

- Is your AML compliance software vendor providing timely model updates as typologies evolve?

- Are SAR decisions documented with sufficient narrative to meet FinCEN requirements?

- Do you have a licensed compliance officer with BSA/AML authority who isn't also your general counsel?

These questions sound basic, but they're exactly what examiners ask first at fintech institutions.

How AML Compliance Software Accelerates Compliance at Financial Institutions

The shift from manual processes to AML compliance software changes what's possible, not just what's faster. A compliance analyst spending six hours reviewing spreadsheet exports from a core banking system can pivot to investigating genuinely suspicious activity when software handles initial triage.

The honest answer about anti money laundering technology is that it doesn't replace judgment. It removes the cases that don't need judgment. Your experienced investigators should be spending time on complex, multi-layered typologies, not clearing alerts for customers who deposit their paycheck every two weeks.

Anti-Money Laundering Technology Features to Look For

When evaluating anti money laundering technology 2026 solutions, the feature set has matured significantly beyond basic transaction monitoring. Current platforms offer:

- Behavioral analytics: Identifies deviations from a customer's established pattern, not just rule-based thresholds

- Network link analysis: Surfaces connections between accounts that individually look clean but collectively show structuring behavior

- Integrated watchlist screening: Combines OFAC, PEP lists, and adverse media in a single workflow rather than separate tools

- Explainable AI outputs: Generates plain-language rationales for alerts, critical for SAR narratives and examiner documentation, increasingly required under the EU AI Act for financial services

- Case management: Tracks every alert from opening to disposition, with full audit trails

This is where regulatory compliance automation becomes a strategic advantage rather than just an operational convenience, when your AML system generates structured SAR data automatically and routes cases to the right analyst, your compliance team's capacity multiplies without headcount growing proportionally.

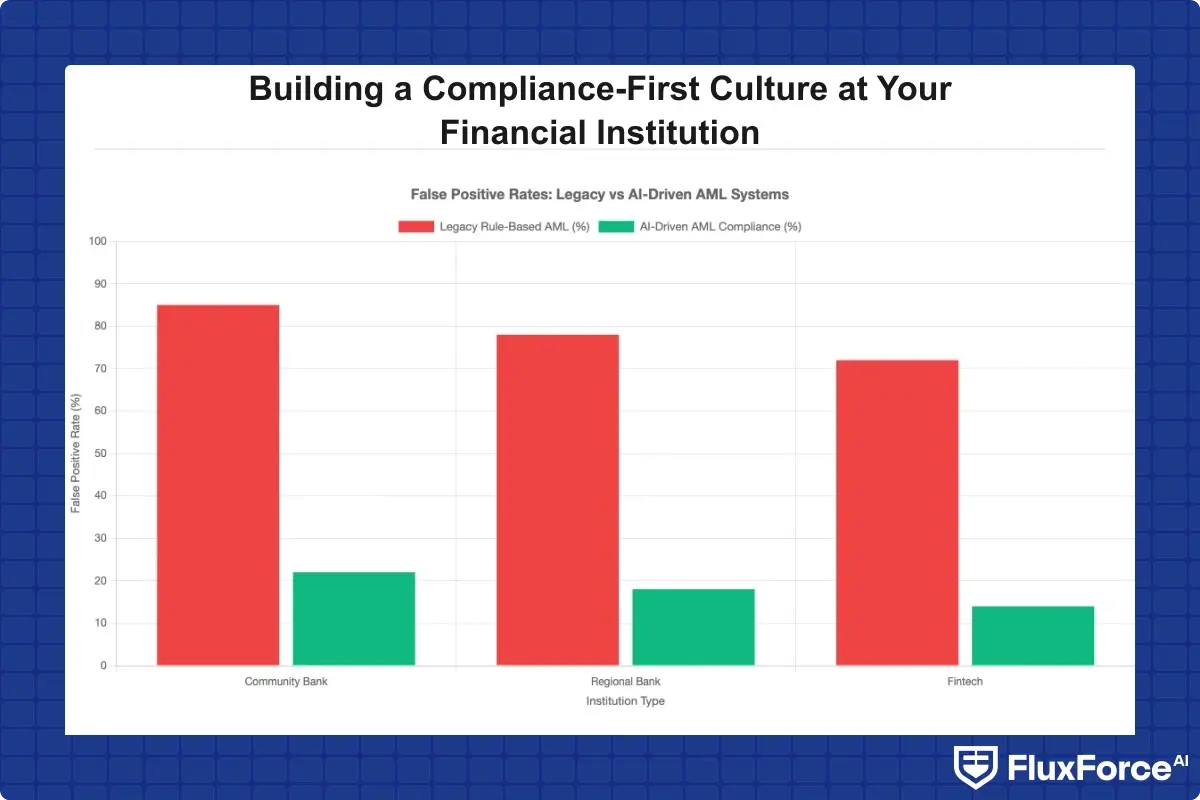

How AML Compliance Software Reduces False Positives

False positives are the hidden cost of compliance programs. A team processing 2,000 alerts per month when only 40 are actionable isn't just inefficient, it trains analysts to rush through cases, increasing the real risk of missing something. The How Agentic AI Fraud Agents Cut False Positives by 80% analysis shows how AI-driven systems reduce alert noise without increasing missed cases.

