.webp)

Listen To Our Podcast🎧

Pig butchering scam detection is one of the hardest fraud challenges banks face today. Not because these schemes are technically sophisticated, but because they are deliberately designed to look like normal banking activity. Every wire transfer a victim sends is fully authorized. The customer calls their own bank to initiate the payment. There are no stolen credentials, no card-not-present anomalies, no velocity spikes that a standard rules engine would catch. According to FBI Internet Crime Complaint Center data, investment fraud losses in the US reached $4.57 billion in 2023, with pig butchering schemes representing the fastest-growing category. This post explains how ai fraud detection, behavioral analytics, and modern transaction monitoring software are helping compliance teams identify long-con investment fraud before victims lose everything.

What Is a Pig Butchering Scam?

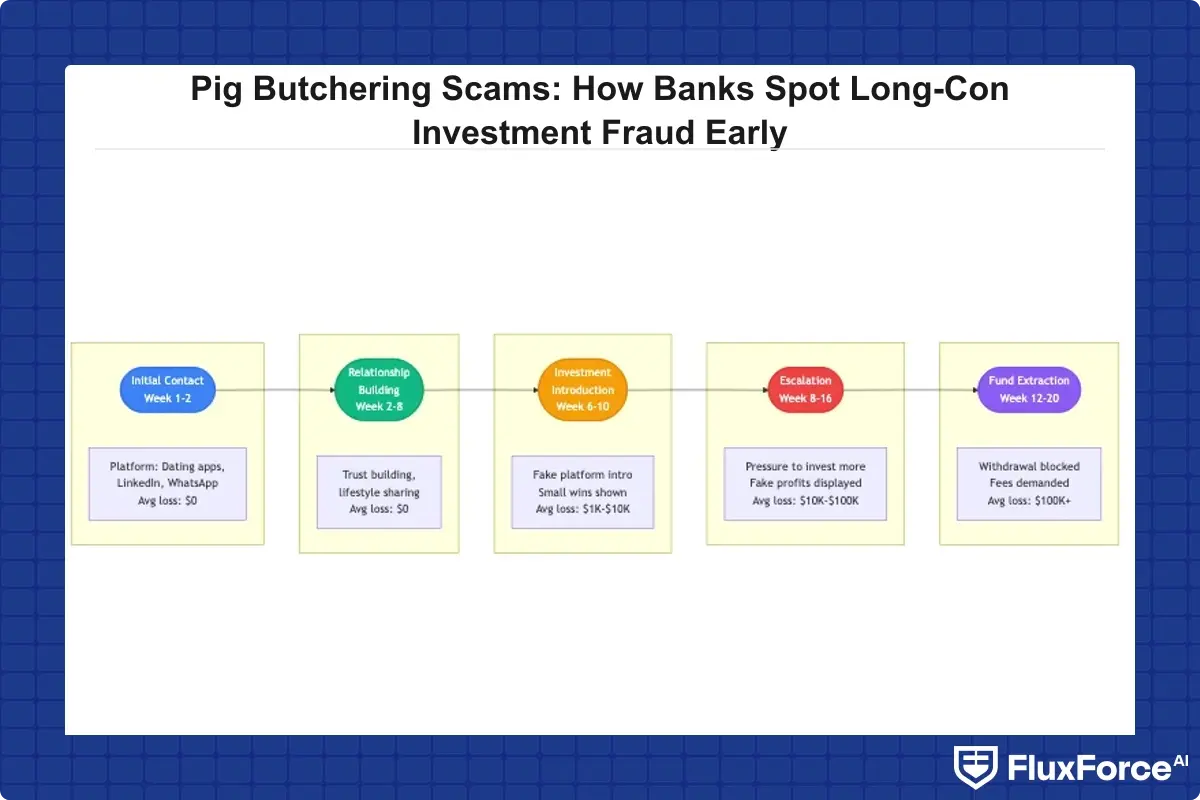

A pig butchering scam is a long-con investment fraud in which criminals groom victims over weeks or months through social media, dating apps, or encrypted messaging before steering them into a fraudulent trading platform. The name comes from the practice of fattening a pig before slaughter. The longer the grooming phase, the larger the eventual theft.

