.webp)

Listen To Our Podcast🎧

Introduction

314(b) information sharing banks use to detect financial crime is one of the most powerful yet consistently underused tools in the AML compliance toolkit. When one institution sees suspicious fund movement and another holds the next leg of that transaction, neither has the complete picture. Section 314(b) of the USA PATRIOT Act closes that gap by creating a voluntary, legally protected framework allowing financial institutions to share intelligence directly with each other, without fear of civil liability. This article explains how the program works, who qualifies, and how modern aml compliance software and anti-money laundering technology are making 314(b) participation more practical heading into 2026 than it has ever been before.

- What Is 314(b) Information Sharing and How Banks Use It

- How 314(b) Information Sharing Helps Banks Detect Complex Financial Crime

- The 314(b) Registration and Operational Process

- AML Compliance Software and Anti-Money Laundering Technology Supporting 314(b)

- SAR Filing Efficiency Through 314(b) Intelligence

Onboard Customers in Seconds

What Is 314(b) Information Sharing and How Banks Use It

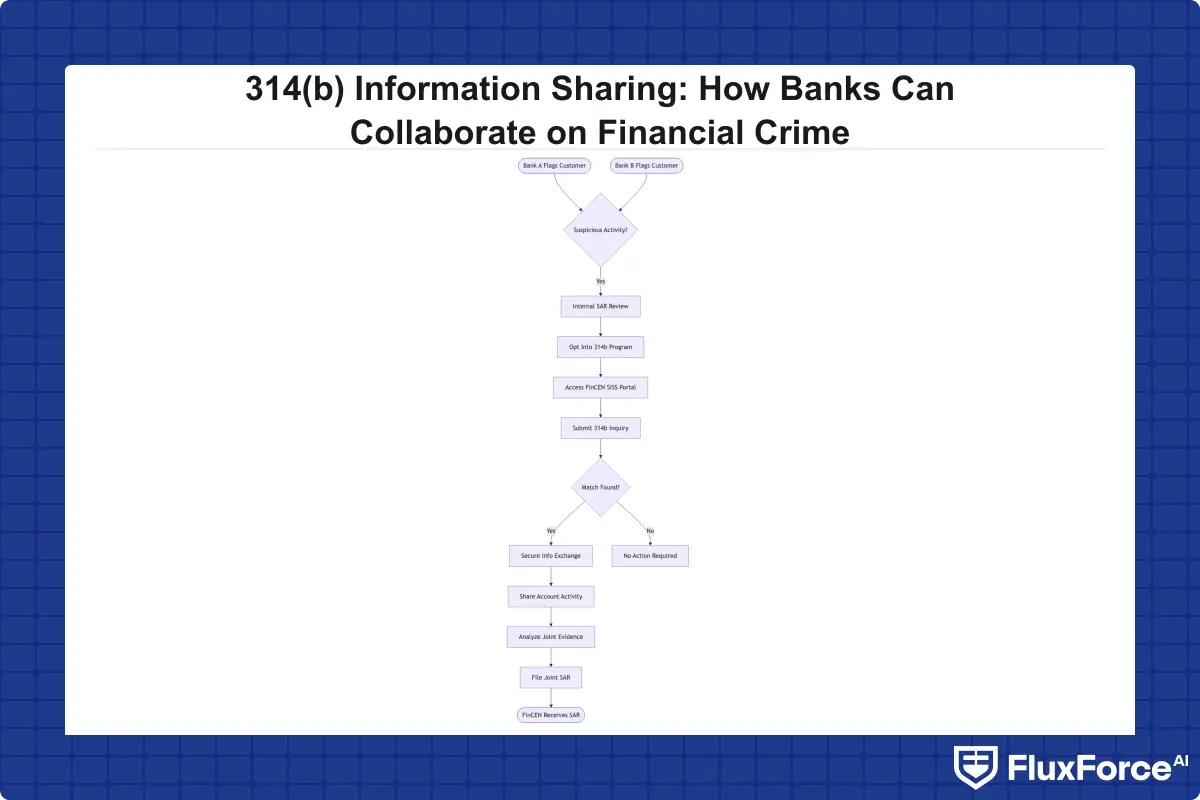

Section 314(b) of the USA PATRIOT Act allows FinCEN-registered financial institutions to voluntarily share information about individuals, entities, and organizations suspected of money laundering or terrorist financing. Unlike the mandatory 314(a) program, where FinCEN pushes a list of names to institutions for screening, 314(b) is peer-to-peer: bank A contacts bank B to ask whether a specific customer holds an account there and what activity that account has shown.

