.webp)

Listen To Our Podcast🎧

.png)

Introduction

28.4% of financial institutions now cite explainability and transparency as their most acute AI regulatory concern, according to Wolters Kluwer's Q1 2026 Banking Compliance AI Trend Report. That figure has moved in one direction every quarter since the Federal Reserve's SR 11-7 guidance was first extended to cover AI and machine learning systems.

Explainable AI in financial services is just not a technical upgrade. It's a control requirement. Banks that can't trace why a credit decision occurred, why a fraud alert triggered, or why a customer was flagged face examination findings that accurate models don't resolve.

The EU AI Act's August 2026 high-risk obligations, SR 11-7's lifecycle accountability expectations, and the Monetary Authority of Singapore's November 2025 consultation paper are converging on the same structural requirement: continuous monitoring, post-deployment oversight, and documented behavioral control across the full operational life of a deployed system, according to Horizon Search Institute's May 2026 analysis.

This blog covers five practices that determine whether explainable AI deployment actually survives regulatory scrutiny. Not just model validation, but live operation, audit review, and cross-role accountability. Each practice reflects how regulated teams evaluate AI in production, not how data science teams build it.

Practice 1 – Responsible AI Governance: Why Explainability Must Be a Defined Standard

Banks should formally define explainability within their AI governance framework, and that definition needs enforcement. It should specify where explanations are mandatory by decision type, how explanations are reviewed and by whom, and who holds accountability when an explanation fails regulatory scrutiny.

Banks follow very strict rules for using AI. Since 2011, the Federal Reserve and the OCC’s SR 11-7 has guided how banks manage model risk. Regulators also expect AI tools, including large language models and third-party services, to follow these rules, based on industry analysis from AegisAI published in May 2026.

Banks should formally define explainability within their AI governance framework. This means stating where explanations are mandatory, how they are reviewed, and who is accountable for them. High-impact use cases such as credit scoring, fraud detection, and compliance monitoring require consistent AI decision transparency by default.

When explainability is governed, institutions move closer to responsible AI and trustworthy AI adoption. Models become easier to validate, audit, and defend during regulatory reviews.

What this practice enforces ?

This governance standard covers four operational requirements.

First, clear policies specify which explainable AI use cases in banking require mandatory documentation. Credit decisions, fraud alerts, and compliance classifications each carry distinct regulatory documentation standards.

Second, consistent requirements for AI model transparency apply across internal teams and external vendors. This consistency reduces the audit issues that arise when different teams produce different explanation formats for equivalent decision types.

Third, defined ownership establishes accountability for explanation, approval, and escalation. Every production model has a named owner responsible for explanation accuracy.

Fourth, alignment with AI risk management connects explainability requirements to the institution’s existing control infrastructure, allowing governance to operate through established accountability structures.

FluxForce’s Agentic OS for Regulated Industries embeds these governance controls directly into AI workflow management, making explanation accountability operational by design and integrated into deployment workflows.

