.webp)

Listen To Our Podcast🎧

Introduction

APP fraud reimbursement rules have fundamentally changed the risk equation for banks and payment service providers. Starting October 2024, the UK's Payment Systems Regulator (PSR) introduced mandatory reimbursement requirements that split liability 50/50 between sending and receiving firms for authorized push payment (APP) fraud. For compliance officers and payments risk teams, this is not a minor policy update. It is a structural change that transforms previously voluntary commitments into enforceable financial obligations, with a reimbursement cap of £85,000 per claim.

Banks that relied on case-by-case discretion now face predictable, significant losses every time a customer falls victim to an APP scam. The pressure to prevent fraud at the source has never been more acute. This post breaks down what the liability shift means operationally, and what fraud prevention infrastructure actually closes the gap.

- What Are the New APP Fraud Reimbursement Rules?

- Why the Liability Shift Changes the Business Case for Fraud Investment

- How AI Fraud Detection Reduces Reimbursement Liability

- What Are False Positives Costing Your Fraud Team?

- Synthetic Identity Fraud and the Reimbursement Blind Spot

Onboard Customers in Seconds

What Are the New APP Fraud Reimbursement Rules?

The UK's PSR mandatory reimbursement regime came into effect on 7 October 2024. Under this framework, payment service providers (PSPs) on both sides of a transaction, the sending PSP and the receiving PSP, share equal responsibility for reimbursing customers who lose money to APP scams. This 50/50 split is the defining feature of the new regime. Prior to October 2024, the Contingent Reimbursement Model (CRM) code governed APP fraud compensation, but participation was voluntary and reimbursement rates varied significantly between institutions.

How the UK's PSR Mandate Works

The PSR mandate applies to Faster Payments transactions and covers personal accounts as well as most business accounts. The default reimbursement cap is £85,000 per claim, though PSPs can voluntarily apply higher limits. There is a consumer excess of £100 for personal account holders, which PSPs may waive. The regime excludes certain categories: international payments, CHAPS transactions, and cases where the customer is found to have acted fraudulently or with gross negligence.

The 50/50 Liability Split Explained

The 50/50 split means a bank that receives fraudulent funds now has direct skin in the game. If a customer at Bank A is deceived into sending £40,000 to a mule account at Bank B, both banks are on the hook for £20,000 each. This fundamentally changes the incentive structure. Receiving PSPs, which previously had little reason to invest in inbound payment screening, now face concrete reimbursement exposure every time their onboarding controls fail to catch a money mule account.

Why the Liability Shift Changes the Business Case for Fraud Investment

Before the mandate, the cost-benefit analysis of fraud prevention was lopsided. Banks weighed the cost of detection tools against potential reputational damage and voluntary compensation. Now the calculation includes mandatory cash outflows. A bank processing 500 APP fraud claims per month at an average loss of £12,000 faces £6 million in monthly reimbursement exposure, split equally with counterparty PSPs. That is £36 million per year before operational costs.

The Financial Exposure Banks Now Face

According to UK Finance, APP fraud losses in the UK totalled £459.7 million in 2023. Under the new mandatory reimbursement rules, a significant portion of those losses now fall directly on PSP balance sheets rather than remaining with victims. For mid-tier banks and challenger fintechs, this is a material financial risk that directly affects capital planning and tier-one capital buffers.

From Voluntary Codes to Legal Obligation

The shift from the CRM code to mandatory reimbursement changes legal exposure significantly. Under the CRM, banks could argue customer vulnerability mitigations and reduce payouts. Under the PSR framework, the bar is higher. PSPs must demonstrate they applied appropriate friction to transactions showing scam indicators. Failure to do so means the presumption runs against the bank, not the customer.