The defining characteristic of pig butchering is time. Most fraud that banks monitor for happens in hours or days. Pig butchering unfolds over 60 to 180 days on average, which means the behavioral signals are subtle and stretched across a timeline that most monitoring systems are not built to evaluate.

The Anatomy of a Long-Con Investment Fraud

The scam follows a predictable five-stage structure. First, a fraudster makes contact through what appears to be an accidental message, a LinkedIn request, or a dating app match. Second, they invest weeks building a genuine-feeling relationship with daily communication. Third, they mention their own investment success, usually in cryptocurrency or foreign exchange, and offer to share their approach. Fourth, they guide the victim onto what looks like a real trading platform, where early trades show impressive returns. Fifth, they encourage progressively larger deposits until the platform goes dark or demands withdrawal fees the victim cannot pay.

Initial deposits are typically $500 to $2,000. Final transfers before the fraud collapses frequently reach $50,000 to $500,000. That escalation pattern is one of the most consistent behavioral signals in documented pig butchering cases, and it is precisely the kind of signal that rules-based systems are blind to.

Scale and Financial Impact on Banking Customers

The Financial Crimes Enforcement Network (FinCEN) has identified pig butchering as a primary typology in its suspicious activity reporting guidance, noting that the fraud is disproportionately under-reported because victims often do not realize they have been defrauded until weeks after the final transfer. Estimated global losses exceeded $75 billion between 2020 and 2024.

For a mid-tier bank with 2 million retail customers, statistical modeling suggests 400 to 600 active pig butchering cases at any given moment. Average losses per victim consistently exceed $120,000. Those are not numbers a compliance team can afford to miss, and they are not numbers that rules-based transaction monitoring was designed to catch.

How Pig Butchering Scams Evade Traditional Detection

Standard transaction monitoring software is built around thresholds and rules: alert when a wire exceeds a set amount, flag velocity spikes, check new payees against known-bad destination lists. Pig butchering defeats every one of those mechanisms, not accidentally but by design.

Rules-Based Systems and Their Blind Spots

A rules engine flags a $50,000 wire to a new payee because it crosses a threshold. A pig butchering operation routes that same $50,000 as four separate $12,500 wires over three weeks, each to a slightly different entity name, all staying below alert thresholds. By the time the total exposure is visible in the data, the money is already multiple crypto hops away.

The second problem is fraud alert fatigue. Analysts reviewing 200 to 400 alerts per day develop processing patterns that prioritize recognized fraud types and deprioritize patterns that do not fit established templates. Pig butchering does not fit any template a rules engine was built around, so cases tend to get cleared without escalation. This is not analyst error. It is an inevitable consequence of high-volume alert queues that do not surface the right contextual signals.

Synthetic identity fraud compounds the problem on the receiving end. Pig butchering operations frequently route victim funds through accounts opened with fabricated identities, held 90 to 180 days to build a clean transaction history, then used for a single large inbound wire before abandonment. Detecting synthetic identity fraud in real-time is already difficult on its own. When layered on top of a pig butchering victim pattern, both the send-side and receive-side detection break down simultaneously.

The Crypto Layering Problem

Most pig butchering transfers eventually route to cryptocurrency exchanges. Funds land in a custodial account at a legitimate, regulated exchange and are then quickly converted and moved to self-custodied wallets or privacy coins. The crypto exchange destination is not a fraud indicator on its own. Millions of legitimate customers transfer money to digital asset platforms every week.

The pig butchering scam detection problem is distinguishing the customer who has genuinely decided to invest in cryptocurrency from the customer being manipulated into sending funds they will never recover. Rules cannot make that distinction. Behavioral context can.

