.webp)

Listen To Our Podcast🎧

Introduction

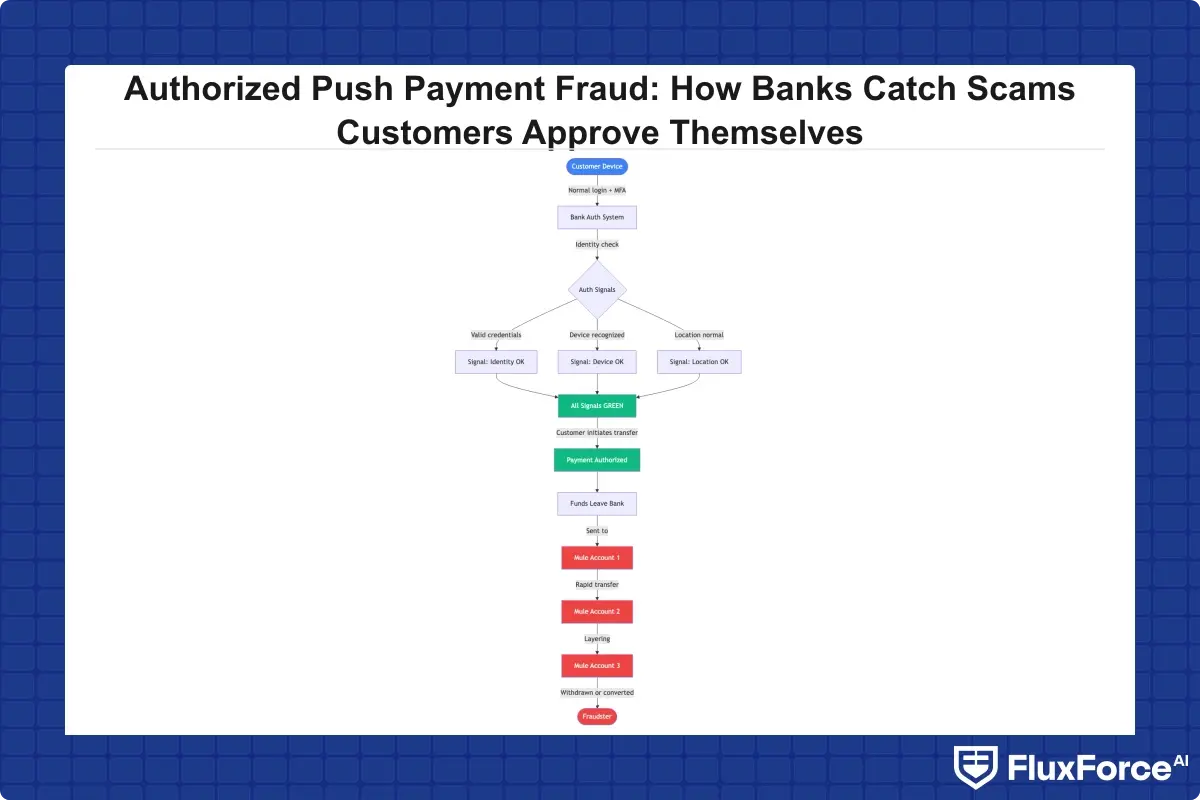

Authorized push payment fraud detection is now the central battleground for bank fraud teams, and the problem is more awkward than most compliance officers want to admit: the customer pushed the button.

Unlike card-not-present fraud, where a transaction occurs without the customer's knowledge, APP fraud works by convincing a legitimate account holder to transfer money to a fraudster's account. The bank's authorization system sees valid credentials, a familiar device, a recognized customer. Every signal says approve. Only the downstream destination is wrong, and by the time anyone notices, the money has moved through several mule accounts.

In 2023, UK Finance reported £460 million in APP fraud losses. The US Federal Trade Commission recorded wire and bank transfer scams as the costliest fraud category by median loss per victim, at $1,500 compared to $100 for credit card fraud. The PSR's October 2024 reimbursement mandate now makes detection accuracy a balance sheet issue, not a technology preference.

The US Federal Trade Commission recorded wire and bank transfer scams as the costliest fraud category by median loss per victim, at $1,500 compared to $100 for credit card fraud.