How AI Fraud Detection Reduces Reimbursement Liability

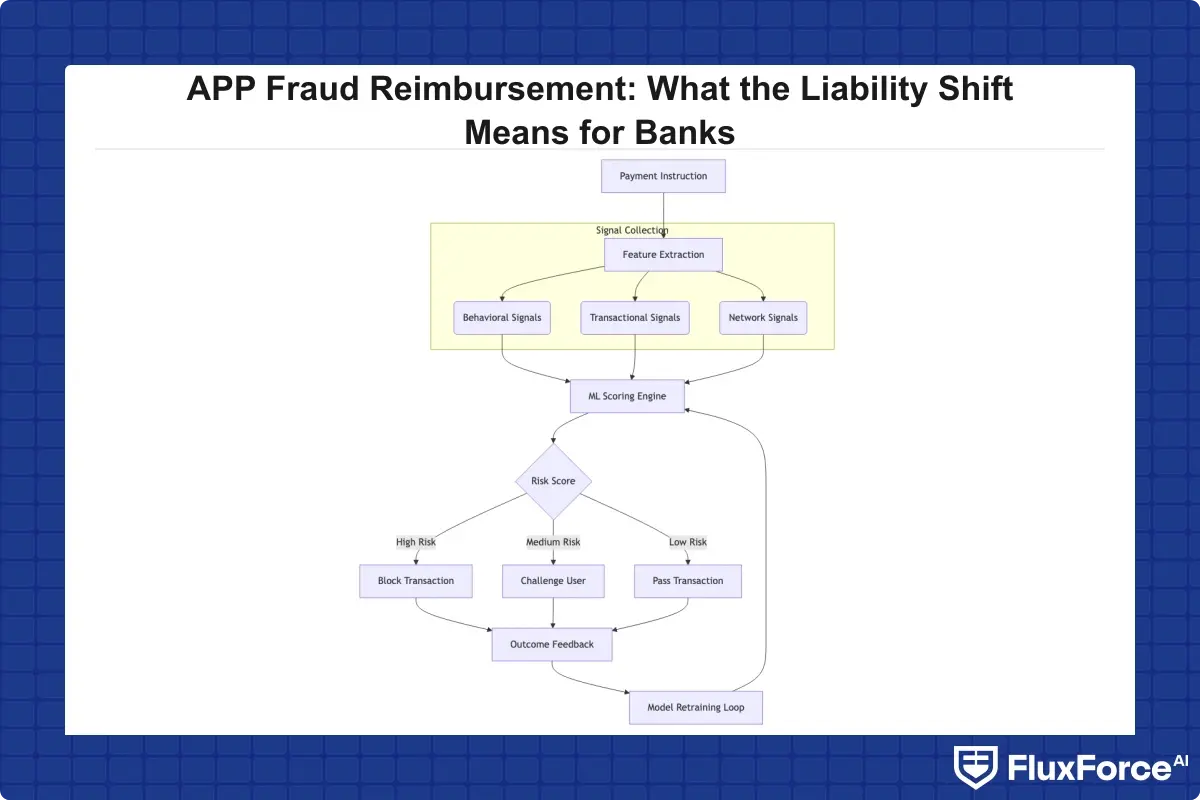

The most direct way to reduce APP fraud reimbursement exposure is to stop the fraud before the payment leaves the customer's account. This is where ai fraud detection in banking has moved from a nice-to-have to a genuine operational necessity. AI systems can evaluate hundreds of behavioral and transactional signals simultaneously, something rule-based systems cannot do at scale.

Real-Time Fraud Detection Banks Are Deploying Now

Real time fraud detection works by scoring every payment instruction against a model trained on historical fraud patterns. When a customer instructs a £15,000 transfer to a new payee they have never transacted with before, combined with a session that began on an unrecognized device at an unusual hour, the model assigns a high-risk score within milliseconds and triggers step-up authentication or a brief payment delay.

Real time fraud detection banks are investing in operates on sub-100ms latency, because payment rails like Faster Payments complete in seconds. The architecture typically uses in-memory feature stores to avoid database round trips during scoring. For a detailed breakdown of how these systems work across card and payment channels, see our analysis of AI-powered fraud detection strategy for risk heads.