The How Agentic AI Fraud Agents Cut False Positives by 80% analysis shows how AI-driven systems reduce alert noise without increasing missed cases.

Modern aml compliance software achieves this through adaptive models that learn from your institution's specific transaction patterns rather than applying generic industry thresholds. A payment processor has fundamentally different baseline behavior than a community bank, and calibrating accordingly cuts false positive rates by 60% or more in practice.

A payment processor has fundamentally different baseline behavior than a community bank, and calibrating accordingly cuts false positive rates by 60% or more in practice.

SAR Filing Efficiency: From Manual Process to Automated System

SAR filing efficiency is one of the clearest measures of a mature compliance program. The average SAR takes two to four hours to complete manually, from identifying the activity to writing the narrative to submitting through FinCEN's BSA E-Filing System. For institutions filing 50 or more SARs per month, that's a significant and recurring operational cost.

A suspicious activity report guide starts with understanding what triggers filing. Under FinCEN guidance, a SAR is required when a transaction involves $5,000 or more and the institution knows, suspects, or has reason to suspect the transaction involves funds from illegal activity, is designed to evade BSA requirements, or lacks a lawful purpose.

SAR Filing Requirements 2026: What's New

Sar filing requirements 2026 reflect ongoing implementation of the Anti-Money Laundering Act of 2020. Key developments compliance teams need to track:

- The beneficial ownership information (BOI) database, now operational under the Corporate Transparency Act, is an available reference when evaluating SAR decisions for business accounts

- Enhanced examiner expectations around SAR narrative quality, specificity about the suspicious behavior is expected, not just transaction data

- Growing expectations that institutions using automated monitoring can explain how their systems make flagging decisions, which connects directly to AI governance requirements

For aml compliance fintech companies, SAR filing carries particular complications because many operate across state lines and in BaaS partnerships, raising questions about shared SAR obligations with sponsor banks.

SAR Filing Best Practices for Efficient Reporting

Sar filing best practices that improve both compliance quality and team throughput:

- Create SAR narrative templates for your most common typologies, structuring, layering through transfers, third-party payroll schemes, with placeholders for case-specific details

- Implement a two-reviewer workflow: one analyst drafts, one senior analyst reviews, rather than each person working in isolation

- Track your SAR-to-filing ratio: if you're opening investigations and closing most without filing, your alert thresholds are likely miscalibrated

- File timely, the 30-day deadline (60 days with additional investigation) has no effective grace period in practice

- Retain SAR records for five years from filing, including supporting documentation and written decisions not to file on investigated cases

For institutions also managing AML screening in digital lending, integrating SAR workflows directly with your loan origination system eliminates the manual handoffs that cause filing delays.

KYC Automation and CDD Requirements in 2026

KYC automation has shifted from a competitive differentiator to an operational necessity. Institutions still running manual customer due diligence processes are operating at a pace that doesn't match digital account opening volumes, and the documentation gaps that result show up directly in exam findings.

KYC CDD Requirements for Banks

Kyc cdd requirements banks must meet stem from FinCEN's Customer Due Diligence Final Rule. The four core elements are:

- Customer identification: Verify identity using documentary or non-documentary methods

- Customer due diligence: Understand the nature and purpose of the customer relationship

- Beneficial ownership: For legal entity customers, identify individuals who own 25% or more or exercise significant control

- Ongoing monitoring: Identify and report suspicious activity; maintain current customer information

Kyc automation 2026 tools address all four elements, but the integration point matters most. A KYC platform that doesn't connect to your core banking system for ongoing monitoring creates a two-database problem: your onboarding records are current, but your transaction monitoring rules aren't informed by updated customer risk ratings.

Enhanced Due Diligence Guide for High-Risk Customers

An enhanced due diligence guide for your highest-risk customer segments, politically exposed persons, money services businesses, cash-intensive businesses, should specify:

- What additional documentation is required at onboarding

- What transaction limits apply during the initial relationship period

- How frequently enhanced reviews occur (often annually versus standard three-year cycles for lower-risk customers)

- Who has authority to approve the relationship and under what documented conditions

The AML Risk Checks in Policy Issuance guide covers similar EDD principles for insurance institutions managing high-risk applicants, and the framework translates well to banking contexts.