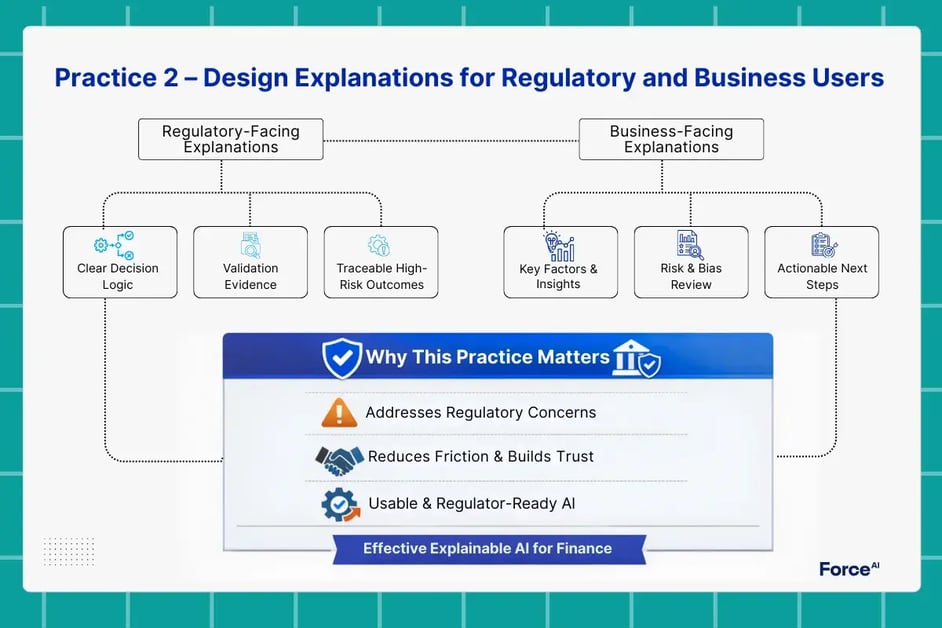

Practice 2 – AI Governance in Financial Services: Designing Explanations That Work for Regulators and Operators

Explainability fails when it assumes a single audience. In AI in financial services, regulators, risk leaders, and business teams interpret AI decisions differently. Effective deployment of explainable AI requires explanations that are tailored by role, not by model type.

Regulatory guidance and industry research, including recent CFA Institute analysis, highlight that supervisors expect explanations to support accountability, audit review, and post-incident investigation. They do not evaluate AI logic the same way internal data science teams do. This mismatch often leads to rework, delayed approvals, or model restrictions.

Regulatory-facing explanations

For compliance and supervisory review, explanations must support AI model transparency and AI auditability. This includes:

- Clear decision logic tied to input data

- Evidence supporting AI model validation outcomes

- Traceable reasoning for adverse or high-risk decisions

These explanations form the basis of AI compliance in finance and must remain consistent over time.

Business-facing explanations

Operational teams require model interpretability that supports action. Fraud analysts, credit officers, and risk managers need to understand why a decision occurred and what factors drove it. This supports AI risk management, bias review, and escalation workflows.

Why this practice matters ?

Research shows that lack of explainability remains a top regulatory concern for banks adopting AI. Designing explanations by stakeholder role improves trust, reduces friction, and supports trustworthy AI without sacrificing decision speed.

Banks that apply this practice deploy explainable AI in banking environments that are usable, defensible, and regulator-ready.