How Does AI Detect Fraud in Long-Con Investment Schemes?

AI fraud detection explained: machine learning models build a behavioral baseline for each account individually, then score every new action against that baseline in milliseconds. A transaction that matches the customer's historical pattern gets a low risk score. A transaction that deviates sharply from that baseline, even if it falls below rule thresholds, gets a high score and enters a review queue.

For pig butchering, this matters because the behavioral shift is real and measurable. A customer who has never sent an international wire, has no prior interaction with a crypto exchange, and has maintained a stable transaction pattern for four years is exhibiting a meaningful anomaly the first time they send $8,000 to a digital asset platform. A rules engine misses it because $8,000 is below threshold. A machine learning model flags it because it represents a 6-sigma deviation from that specific customer's own four-year history.

Machine Learning Fraud Detection: Behavioral Baselines

The core of machine learning fraud detection for pig butchering is customer-level entity modeling. Instead of comparing a transaction against population averages, the model compares it against that specific customer's own history across a 90 to 180-day lookback window. Key features include average transfer amount and standard deviation, payee diversity and new payee frequency, time-of-day patterns, channel usage (branch versus app versus online), and geographic spread of transaction destinations.

When a pig butchering victim enters the investment phase, multiple feature clusters change simultaneously. That co-occurrence of deviations across several behavioral dimensions is something a rules engine cannot evaluate. A gradient boosting or neural network model catches it at the first or second anomalous transaction, before the escalation pattern has fully formed.