Building Compliance Culture in Fintechs and Community Banks

The compliance culture financial institution conversation looks different depending on charter type and size. A national bank with 5,000 employees has the resources, and the regulatory scrutiny, that make formal culture programs necessary. A 40-person fintech or a community bank with eight branches operates under different constraints, and has different opportunities.

AML Compliance Fintech: Unique Pressures

Aml compliance fintech companies face a structural tension: growth speed and compliance rigor pull in opposite directions. A startup that takes three months to onboard a new business customer because CDD is manual doesn't survive long enough to worry about exams. But cutting corners on beneficial ownership verification creates direct regulatory exposure that can result in enforcement actions, fines, or charter restrictions.

The resolution isn't choosing between speed and compliance. Fintechs that integrate aml compliance software at the API level, where identity verification, watchlist screening, and transaction monitoring happen as part of the core product flow rather than as manual post-processing, achieve both goals. Manual Compliance vs. AI Automation is worth reading if your team is still debating whether automation replaces the compliance officer role. It doesn't. But it changes what that role looks like in practice.

Fintech BSA AML Small Team Strategies

Fintech bsa aml small team programs that work share one characteristic: they're designed for the size of the operation, not copied from a large bank's compliance manual. A three-person compliance team at a digital payments company should be spending most of their time on judgment calls, not extracting data from systems that don't communicate with each other.

Practical steps for lean teams:

- Prioritize a single integrated platform over a collection of point solutions, data fragmentation is the primary enemy of small compliance teams

- Use vendor-provided typology libraries rather than writing all your own alert rules from scratch

- Build direct relationships with your examination team, smaller institutions typically get more examiner contact time, which can be used proactively to discuss program changes before exams rather than defending them during one

Anti-Money Laundering Technology in 2026: What's Changed

Anti money laundering technology 2026 has three trends compliance officers need to understand, not because they're mandatory today but because regulators are already asking about them in examination conversations.

AML Risk Assessment Guide for 2026

An aml risk assessment guide for 2026 needs to account for risk factors that weren't material three years ago:

- Cryptocurrency exposure: Institutions that don't custody crypto still need to assess exposure through customers who do. Payment rails that touch crypto platforms carry risk profiles different from purely fiat flows.

- AI model governance: If your AML monitoring uses machine learning, regulators expect documentation of how the model works, what data it trained on, and how you validate outputs. This is a compliance question, not just an IT one.

- Third-party vendor risk: AML programs increasingly rely on external providers for identity verification, adverse media, and beneficial ownership data. Your risk assessment should evaluate vendor reliability and data coverage gaps.

EU AI Act Financial Services Implications

The eu ai act financial services requirements are becoming concrete for institutions with European operations or European customers. AI systems used in customer risk scoring or transaction monitoring may qualify as high-risk systems under the Act, which carries specific requirements for human oversight, documentation, and transparency.

For U.S.-only institutions, this still matters: the EU AI Act is actively shaping how global AML software vendors design their products. Understanding the framework helps you evaluate vendor roadmaps more accurately. Sanctions Screening automation is one area where AI governance requirements are especially relevant, since automated screening decisions carry immediate customer-facing consequences.

- A compliance culture financial institution environments need is one where compliance is treated as an operational standard rather than a legal obstacle.

- A practical bsa aml compliance checklist covers more than what you hand regulators during an exam.

- The shift from manual processes to AML compliance software changes what's possible, not just what's faster.

- SAR filing efficiency is one of the clearest measures of a mature compliance program.

- KYC automation has shifted from a competitive differentiator to an operational necessity.

Onboard Customers in Seconds

Conclusion

Building a compliance culture financial institution teams actually adopt requires connecting formal program requirements, the BSA/AML compliance checklist, the SAR filing procedures, the KYC automation systems, to the daily decisions your people make. Technology solves the volume problem. Culture solves the judgment problem.

The institutions that handle regulatory change well aren't the ones with the most sophisticated software. They're the ones where aml compliance is a shared responsibility, where a branch manager escalates a concern because they understand why it matters, and where the compliance officer isn't scrambling during exam prep because the program runs consistently all year.

Start with tone at the top, invest in the right AML infrastructure, and build processes your team can actually follow rather than work around. The gap between a compliance program that exists on paper and one that functions under pressure almost always comes down to the culture you've built around it, and that's something no software purchase solves on its own.

Share this article