The practical impact is significant. A drug trafficking organization that structures deposits across three regional banks looks like low-risk activity at each individual institution. With 314(b) in place, all three institutions can legally confirm the connection, aggregate the picture, and file a coordinated suspicious activity report.

According to FinCEN's 314(b) program guidance, the program was designed specifically to address the limitation that no single institution sees the full scope of sophisticated money laundering operations.

Who Can Participate in 314(b)?

Eligibility extends well beyond banks. The following entity types can register:

- Federally insured depository institutions (banks, credit unions, thrifts)

- Broker-dealers registered with the SEC

- Mutual funds

- Money services businesses (MSBs) licensed in the US

- Insurance companies subject to Bank Secrecy Act requirements

- Loan or finance companies

- Registered housing government-sponsored enterprises

Fintech companies operating as licensed MSBs or as bank holding company subsidiaries are eligible. Registration is free and typically takes under 15 minutes on the FinCEN portal.

How Does 314(b) Differ from 314(a)?

The core difference is directionality and control. Under 314(a), FinCEN distributes a subject list to institutions, which must screen their records and respond within a fixed window. Under 314(b), institutions initiate contact with each other on their own timeline, about subjects they have already flagged internally. This means 314(b) sharing happens after your compliance team has completed an initial aml risk assessment and concluded the activity warrants peer consultation.

How 314(b) Information Sharing Helps Banks Detect Complex Financial Crime

The financial crimes that matter most, including trade-based money laundering, human trafficking networks, and state-sponsored sanctions evasion, almost always leave partial traces across multiple institutions. That is intentional. Layering transactions across accounts and entities is the core technique of professional money launderers, specifically designed to fall below any single institution's detection threshold.

314(b) information sharing banks rely on works because the legal safe harbor removes the biggest friction point: fear of liability for sharing customer data with a peer institution. A participating institution that shares information in good faith is protected from civil liability under both federal and state law. That protection changes the calculus for compliance officers who previously hesitated to reach out even when they suspected a strong connection.

Identifying Layered Transactions Across Institutions

Consider a concrete example. A payment processor sees a business account receiving high-volume ACH credits from dozens of shell companies. The pattern suggests structuring, but each individual credit falls below ctr filing rules thresholds, so no Currency Transaction Reports are triggered automatically. The processor contacts a regional bank that also appears in the transaction data through a 314(b) inquiry. The bank confirms the same entities are making near-identical deposits at their institution. Together, both institutions now have sufficient grounds for a coordinated sar filing, and the shared intelligence makes the SAR substantially more valuable to law enforcement than either filing could achieve independently.

CTR filing rules require reporting cash transactions above $10,000, but structuring specifically exploits the gap just below that threshold. 314(b) is the mechanism that exposes structuring patterns that no single institution's ctr filing rules compliance process would catch on its own.

CTR filing rules require reporting cash transactions above $10,000, but structuring specifically exploits the gap just below that threshold.

KYC Automation and Enhanced Due Diligence in Shared Intelligence

kyc automation 2026 platforms are beginning to integrate 314(b) workflows directly into due diligence pipelines. When a KYC alert fires and a customer is flagged for review, some platforms now prompt analysts to check whether any 314(b)-registered partner institutions have seen the same entity. This cuts investigation time substantially. A review that once required three days of manual phone outreach can close in hours when kyc cdd requirements banks need to satisfy are supported by a connected intelligence layer. Enhanced due diligence cases, particularly those involving politically exposed persons or high-risk jurisdictions, benefit most from peer corroboration before the EDD report is finalized.

The AML screening strategy for payments risk officers follows the same logic: shared context from peer institutions always produces better risk decisions than isolated, single-institution screening alone.

The 314(b) Registration and Operational Process

Registration is handled through FinCEN's Secure Information Sharing System (SISS). The process itself is quick. The operational infrastructure required to make it work is where institutions either build a real program or let registration sit idle.