How Does AI Detect Fraud in Payment Networks?

AI fraud detection explained simply: the model ingests features derived from the payment instruction (amount, beneficiary, payment type), the customer's behavioral baseline (typical transaction amounts, usual hours, device fingerprints), and network-level signals, such as whether the receiving account is linked to other known fraud cases. Machine learning fraud detection models, including gradient boosting and neural networks, calculate the probability that a transaction is fraudulent before it completes.

The honest answer is that no model is perfect. Fraud rings adapt quickly, and novel attack vectors like impersonation scams involving fake bank calls can fool behavioral models that do not account for real-time telephony signals. The most effective deployments combine ai fraud detection software with step-up challenges tuned to risk score thresholds, rather than simple block/allow decisions.

What Are False Positives Costing Your Fraud Team?

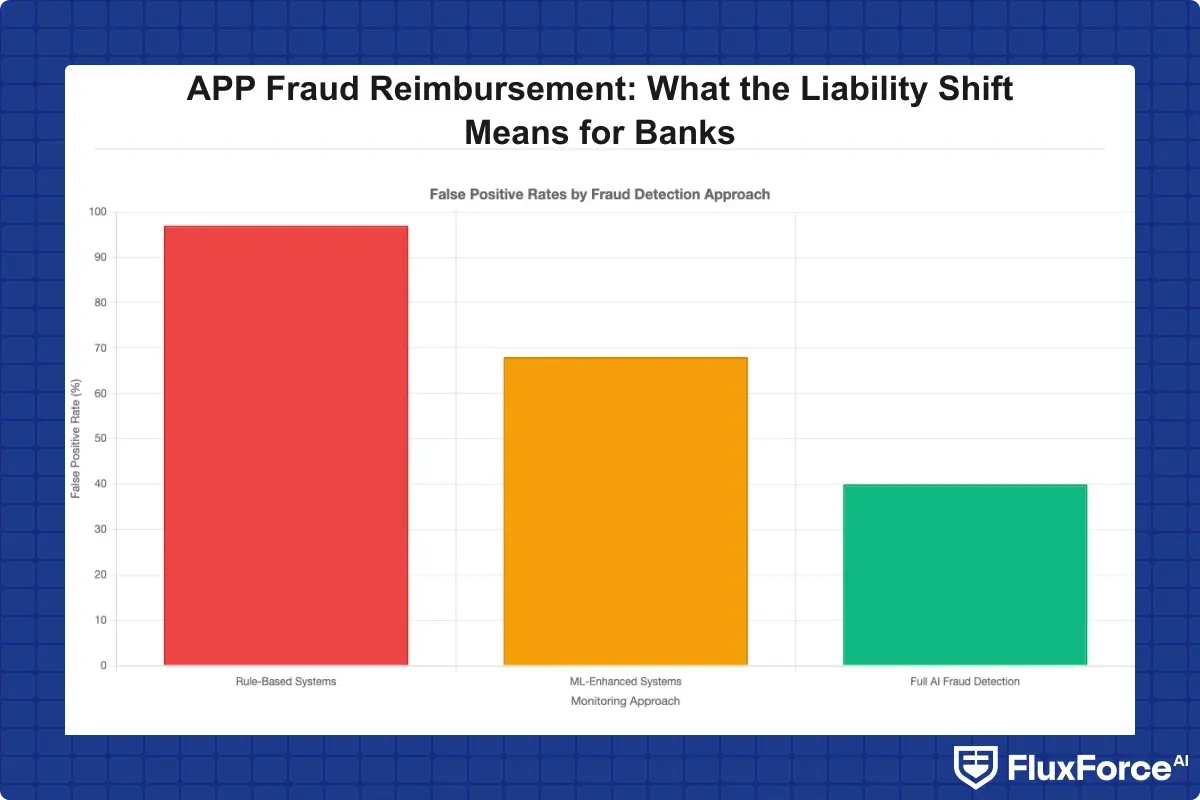

False positives are the silent cost of fraud prevention. Every legitimate transaction blocked or challenged unnecessarily costs the bank a customer interaction, potential abandonment, and the operational overhead of a manual review. As banks tighten controls in response to app fraud reimbursement rules, the false positive rate tends to climb unless AI tuning keeps pace.