- Why Authorized Push Payment Fraud Detection Fails With Rule-Based Systems

- How Does AI Detect Fraud in APP Scam Scenarios?

- The False Positive Problem in Authorized Push Payment Fraud Detection

- What Does Real-Time Authorized Push Payment Fraud Detection Actually Require?

- How Transaction Monitoring Software Handles APP Fraud at Scale

Onboard Customers in Seconds

Why Authorized Push Payment Fraud Detection Fails With Rule-Based Systems

Rule-based fraud systems were designed for a different problem. They catch velocity anomalies: too many transactions in an hour, a card-not-present purchase above a threshold, a geographic impossibility. These rules work against automated card fraud because the attacker's behavior is consistent and pattern-matching catches it.

APP fraud does not cooperate with velocity rules. A £22,000 transfer to a new payee is suspicious, but it also describes exactly what legitimate business payments look like. A customer sending their life savings to a financial advisor they met online has a completely normal behavioral fingerprint right up until the moment they execute the transfer.

The Problem With Static Velocity Rules

Static velocity rules produce two failure modes. First, they miss APP fraud because the transaction profile often matches legitimate large payments. Second, they flag legitimate business transactions at a high rate, which drives fraud alert fatigue across operations teams. When analysts review 400 alerts a day and 380 are false positives, the real fraud cases get buried under noise.

The false positive rate in rule-only systems typically runs between 85% and 95% in high-volume environments. That means for every 20 alerts, 17 to 19 require no action. The practical result: burned-out analysts, review queues measured in days, and fraud slipping through because human attention has limits. Fraud alert fatigue is not a morale problem. It is a detection gap with a measurable cost.