Step-by-Step Registration with FinCEN

- Log into the FinCEN 314(b) SISS portal

- Complete the institution profile: legal name, routing number, primary AML contact details

- Designate a secondary contact for coverage during absences

- Submit, FinCEN processes most registrations within one business day

- Renew annually (registration lapses automatically at calendar year-end if not renewed)

The renewal requirement catches many compliance teams off guard. A lapsed registration means your institution cannot legally send or receive 314(b) information. Add the annual renewal to your bsa aml compliance checklist so it does not get skipped during the Q4 compliance calendar crunch.

What Can Be Shared, and What Cannot?

Under 314(b), institutions can share account ownership information, transaction history and behavioral patterns, beneficial owner details, and prior investigation summaries. Institutions cannot share the contents of a filed SAR or confirm that a SAR has been filed on the subject of an inquiry. This is a hard legal line. Disclosing a SAR's existence to any third party, including another 314(b)-registered institution, violates the SAR confidentiality requirement under 31 U.S.C. § 5318(g)(2) and exposes the institution to serious regulatory action.

AML Compliance Software and Anti-Money Laundering Technology Supporting 314(b)

The honest reality is that legacy anti money laundering technology made 314(b) harder to use, not easier. Most traditional transaction monitoring platforms were designed for internal detection workflows, not inter-institutional communication. Analysts wanting to initiate a 314(b) inquiry had to work manually: locate the partner institution's AML contact, send a structured request by secure email or phone, wait for a response, and then reconcile the answer against an open investigation by hand. That friction meant many valid 314(b) inquiries simply never happened.

anti money laundering technology 2026 is addressing this directly. A new generation of aml compliance software, including purpose-built collaborative intelligence platforms, is adding structured 314(b) workflows that handle secure messaging, inquiry tracking, and response documentation entirely within the compliance toolset. For aml compliance fintech operators managing BSA programs with lean teams, this capability is the difference between a 314(b) program that functions in practice and one that exists only on paper.

How Technology Platforms Enable Structured Sharing

The platforms that do this well typically cover four areas:

- Verified partner directories maintained against FinCEN's current registration database, so analysts know immediately which institutions are eligible to receive an inquiry

- End-to-end encrypted messaging with full audit trails that satisfy BSA documentation requirements and data privacy obligations

- Case linkage that automatically enriches an open investigation file when a 314(b) response comes in

- Response documentation templates that confirm safe harbor compliance and can be produced on demand during examination

The EU AI Act and AML Compliance Tools in 2026

For institutions operating across jurisdictions, eu ai act financial services requirements are adding a new layer of consideration to aml compliance software procurement decisions. AI-powered monitoring tools used in customer risk scoring and AML screening now face classification as high-risk AI systems under the EU AI Act, which imposes explainability, human oversight, and audit trail requirements. Compliance teams evaluating new platforms in 2026 should verify that any vendor under consideration has a published EU AI Act compliance roadmap before committing to a multiyear contract.