False Positive Cost in Transaction Monitoring

The false positive cost fraud teams absorb is substantial. Industry estimates suggest that for every genuine fraud case caught by a rule-based system, 200 to 1,000 false alerts are generated. Each alert requires analyst time, typically 15 to 30 minutes for triage. At a fully loaded analyst cost of £40 per hour, 500 false alerts per day costs roughly £100,000 per month in pure labor, before accounting for customer friction and attrition.

This is why false positive rate fraud detection is now a board-level metric at most tier-one banks. Without AI tuning, the false positive rate typically runs 95-99% of all alerts being non-fraudulent. That number needs to drop below 70% for teams to operate sustainably under the new reimbursement regime.

Without AI tuning, the false positive rate typically runs 95-99% of all alerts being non-fraudulent.

How to Reduce False Positives in AML and Transaction Monitoring

Reduce false positives in transaction monitoring by moving away from static rule thresholds toward dynamic, peer-group benchmarking. A customer sending £5,000 to a new payee carries very different risk depending on whether that customer is a sole trader who regularly pays new suppliers, or a 72-year-old retiree with no history of large outbound transfers.

AI systems achieve this by clustering customers into behavioral cohorts and applying cohort-specific thresholds. Our post on how agentic AI fraud agents cut false positives by 80% covers this architecture in detail. The reduction in alert volume directly reduces transaction monitoring cost and frees analyst capacity for genuine risk cases. For banks still on legacy monitoring, see our breakdown of rule-based systems vs. AI-driven solutions for reducing false positives.