How Social Engineering Bypasses Authorization Checks

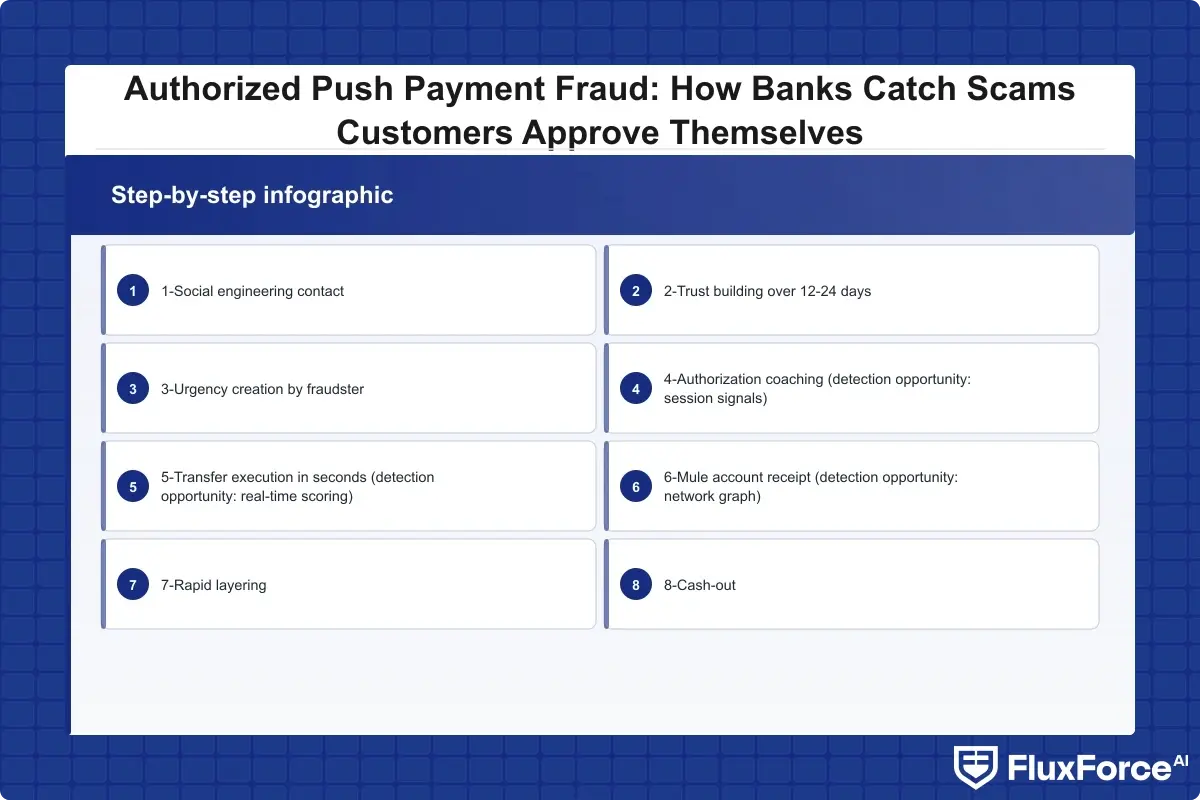

The deeper failure is that rule-based systems cannot detect social engineering context. When a fraudster calls a customer, impersonates their bank's fraud team, and walks them through approving a test transaction to a safe account, the customer's behavior at the transaction screen is indistinguishable from a routine payment. The bank's system has no signal for the conversation happening in parallel. This is where ai fraud detection has to work differently.

How Does AI Detect Fraud in APP Scam Scenarios?

AI fraud detection explained: AI-based systems do not just check whether a transaction exceeds a threshold. They build a behavioral model per customer, per device, per payment corridor, and they measure how far today's behavior deviates from that model. The baseline is not a static rule. It updates continuously as the customer's normal patterns evolve.

Machine Learning Fraud Detection: Behavioral Baselines

Machine learning fraud detection systems build profiles across hundreds of dimensions: typical payee types, usual transaction sizes by payee category, time-of-day patterns, device characteristics, session velocity, and geographic context. When a first-time large payment goes to a new payee at 11pm from a device that spent 40 minutes in a call application before opening the banking app, that cluster of signals produces an anomaly score that no single rule would catch.

The important nuance: machine learning does not compare behavior against population averages. A small business owner regularly sending £50,000 to suppliers has a different baseline than a personal account holder. Training on individual-level patterns is what separates modern fraud detection software from population-level rules, and it is why ai fraud detection in banking has become a board-level investment rather than an IT refresh.

AI Fraud Detection in Banking: The Graph Signal Layer

AI fraud detection in banking increasingly layers network graph analysis on top of behavioral models. If the destination account for today's transfer received funds from six other customers across three different banks in the last 72 hours, and all those senders show behavioral anomalies consistent with social engineering (prolonged session, delayed submission, multiple correction events), the system can flag that destination as a likely mule account before the transfer completes.

This is materially different from what rule-based systems can do. Graph signals require cross-customer data correlation in real time, which is computationally expensive but increasingly practical as cloud-native transaction monitoring software scales horizontally. It is also why ai fraud detection software from newer vendors outperforms legacy rule engines on APP fraud specifically.

How Does AI Detect Fraud With Minimal Customer Friction?

By scoring transactions in the background and triggering intervention only when the anomaly score crosses a calibrated threshold. A transaction scoring 0.3 goes through with no friction. A transaction scoring 0.85 triggers a soft confirmation prompt or a short delay. A transaction scoring 0.97 triggers an analyst hold and an automatic case. This tiered model catches APP fraud without adding friction to the 98% of transactions that are legitimate. Getting those thresholds right is the hard part, and it is where most implementations fall short.

The False Positive Problem in Authorized Push Payment Fraud Detection

Every authorized push payment fraud detection system faces a core tension: the same signals that indicate APP fraud also describe urgent legitimate transactions. A first-time large payment to a new payee is suspicious. It is also how every legitimate new supplier relationship starts. Getting this balance wrong in either direction creates real costs.