AI Fraud Detection Explained: Graph Analysis and Network Signals

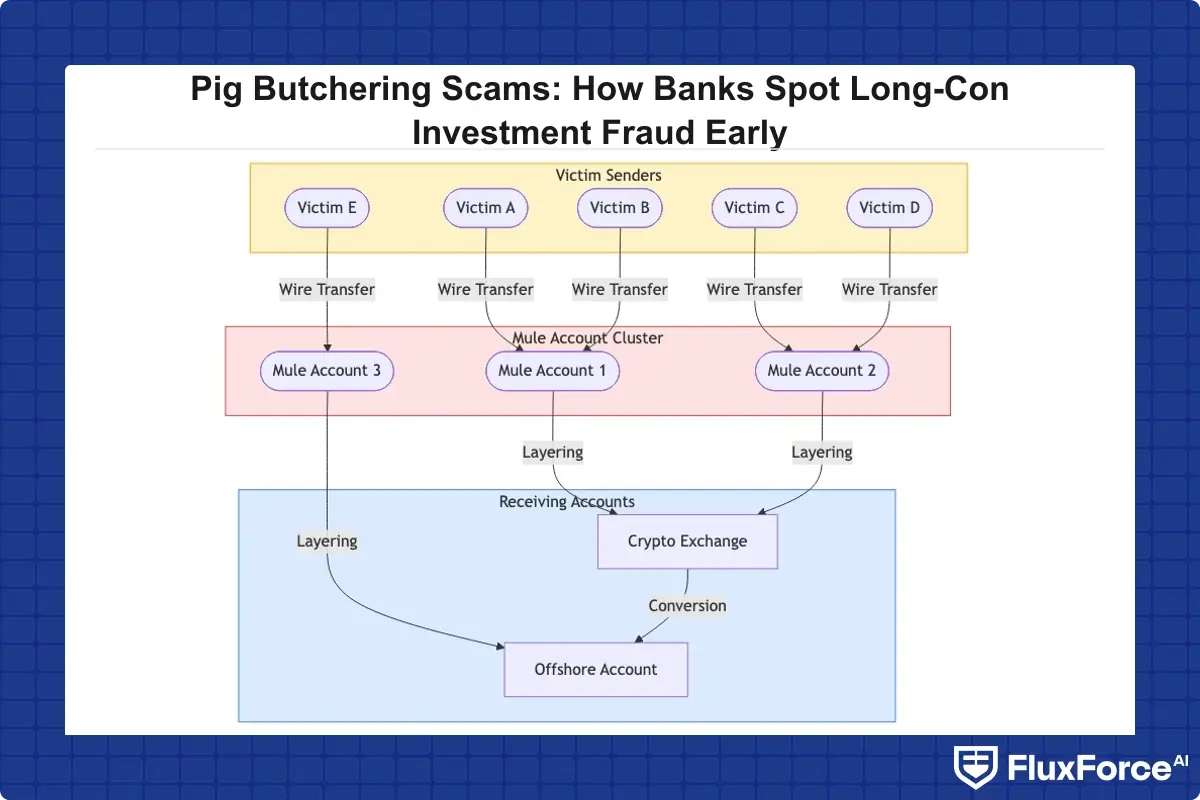

Beyond individual account behavior, ai fraud detection in banking increasingly relies on graph analysis to map relationships between accounts. A pig butchering operation typically uses 10 to 50 receiving accounts linked by shared device IDs, IP addresses, phone numbers, or application timing patterns.

When a customer sends money to what appears to be a legitimate investment platform, a graph model can check whether the receiving account has received funds from dozens of other customers at the same institution over the past 90 days, whether those senders share behavioral characteristics, and whether the receiving account's own history matches a known mule pattern. This network-level signal is invisible to rules-based systems but is one of the strongest indicators that ai fraud detection software purpose-built for investment fraud can surface.

Real-Time Fraud Detection at the Wire Transfer Layer

Real-time fraud detection means scoring a transaction before it is released for processing, typically within 200 to 500 milliseconds. For pig butchering, the model needs to score not just the transaction in isolation but the trajectory: is this the third transfer to the same destination in six weeks? Is the amount 40% larger than the previous one? Does the customer's digital activity show unusual patterns, like a sudden increase in mobile banking logins after years of branch-only behavior?

The institutions getting this right are running AI-powered fraud detection software that combines real-time transaction scoring with historical sequence modeling, so the system is not just asking whether a single transaction is suspicious, but whether it is the fourth step in a suspicious behavioral trajectory.

Real-Time Fraud Detection Banks Use to Stop Pig Butchering Early

Real-time fraud detection banks deploy most effectively combines three layers: transaction-level ML scoring, customer journey analytics, and a human review workflow that places an analyst in front of a flagged case within 24 hours of the first anomalous signal. Getting all three working together is harder than enabling any one of them individually.

How AI Fraud Detection in Banking Triggers the Right Alerts

The alert generation problem for pig butchering is a precision-recall tradeoff. A model tuned for maximum sensitivity generates an alert on every first wire to a new payee, flooding the analyst queue and creating the same fraud alert fatigue problem that plagued the rules-based system it was meant to replace. A model tuned for maximum specificity misses early-stage cases that are still preventable.