Synthetic Identity Fraud and the Reimbursement Blind Spot

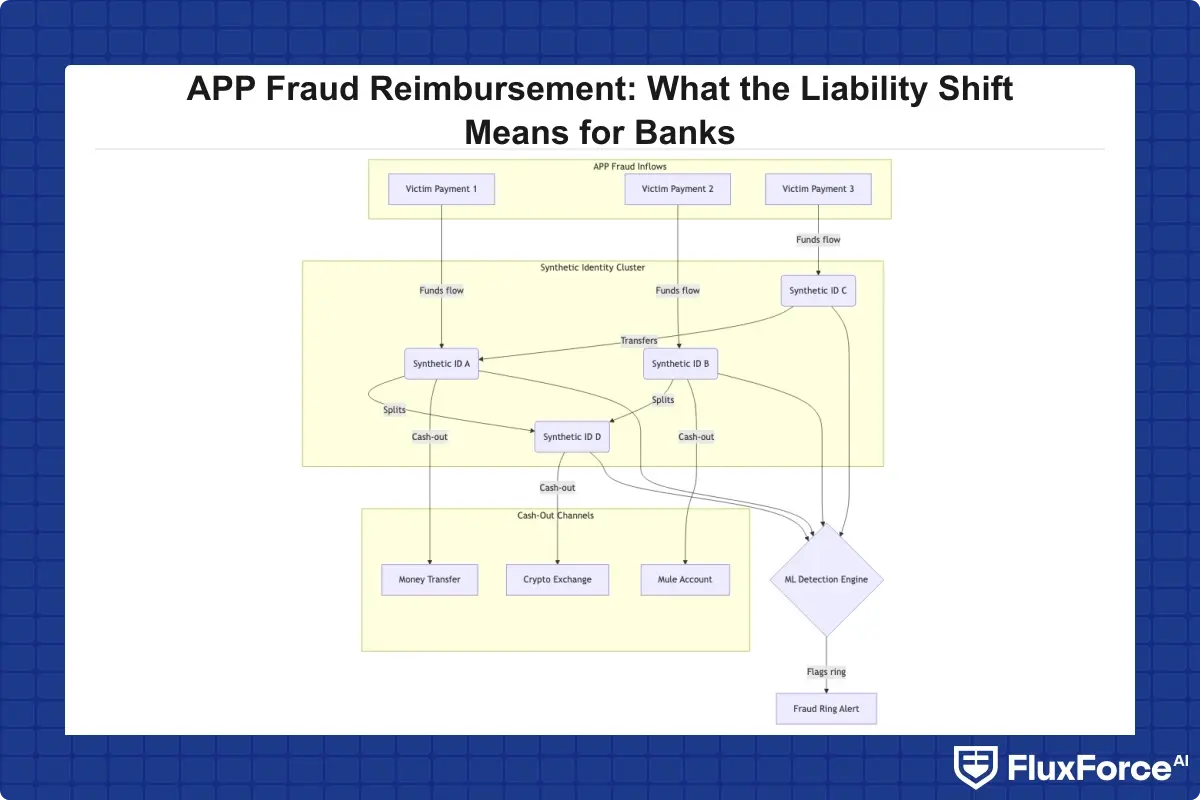

Synthetic identity fraud is a growing vector that intersects directly with APP fraud reimbursement liability. A synthetic identity, created by combining real and fabricated personal data, can pass standard KYC checks and establish a mule account that looks legitimate for months before it receives APP fraud proceeds.

Why Synthetic Identities Evade Traditional Checks

Traditional KYC processes verify that a name, date of birth, and address exist in reference databases. A synthetic identity constructed from a real address, a real date of birth from a different person, and a fabricated name can clear these checks. The account then builds a transaction history over three to six months before being activated for fraud, a pattern known as bust-out fraud. Under the app fraud reimbursement rules, the receiving bank holding this account faces a 50% reimbursement obligation every time the account receives APP fraud proceeds.

Under the app fraud reimbursement rules, the receiving bank holding this account faces a 50% reimbursement obligation every time the account receives APP fraud proceeds.

Machine Learning Fraud Detection for Synthetic Identity Patterns

Machine learning fraud detection is better suited to catching synthetic identities than rule-based systems because the signals are subtle and multi-dimensional. A synthetic account might show perfectly normal individual transactions but an unusual pattern of accepting peer-to-peer payments followed by rapid outbound transfers within hours. Graph-based machine learning models map second-degree connections across accounts to identify mule network clusters before they are activated.

Our post on detecting synthetic identity fraud in real-time covers the specific model architectures banks are using for this problem. The connection to payment fraud prevention is direct: stopping mule accounts at onboarding is cheaper than reimbursing the fraud claims they later enable.

Sardine vs Unit21: Choosing Transaction Monitoring Software Under the New Rules

Banks comparing sardine vs unit21 for transaction monitoring software are weighing two platforms with different architectural philosophies. The choice matters more now that app fraud reimbursement rules create direct financial liability tied to monitoring quality.

How Sardine and Unit21 Approach APP Fraud Detection

Sardine focuses heavily on device and behavioral biometrics as primary fraud signals, with particular strength in real-time session analysis during payment initiation. This makes it well-suited to catching behavioral anomalies that precede APP fraud, such as a customer operating under social engineering pressure, which shows up as faster typing, unusual navigation patterns, or a session open simultaneously with an incoming call.

Unit21 takes a more configurable rules-and-AI hybrid approach, with strong case management workflows that suit AML-heavy compliance teams. Its automated transaction monitoring pipeline integrates with major core banking platforms, and its alert configuration options give teams more direct control over threshold tuning. For teams that need extensive customization of alert rules alongside machine learning scoring, Unit21 provides more flexibility in workflow design.