How to Reduce False Positives in AML Programs

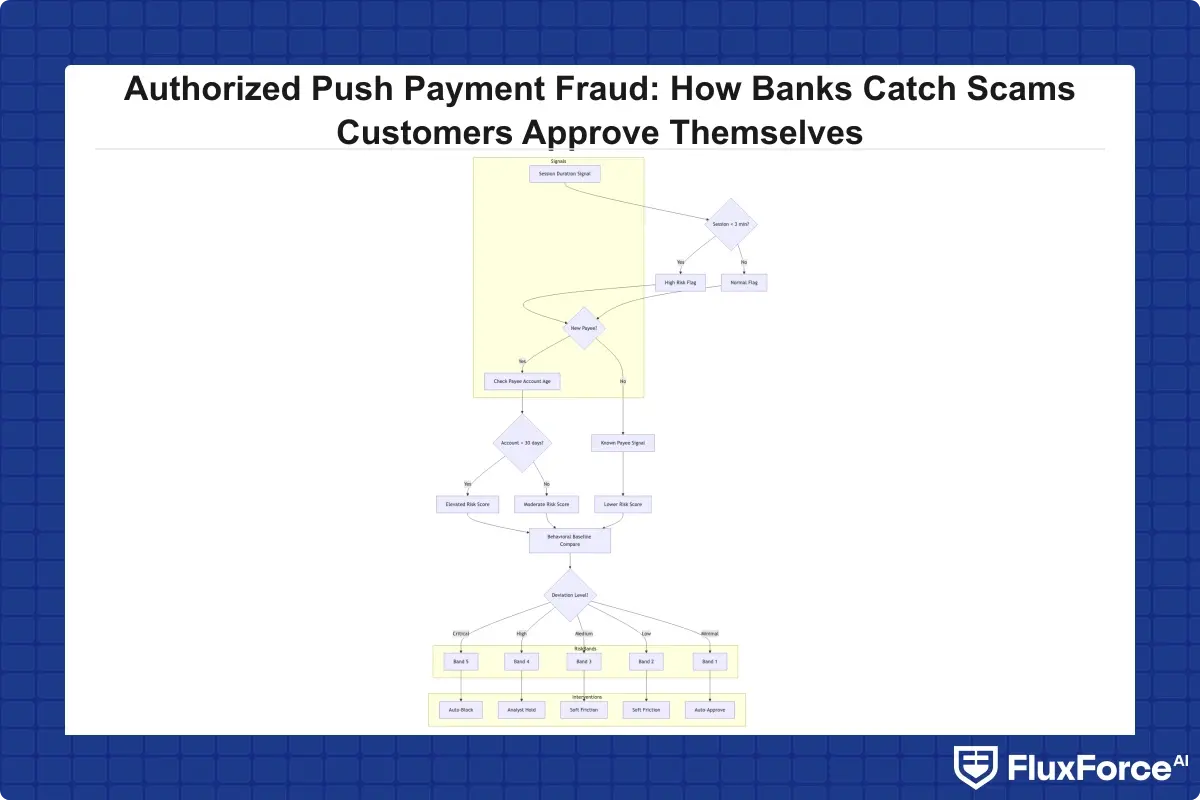

Reducing false positives in AML and fraud contexts requires moving from binary scoring to probabilistic tiering. Instead of block-or-pass, automated transaction monitoring systems assign each transaction to a risk band, and each band triggers a proportionate response:

- Band 1 (score 0-0.4): Auto-approve, no friction

- Band 2 (score 0.4-0.65): Soft friction, confirmation prompt

- Band 3 (score 0.65-0.8): Enhanced confirmation, delay timer

- Band 4 (score 0.8-0.95): Analyst review queue, automatic hold

- Band 5 (score 0.95+): Auto-block, immediate case creation

This structure gives operations teams an actionable workflow rather than an undifferentiated queue of alerts. Agentic AI approaches to false positive reduction show that tiered intervention with automated transaction monitoring can reduce analyst workload by up to 80% compared to rule-only alerting, without a corresponding increase in missed fraud.

Agentic AI approaches to false positive reduction show that tiered intervention with automated transaction monitoring can reduce analyst workload by up to 80% compared to rule-only alerting, without a corresponding increase in missed fraud.

False Positive Cost Fraud Operations Must Price In

False positive cost fraud teams often undercount. The visible cost is analyst time: at 15-20 minutes per alert, a team processing 500 daily alerts spends roughly 125-167 person-hours per day on review. At a fully loaded cost of $80 per hour for experienced fraud analysts, that is $10,000 to $13,360 per day in labor alone.

The invisible costs are larger. Customers blocked during legitimate urgent transfers experience friction that increases churn risk. One UK consumer study found that 34% of consumers who experienced a false fraud block would consider switching banks. Fraud alert fatigue compounds this: when analysts are buried in false positives, real cases get less attention and miss rates climb. Pricing the full false positive cost fraud impact, including churn and missed detection, changes the ROI calculation on better tooling considerably.