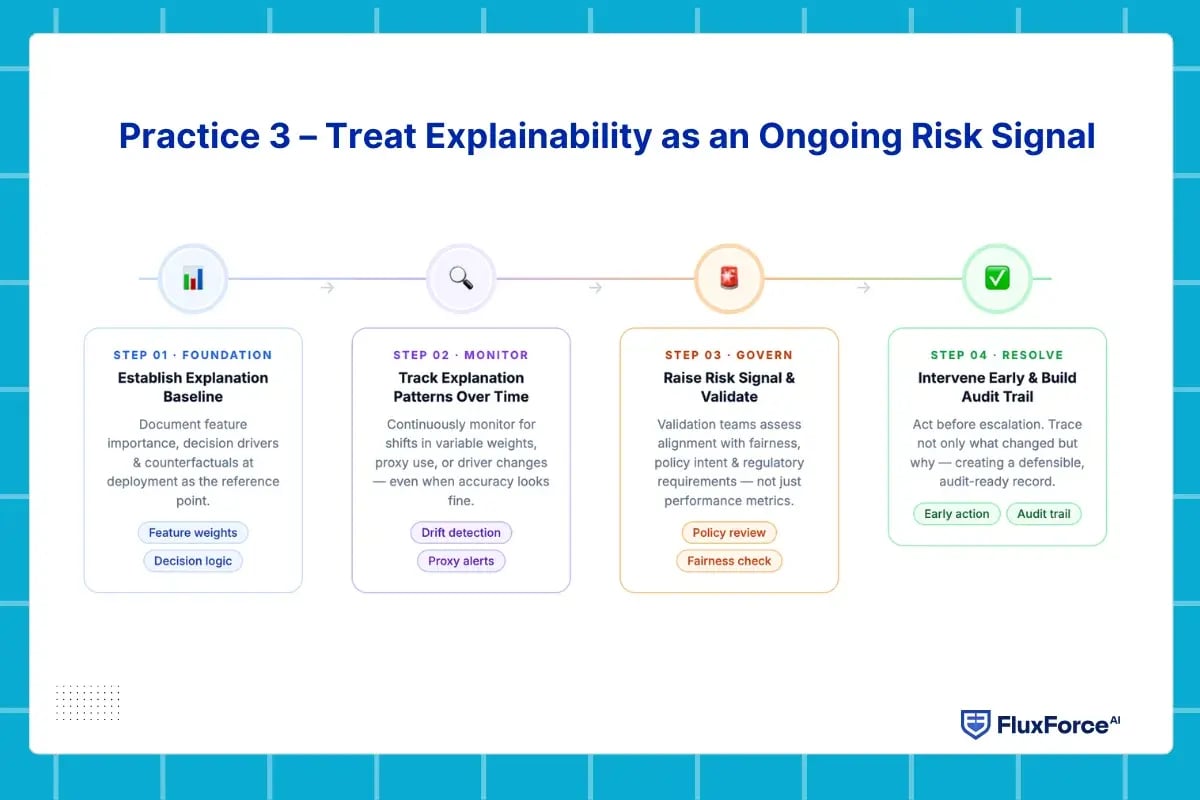

Practice 3 – Treat Explainability as an Ongoing Risk Signal

In financial systems, model risk rarely appears as a sudden failure. It develops gradually through small changes in data, customer behavior, or economic conditions. One of the most practical uses of explainable AI is identifying these shifts early, before they escalate into regulatory findings or operational losses.

In AI in financial services, a model can remain statistically accurate while drifting away from its original intent. When teams cannot see how decision logic evolves, risk accumulates silently.

Using explanations to detect emerging risk

Explanation monitoring turns a documentation tool into a live risk signal. When the feature importance ranking in a credit model shifts let’s say, geographic variables gain weight relative to financial ones. The SHAP attribution record shows these weeks before aggregate accuracy statistics reflect the change. Compliance teams can intervene based on evidence, not performance degradation.

This is especially relevant in artificial intelligence in banking, where policy changes and market conditions alter model behavior without triggering retraining. A model that correctly applied one set of assumptions in Q1 may apply different assumptions in Q3 due to data distribution shifts that no rule-based monitor would flag.

Strengthening model validation and oversight

From a governance standpoint, this practice strengthens AI model validation by adding behavioral context to performance review. Validation teams can ask whether decisions remain aligned with policy intent and fairness expectations. That's the question SR 11-7 examiners are asking when they review credit model governance, and it's the question fair lending examiners ask when they assess disparate impact.

Trustworthy AI: How Explainable AI for Fraud Detection and Credit Scoring Works at Scale

In many financial institutions, explainable AI is validated in isolation but disconnected from real decision environments. This creates a gap between model approval and daily use. In AI in financial services, explanations only become meaningful when they are available within the same systems where decisions are reviewed, challenged, and escalated.

Risk and compliance teams consistently flag this gap during audits. If explanations sit outside case management or monitoring tools, they cannot support defensible decisions at scale.

Enabling real-world AI decision transparency

Operational teams need concise, consistent explanations tied to individual outcomes. When explanations remain isolated in separate data science environments, they support documentation rather than decision-making. Auditors recognize that distinction immediately.

Explainable AI for Fraud Detection

In fraud operations, explainable AI for fraud detection works best when the alert and its explanation appear directly within the analyst’s existing workflow. An alert that says “risk score: 87” creates investigative workload. An alert that says “risk score: 87, transaction velocity 340% above customer’s 90-day average (35%), counterparty on OFAC watch list at 78% match confidence (28%), unusual session timing (22%)” enables a decision. The analyst can clear the alert in seconds or escalate it with documented reasoning. That distinction determines whether AI fraud detection reduces false-positive handling time or increases operational burden.