SAR Filing Efficiency Through 314(b) Intelligence

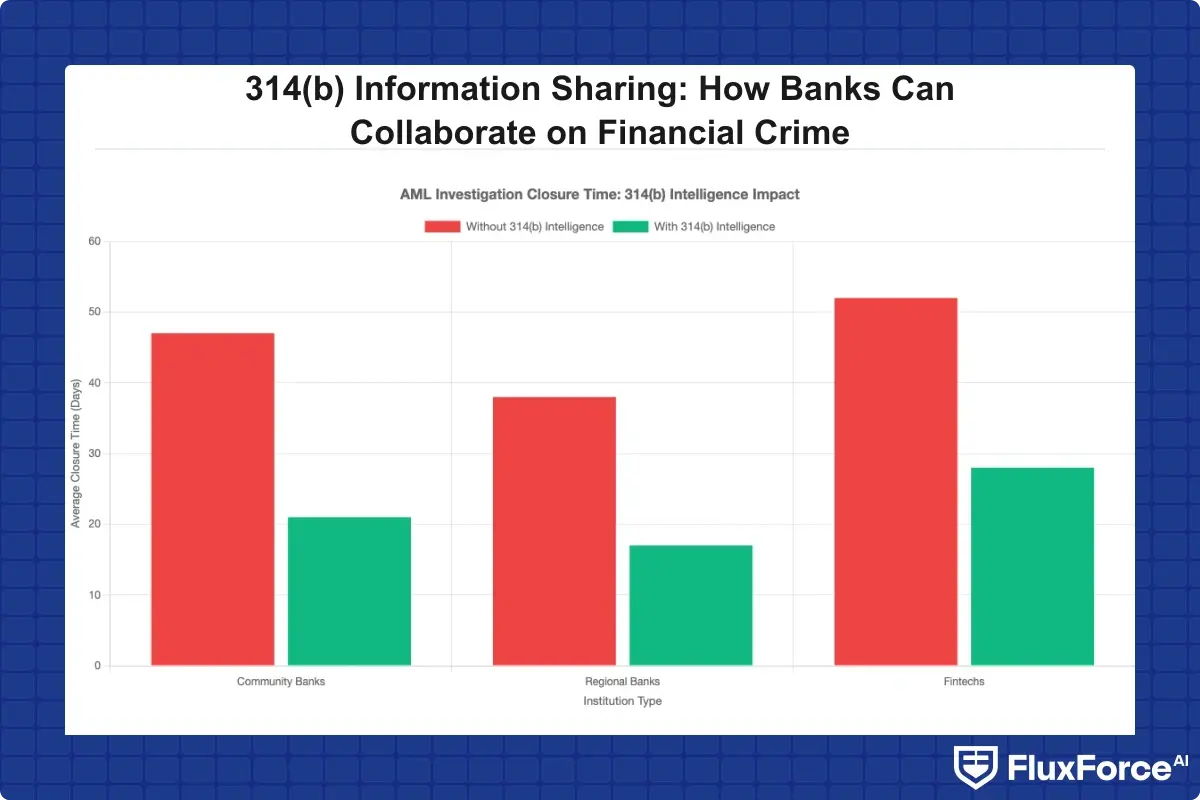

sar filing is where 314(b) delivers its most measurable compliance value. A SAR filed with intelligence from a single institution is useful. A SAR corroborated by information from two or three institutions, each showing the same subject conducting consistent suspicious activity across accounts, is significantly more actionable for law enforcement and reflects better on your institution's program quality.

How Shared Data Improves Suspicious Activity Reports

The suspicious activity report guide published by FinCEN notes that SARs should capture all relevant information known to the filer at the time of submission. When a 314(b) inquiry response reveals that a partner institution has observed matching behavioral patterns, that intelligence belongs in the SAR narrative. It makes the filing more specific, reduces the chance that investigators treat it as low priority, and demonstrates that the institution's program goes beyond automated rule-based screening.

sar filing best practices in 2026 increasingly include a formal 314(b) inquiry step before the SAR narrative is drafted, particularly for cases involving suspected structuring, trade-based laundering, or business account fraud. Some institutions have formalized this as a mandatory workflow gate: no SAR narrative is drafted until a 314(b) inquiry is completed or explicitly documented as not applicable to the specific case under review.

SAR Filing Requirements 2026: What FinCEN Is Prioritizing

sar filing requirements 2026 have remained stable at the federal level, but FinCEN's enforcement emphasis has shifted notably. The agency has flagged increased scrutiny on virtual asset service providers and their interaction with traditional bank accounts, beneficial ownership disclosures under the Corporate Transparency Act, and human trafficking typologies with specific SAR indicator patterns.

For institutions using regulatory compliance automation to manage SAR workflows, verifying that SAR templates reflect current FinCEN priority typologies is a routine step that meaningfully improves sar filing efficiency. Templates that prompt analysts for the right data fields from the start eliminate the revision cycles that add days to SAR completion times.

BSA/AML Compliance Checklist for Community Banks and Fintechs

Building a functional BSA/AML program with active 314(b) participation requires more than a FinCEN registration confirmation. The framework below reflects what a thorough aml risk assessment guide would identify as the operational core requirements for sustained compliance.

BSA/AML Compliance for Community Banks

bsa aml compliance community banks face a distinctive challenge: small compliance teams managing disproportionate regulatory obligations relative to resources available at larger institutions. According to the FFIEC BSA/AML Examination Manual, every bank must maintain five foundational program elements:

- Designated BSA Officer with a direct reporting line to the board of directors

- Written policies and procedures covering transaction monitoring, SAR filing, CTR filing, and customer due diligence

- Risk-based customer due diligence with documented enhanced due diligence guide procedures for high-risk customer categories

- Independent testing of the full AML program at least once per calendar year

- Ongoing employee training for both frontline staff and the BSA compliance team

The enhanced due diligence guide your institution follows should specify clear triggers for EDD reviews: high-risk geographic exposure, PEP status, cash-intensive businesses, and customers with prior SAR history.