False Positive Rate Fraud Detection Benchmarks

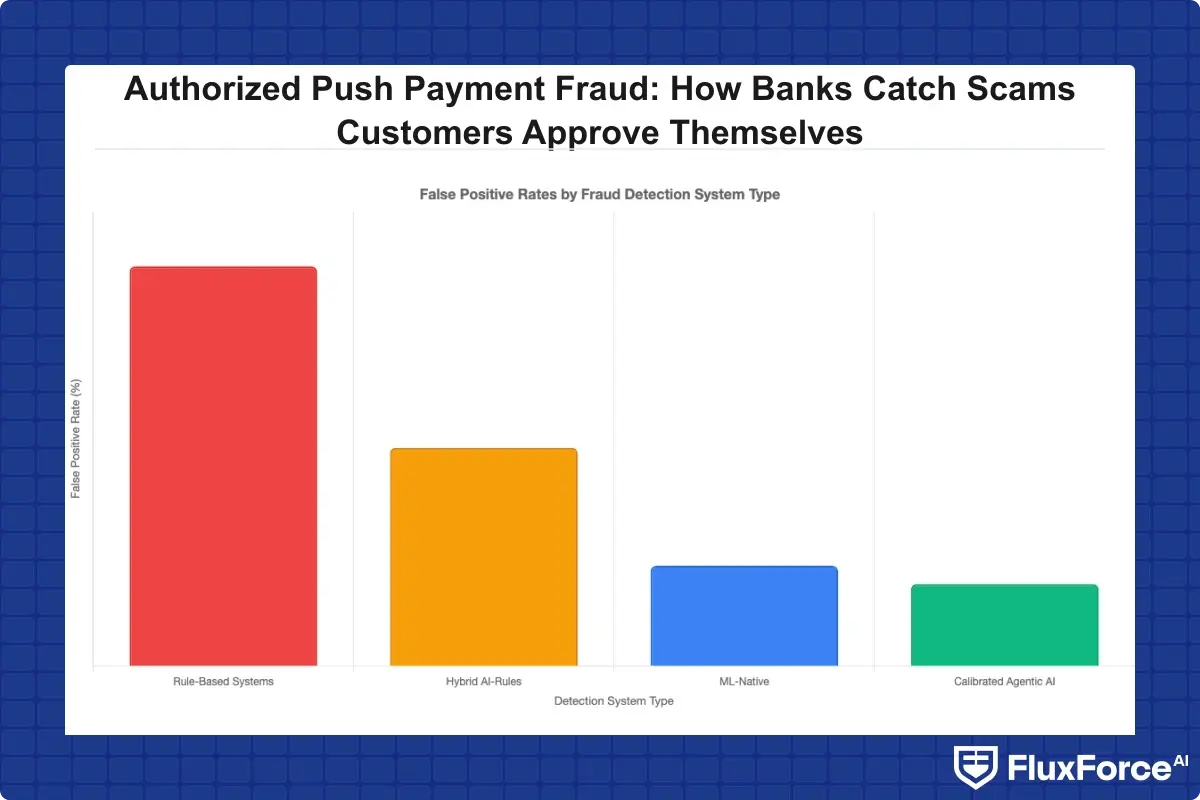

False positive rate fraud detection performance varies widely by system type. Rule-based systems in production environments: 85-95% false positive rate. Hybrid rule-plus-ML systems: 40-55%. Well-calibrated ML-native systems: 15-25%. The operational difference between an 85% false positive rate and a 20% false positive rate at 500 daily alerts is approximately 325 fewer analyst review hours per day. That is the labor equivalent of four full-time fraud analysts. For context on what this looks like across a full detection program, the comparison of AI versus rule-based false positive approaches covers the architectural tradeoffs in detail.

Rule-based systems in production environments: 85-95% false positive rate.

What Does Real-Time Authorized Push Payment Fraud Detection Actually Require?

Real-time fraud detection banks need differs from what legacy systems deliver. Real-time in fraud contexts means sub-second scoring: the decision to approve, add friction, or hold must be made before the customer sees a payment confirmation screen. That requires the scoring model to execute in under 200 milliseconds, including data enrichment.