Explainable AI for Credit Scoring

In lending, explainable AI for credit scoring allows decision reviewers to assess fair lending alignment without reverse-engineering model outputs. AI systems used in credit decisions must comply with ECOA, and lenders must be able to explain adverse decisions and test models for potential discrimination, a requirement the CFPB has consistently enforced, according to InnReg’s AI in Financial Services compliance analysis. Consumer Financial Protection Bureau

When explanations identify the specific factors behind a denial, compliance reviewers can verify that those factors align with policy requirements and fair lending standards without involving the model development team.

Fair lending AI models that generate clear explanations also simplify the production of adverse action notices required under ECOA. These notices can include specific, ranked reasons connected to actual model logic rather than generic statutory codes that satisfy disclosure requirements only at a surface level.

Designing for performance and control

High-volume environments require speed. Mature deployments separate prediction execution from explanation delivery. The model scores transactions in milliseconds while the explanation generates in parallel. This hybrid structure allows machine learning explainability to operate without slowing transaction processing, addressing a common implementation concern and supporting explanation delivery directly within production workflows.

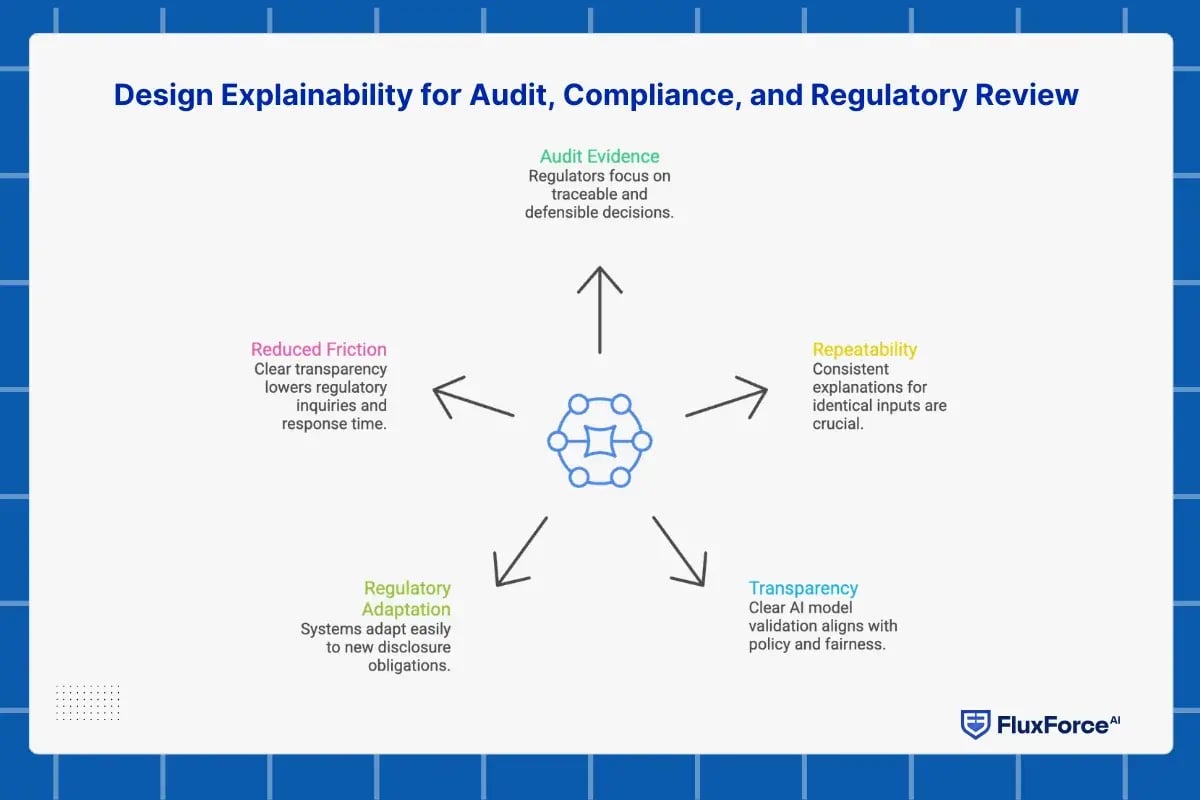

Design Explainability for Audit, Compliance, and Regulatory Review

Explainability carries the most weight when decisions are questioned after they are made. In AI in financial services, regulatory reviews often occur months after deployment, when teams must justify outcomes under real scrutiny. Explainable AI must therefore support retrospective analysis, not just real-time understanding. This practice focuses on aligning explainability with how audits and regulatory examinations actually function.