The honest tradeoff: Sardine's behavioral biometrics layer is more sophisticated for real-time payment fraud prevention. Unit21 is stronger for post-transaction AML compliance workflows and SAR filing. Many banks run both, using Sardine for fraud decisioning and Unit21 for AML case management.

What to Look for in Automated Transaction Monitoring Under the New Rules

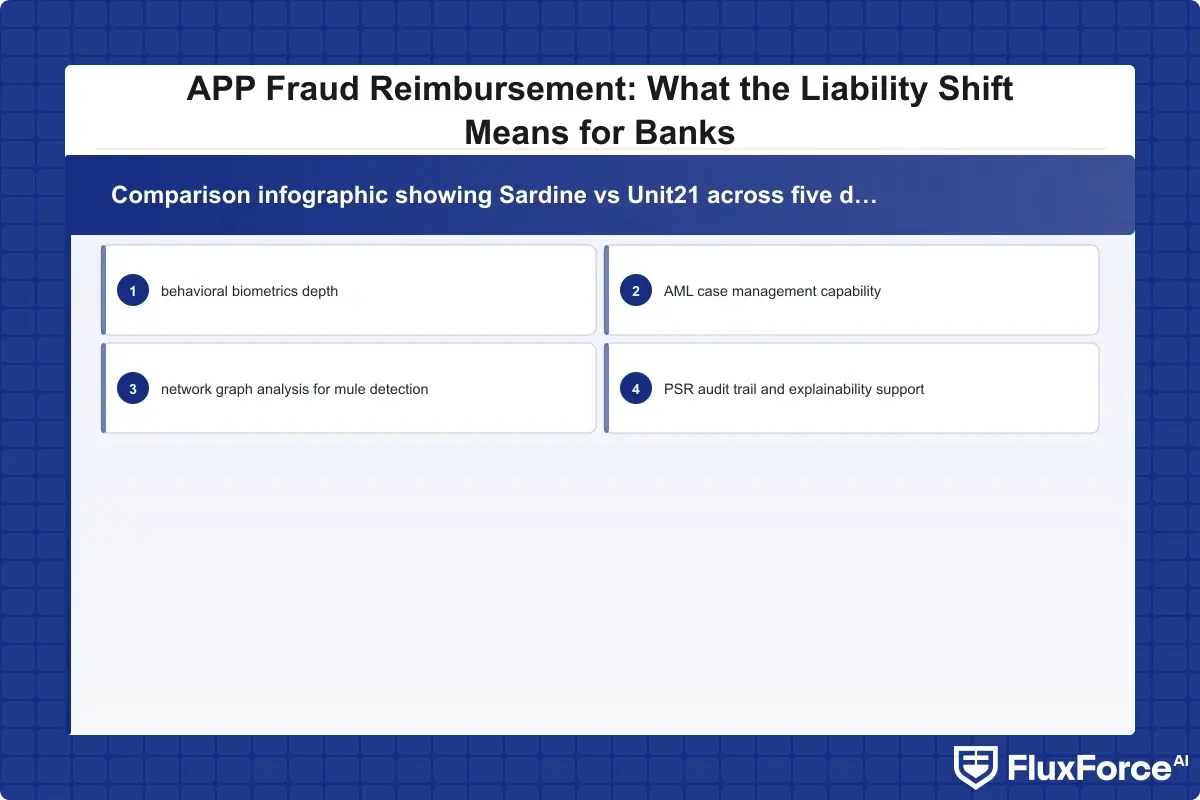

Automated transaction monitoring systems must now meet APP fraud-specific criteria, not just AML checkbox compliance. Key requirements include sub-200ms scoring latency for Faster Payments, behavioral biometrics integration, network graph analysis for mule detection, and explainability outputs for PSR audit trails.