Real-Time Fraud Detection Banks Need: Sub-Second Architecture

Real-time fraud detection banks require a specific infrastructure stack. The model needs to run inference in memory, not against a cold database query. Feature engineering (computing behavioral deltas, network signals, session characteristics) needs to run in a streaming pipeline, not a batch job. And the decision needs to return to the authorization API before the payment gateway times out.

Most banks that built their transaction monitoring infrastructure in the 2010s run batch-mode processing with 4-hour or 24-hour windows. For APP fraud, batch-mode is useless: the money moves in seconds. Real-time fraud detection, properly implemented, cuts APP fraud losses by 40-65% compared to batch-mode alerting, based on published results from UK banks that adopted PSR-compliant real-time monitoring between 2022 and 2024.

Data Signals That Matter Most for APP Fraud

Not all data signals are equally predictive of authorized push payment fraud. The highest-value signals across multiple production deployments:

- Session duration before submission: Victims spend significantly longer in the app before authorizing fraudulent transfers, often because the fraudster is coaching them in real time.

- New payee combined with large amount and unusual time: This combination has a much higher fraud rate than any single factor alone.

- Payee account age under 30 days: Newly opened accounts receive disproportionately high APP fraud proceeds.

- Keyboard correction events: High correction counts before submitting a payment often indicate someone reading out account numbers from a fraudster.

- Prior extended call-application usage in the session: Transactions initiated shortly after 30-plus minutes in a call app show elevated fraud rates across multiple bank datasets.

How Transaction Monitoring Software Handles APP Fraud at Scale

Transaction monitoring software built for AML compliance was not designed for APP fraud. AML monitoring looks for patterns over weeks or months: structuring, layering, smurfing. APP fraud happens in minutes and the intervention window is seconds. The two problems are related but they require different architectures, and many institutions are trying to solve an APP fraud problem with an AML-era system that processes events in batches rather than streams.

Reduce False Positives Transaction Monitoring With AI Triage

The most effective approach to reduce false positives in transaction monitoring is adding an AI triage layer between the alert generation engine and the analyst queue. Raw alerts come out of the rules engine. The AI triage layer scores each alert against a secondary model trained on case outcome history, learning from every previous alert that turned out to be a false positive and adjusting future scoring accordingly.

Its only job is to tell analysts which alerts to open first. Automated transaction monitoring with this triage capability consistently moves confirmed fraud cases to the top of the queue, which means analysts catch more fraud within the same working hours. For institutions processing above 100,000 transactions daily, AI-assisted triage has moved from a competitive advantage to a baseline operational requirement.

Transaction Monitoring Cost vs. Detection Value

Transaction monitoring cost is often framed as a technology purchase decision, but the real model is more complex. A bank paying $1.2 million per year for a well-calibrated AI monitoring platform that catches 70% of APP fraud spends far less than a bank paying $400,000 for a rules engine and $900,000 in analyst labor to process the resulting alert volume. Factor in reimbursement liability under PSR rules, and the math shifts further toward AI-native platforms.

The honest tradeoff: transaction monitoring software with strong AI capabilities requires more upfront configuration, data science involvement in threshold tuning, and ongoing model monitoring. That is real operational overhead that smaller fintechs may lack the in-house capacity to absorb.

Sardine vs Unit21: Picking the Right Fraud Platform

The sardine vs unit21 comparison comes up frequently in procurement conversations because both platforms target financial institutions with APP fraud problems, but they serve different operational profiles. The decision is less about which platform is better in the abstract and more about which fits the institution's detection priorities and compliance workflow.

Sardine: Strengths for Digital-First Fintechs

Sardine is built around device intelligence and behavior biometrics. Its strongest capabilities are in detecting account takeover and social engineering at the session layer, making it a natural fit for mobile-first fintechs where device signals are rich. The platform delivers real-time fraud detection with sub-200ms latency on standard deployments and has particularly strong APP fraud detection in consumer mobile contexts.

Where Sardine is weaker: large-enterprise compliance workflows. Its case management and SAR filing tooling is less mature than Unit21's, and its reporting structure requires more custom development for institutions with complex compliance hierarchies.

Unit21: Strengths for Compliance-Heavy Banks

Unit21 is designed as a no-code rules and investigation platform. Its strength is giving compliance teams the ability to build and modify detection logic without engineering involvement. For banks where the bottleneck is the compliance team's ability to respond to new fraud typologies quickly, that flexibility is a genuine advantage.