Fintech BSA/AML on a Small Team

fintech bsa aml small team environments are genuinely challenging to operate. A lean compliance function at a growing payments fintech might handle thousands of automated alerts per month with no dedicated 314(b) coordinator on staff. The practical approach involves assigning 314(b) inquiry authority to senior AML analysts rather than junior reviewers, building a standard response template that satisfies safe harbor documentation requirements in under five minutes, setting a written policy that all inbound inquiries are acknowledged within 24 hours, and using kyc automation 2026 platforms that log and track 314(b) correspondence within the case management system automatically.

For teams managing aml compliance fintech programs with limited staff, integrating 314(b) inquiry capability into the existing alert workflow is far more sustainable than running it as a separate manual process alongside everything else.

KYC/CDD Requirements and Beneficial Ownership

kyc cdd requirements banks must meet under FinCEN's CDD Final Rule include identifying and verifying beneficial owners of legal entity customers to a 25% ownership threshold. This intersects directly with 314(b) practice: if a peer institution's inquiry response reveals different beneficial ownership information on file for the same legal entity, that discrepancy is itself a red flag warranting escalation, not merely a data reconciliation note to be logged and closed.

kyc cdd requirements banks must meet under FinCEN's CDD Final Rule include identifying and verifying beneficial owners of legal entity customers to a 25% ownership threshold.

Common Pitfalls and How Compliance Teams Can Avoid Them

Even well-resourced institutions make predictable mistakes with 314(b). Three issues surface consistently across examination findings and industry working groups.

Sharing without a documented suspicious activity basis. Section 314(b) is not a general background check tool. Inquiries must be connected to a specific suspected money laundering or terrorist financing matter. Sharing customer information without a documented internal trigger removes the safe harbor protection entirely and creates regulatory exposure.

Disclosing SAR existence. Confirming to a partner institution that you have filed a SAR on a shared subject is a federal violation. Train your AML team to describe suspicious transaction patterns and account behaviors without referencing SAR status in any form, even indirectly.

Letting registration lapse. FinCEN's annual renewal requirement is a hard cutoff with no grace period. Institutions that miss the renewal window cannot legally participate in 314(b) for the remainder of that calendar year. Add this renewal step to your standard bsa aml compliance checklist review process alongside your CTR filing rules compliance review and it will not get missed during busy Q4 cycles.

The sanctions screening automation strategy for CISOs covers adjacent compliance areas that regularly surface in the same investigations where 314(b) intelligence proves most valuable, particularly where cross-border wire activity and OFAC exposure overlap.

- Section 314(b) of the USA PATRIOT Act allows FinCEN-registered financial institutions to voluntarily share information about individuals, entities, and organizations suspected of money laundering or terrorist financing.

- The financial crimes that matter most, including trade-based money laundering, human trafficking networks, and state-sponsored sanctions evasion, almost always leave partial traces across multiple institutions.

- Registration is handled through FinCEN's Secure Information Sharing System (SISS).

- The honest reality is that legacy anti money laundering technology made 314(b) harder to use, not easier.

- sar filing is where 314(b) delivers its most measurable compliance value.

Onboard Customers in Seconds

Conclusion

314(b) information sharing banks implement as part of their AML programs is one of the few compliance tools that directly makes financial crime harder, not just compliance easier. When institutions share intelligence within the legal framework FinCEN has established, professional money launderers lose their core structural advantage of operating across institutional boundaries invisibly. The combination of active 314(b) participation, modern aml compliance software, automated sar filing workflows, and kyc automation 2026 platforms creates an intelligence network that no single institution could build independently. If your institution is not registered or has not submitted a 314(b) inquiry in the past 90 days, that is the starting point. Registration is free, the safe harbor is real, and the quality of your next aml compliance examination will reflect the difference.

For institutions looking to modernize the broader compliance infrastructure alongside 314(b), the DORA compliance automation strategy for risk heads in banking covers the regulatory technology shifts reshaping financial services compliance programs across 2026.

Share this article