On explainability: when a bank declines reimbursement because a customer acted with gross negligence, the PSR expects documented evidence of the warning given at the time of payment. Automated systems must log the specific signals that triggered friction, not just the outcome. Vendors that cannot produce this audit trail create regulatory exposure regardless of how good their detection rates are.

Building a Payment Fraud Prevention Strategy That Meets the New Rules

Meeting the requirements of the PSR's mandatory reimbursement regime requires more than deploying a single tool. The Payment Systems Regulator makes clear that PSPs must demonstrate proportionate measures across the full payment journey: onboarding controls, transaction monitoring, customer communication, and post-payment review.

Fraud Alert Fatigue Undermines APP Fraud Compliance

Fraud alert fatigue is the compliance risk hiding in plain sight. When analysts process hundreds of low-quality alerts per day, genuine fraud cases get missed. Research indicates that alert fatigue in financial crime teams causes miss rates to climb by 20-30% after the third consecutive hour of queue review. This is not a people problem; it is a systems design problem.

The fix is reducing alert volume through smarter automated transaction monitoring, so that each alert reaching a human analyst is worth reviewing. AI scoring that filters out obvious false positives before they hit the queue cuts volume by 50-80% in most deployments, making fraud teams materially more effective without adding headcount. Fewer alerts, higher quality, fewer missed cases, lower reimbursement exposure.

AI scoring that filters out obvious false positives before they hit the queue cuts volume by 50-80% in most deployments, making fraud teams materially more effective without adding headcount.

Transaction Monitoring Cost vs. Reimbursement Risk

The transaction monitoring cost of a modern AI-enhanced platform, typically £200,000 to £800,000 per year for a mid-tier bank, looks very different when set against reimbursement exposure. A bank with 200 APP fraud cases per month at an average claim of £8,000 faces £1.6 million in monthly reimbursements under the new rules. A 30% reduction in fraud through better detection saves £5.76 million annually, making the monitoring investment pay back in under two months.

For banks evaluating where to start, the fraud detection software available through FluxForce's AI-based fraud detection platform provides a practical reference point for understanding what a compliance-ready stack looks like in production. Fraud prevention also extends beyond technology: banks need clear customer communication strategies, confirmation of payee services, and friction calibrated to actual risk scores rather than static thresholds.

The Financial Conduct Authority's fraud prevention standards define the compliance framework that AI-powered monitoring systems must align with, making vendor selection a compliance exercise as much as a technology decision. For a broader view of how compliance infrastructure connects to modern payment security architecture, our post on zero trust and agentic AI in banking covers the design principles that underpin resilient fraud controls.

- The UK's PSR mandatory reimbursement regime came into effect on 7 October 2024.

- Before the mandate, the cost-benefit analysis of fraud prevention was lopsided.

- The most direct way to reduce APP fraud reimbursement exposure is to stop the fraud before the payment leaves the customer's account.

- False positives are the silent cost of fraud prevention.

- Synthetic identity fraud is a growing vector that intersects directly with APP fraud reimbursement liability.

Onboard Customers in Seconds

Conclusion

APP fraud reimbursement rules have shifted financial liability in a way that makes fraud prevention an urgent balance sheet issue, not just a compliance checkbox. Banks and payment providers that relied on discretionary reimbursement decisions and legacy rule-based monitoring now face mandatory cash outflows tied directly to the quality of their fraud controls. The 50/50 liability split pushes receiving banks to scrutinize onboarding as carefully as sending banks scrutinize payment instructions.

The practical response combines real time fraud detection with AI scoring that reduces false positives, network graph analysis for synthetic identity and mule account detection, and automated transaction monitoring platforms that generate audit-ready evidence for PSR review. Selecting the right transaction monitoring software, whether sardine vs unit21 or another platform, now carries direct financial consequences. The banks that move fastest on ai fraud detection will carry a materially lower reimbursement burden over the next three to five years. If your current fraud stack was not built with mandatory reimbursement in mind, now is the right time to reassess it.

Share this article