The tradeoff: Unit21's AI capabilities, while improving, rely more heavily on rule configuration than pure ML inference. For APP fraud specifically, where behavioral signals matter more than transaction patterns, the ML layer needs to be doing real work. For institutions evaluating the sardine vs unit21 decision, a complementary architecture (Sardine's device intelligence feeding Unit21's case management) is a deployment pattern several mid-sized banks have adopted effectively.

Regardless of platform, understanding intersecting fraud types is essential. APP fraud frequently involves synthetic identity fraud, where fraudsters build credible account histories over 12-24 months before executing large transfers. Any platform evaluation should include testing against synthetic identity scenarios in the mule account detection layer.

Payment Fraud Prevention: What Regulators Now Expect

The regulatory floor for payment fraud prevention has risen sharply since 2022. In the UK, the PSR's APP fraud reimbursement mandate effective October 2024 requires banks and payment service providers to reimburse APP fraud victims up to £85,000 per claim, with liability shared between the sending and receiving institution. For US institutions, FinCEN's expanding guidance on business email compromise and wire fraud puts similar pressure on risk programs.

PSR Reimbursement Rules and What They Mean for Risk Teams

PSR reimbursement liability changes the authorized push payment fraud detection ROI calculation at a structural level. Previously, a bank might absorb a portion of APP fraud losses as a customer relations cost while declining most reimbursement claims informally. Under the new rules, the liability is mandatory and auditable: miss a fraud that a proportionate detection system should have caught, and the reimbursement is non-discretionary.

Risk teams need to document that their detection systems meet a proportionate and effective standard. That means having model documentation, threshold calibration records, and alert disposition histories available for regulatory review. Institutions that have built program documentation alongside their detection capabilities, as outlined in this overview of AI versus traditional fraud detection frameworks, are better positioned for examiner scrutiny than those that upgraded technology without upgrading their documentation practices.

Synthetic Identity Fraud: The APP Fraud Enabler

Synthetic identity fraud creates the mule accounts that receive APP fraud proceeds. A synthetic identity (a manufactured persona combining real and fabricated elements) can maintain a clean account history for 12-24 months before being activated. By the time an APP fraud victim sends money to that account, it has a transaction history that looks legitimate to any rule-based monitoring system.

Detecting synthetic identity accounts before they are activated as mule accounts requires cross-institutional signals and network-level analysis. Platforms with broad institutional connectivity have a structural advantage here, and it is a key dimension in any authorized push payment fraud detection vendor evaluation. Payment fraud prevention programs that treat mule account detection as a separate workstream from APP fraud detection will always be one step behind the attack chain.

- Rule-based fraud systems were designed for a different problem.

- AI fraud detection explained: AI-based systems do not just check whether a transaction exceeds a threshold.

- Every authorized push payment fraud detection system faces a core tension: the same signals that indicate APP fraud also describe urgent legitimate transactions.

- Real-time fraud detection banks need differs from what legacy systems deliver.

- Transaction monitoring software built for AML compliance was not designed for APP fraud.

Onboard Customers in Seconds

Conclusion

Authorized push payment fraud detection is hard precisely because the customer's authorization is genuine. The fraud happens in the conversation before the customer opens their banking app, and detection systems must work backward from behavioral signals to infer that something is wrong with context, not just the transaction itself.

AI fraud detection, particularly machine learning models that build per-customer behavioral baselines and incorporate real-time network signals, addresses this problem in ways static rule-based systems cannot. The key operational lever is calibrating false positive rates: a detection system generating 90% false positives costs nearly as much as the fraud it prevents. Payment fraud prevention at enterprise scale requires probabilistic tiering, automated transaction monitoring with AI triage, and ongoing model calibration.

For compliance officers and risk heads building or upgrading their programs: the PSR reimbursement rules have made the wait-and-see approach to AI adoption significantly more expensive. The institutions ahead on authorized push payment fraud detection treated detection accuracy as a balance sheet issue from the start. If your team is benchmarking current capabilities, this overview of AI-powered fraud detection strategy for risk heads is a practical starting point for identifying gaps in your current detection stack.

Share this article