What regulators actually test in explainable AI systems

Audits evaluate evidence, not intent. Supervisors assess whether a specific decision can be traced, explained, and defended after the fact, for credit approvals, fraud alerts, and risk classifications.

FINMA's framework under the EU AI Act requires high-risk AI systems in the financial sector to meet specific explainability requirements, with obligations tied to risk management concepts and governance controls that closely align with DORA's IT-risk frameworks. Regulators aren't checking whether your system has an explanation capability. They're checking whether that explanation was captured at the moment of decision and can be reproduced on demand.

An explanation that exists only at runtime fails that standard. Examiners expect institutions to reproduce decision logic using the same model behavior and input data that existed at the time of execution. That means explanation records must be captured at the point of decision, linked to the model version in production, and retrievable without involving the data science team. During an examination, waiting three days for model output interpretation isn't an acceptable response.

Turning explainability into an audit control

For compliance teams, auditability depends on repeatability. Explanations must be consistent for identical inputs and linked to the approved model version used at the time of each decision.

The CFPB's January 2025 Supervisory Highlights specifically reminded institutions that using "black box" algorithms does not exempt them from providing explanations for credit decisions. CFPB examiners directed institutions to develop enhanced testing protocols, and where testing revealed prohibited basis disparities, required institutions to document the specific business needs their credit scoring models serve. That's not a documentation exercise. That's a requirement for traceable, defensible decision logic at the model level.

Strong explainability also strengthens model validation. Teams can assess whether decisions stayed aligned with policy intent across the review period, not just whether the model performed well at validation. This matters most in lending and transaction monitoring, where SR 11-7 requires continuous behavioral oversight, not point-in-time clearance.

Meeting regulatory expectations across regions

The EU deadline picture shifted in May 2026. The European Parliament and Council reached provisional agreement on the AI Omnibus, extending the compliance deadline for standalone high-risk AI systems, including credit scoring and fraud detection, to December 2, 2027, and to August 2, 2028 for AI systems embedded in products. The agreement should not be read as an invitation to pause AI governance efforts. The AI Act is already in force, and organizations are expected to be preparing now.

In the US, SR 11-7's model risk management expectations apply to AI systems at every regulated bank. In July 2025, the Massachusetts Attorney General settled a $2.5 million case against a lender whose AI underwriting models produced disparate impacts by race and immigration status, specifically because the institution failed to test its algorithmic models for disparate impact and couldn't document the business justification for the variables it used. That case matters beyond Massachusetts: it shows what examiner-level scrutiny of AI decision logic actually looks like in practice, regardless of which federal agency is leading enforcement at a given moment.

The FCA expects comparable explainability under Consumer Duty. Systems built for audit-ready explainability from day one adapt to new disclosure requirements faster than those that retrofit it later.

Conclusion

The five practices here reflect how regulated institutions actually evaluate AI governance: in production, under examination, under audit. Explanations must be mandatory where governance requires them, designed differently for regulators vs. operators, and stored as evidence. Monitoring must catch drift before performance statistics do. Production integration must put explanations where decisions get reviewed.

Agentic AI raises the bar. Chained models, sequential decisions, external data sources: the explainability requirements outpace what post-hoc attribution methods were designed for.

SR 11-7 is the ongoing obligation. ECOA, GDPR, and DORA add jurisdiction-specific requirements for institutions operating across markets. Banks treating explainability as a retrofit will scramble at every deadline to document decisions that were never designed to be documentable.

FluxForce is built for this. Explainability is a control embedded in the workflow from deployment, not appended afterward. Request a demo to see it in a production audit environment. For a broader look at where transparent and auditable AI systems are heading across banking and regulated industries, read “The Future of Financial AI: Transparent, Auditable, Explainable.”

Share this article