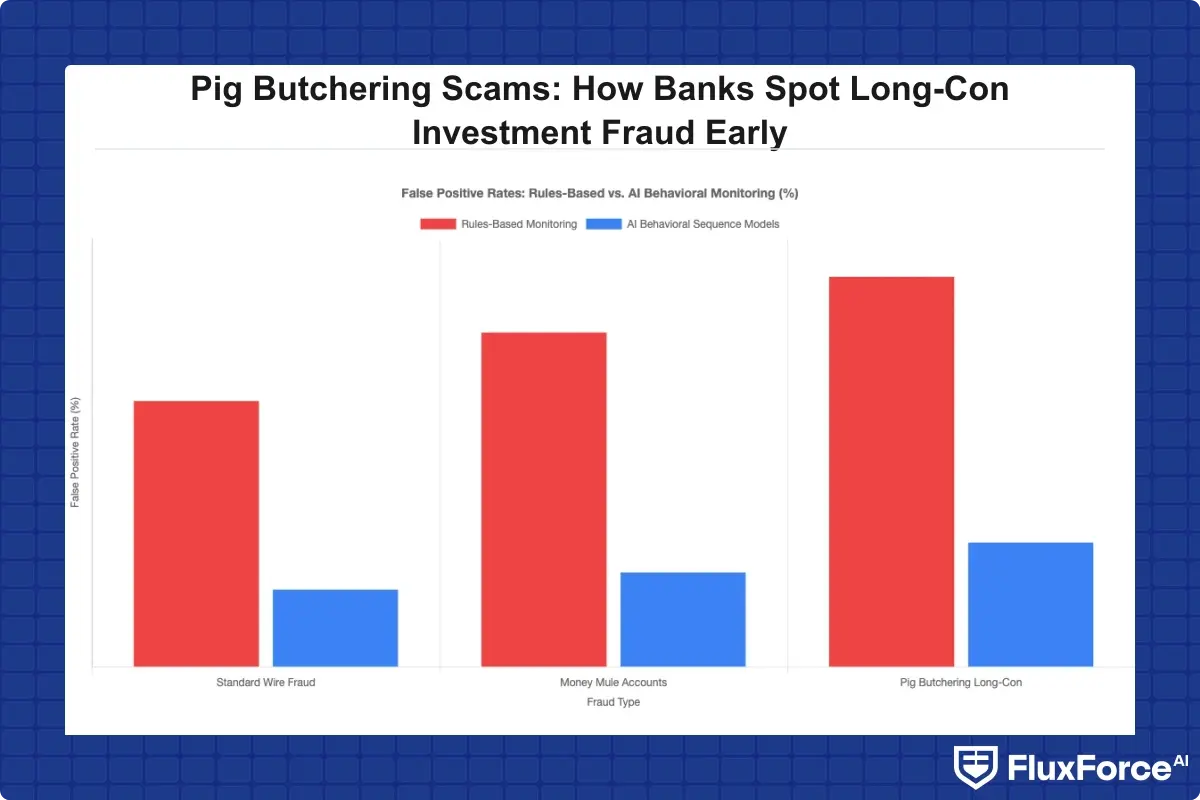

The configurations with the best measured performance maintain a false positives fraud detection rate below 15% on pig butchering-specific alerts by using a composite score: behavioral deviation combined with network risk and destination risk. Any two of the three scores exceeding threshold triggers an alert. This reduces noise significantly compared to single-score thresholds while maintaining detection coverage on true positive cases. For a detailed comparison of detection architectures, AI vs. Traditional Fraud Detection: Key Differences Every Risk Officer Should Know covers the tradeoffs clearly.

Automated Transaction Monitoring Workflows

Automated transaction monitoring for pig butchering works best when the alert workflow includes case enrichment before it reaches an analyst. By the time a human reviews a case, the system should have already pulled: all transactions to the same destination across the full customer base, the customer's 90-day behavioral history, any prior fraud flags or SAR filings on the destination account, and customer service notes from the past 30 days.

An analyst with that enriched context makes a decision in 8 to 12 minutes and produces higher-quality SAR filings. An analyst starting from scratch takes 45 minutes and generates lower-quality outputs. FinCEN has noted that SAR quality on long-con investment fraud is systematically lower than on other fraud types, which directly affects law enforcement's ability to disrupt pig butchering networks at scale.

How to Reduce False Positives in Transaction Monitoring

This is where pig butchering detection programs get expensive if not built carefully. The cost of a false positive is not just analyst time. It includes customer friction, complaint handling costs, and the risk of losing a customer whose legitimate transaction was blocked without adequate justification.

The False Positive Cost Fraud Teams Actually Pay

False positive cost fraud teams face breaks into three components: direct analyst labor at $35 to $65 per case reviewed, customer experience degradation estimated at $40 to $120 per unnecessary friction event based on customer lifetime value models, and regulatory cost when false positive rates attract examination attention. For a bank generating 10,000 monthly fraud alerts with a 40% false positive rate, the annual operational cost sits between $3.5 million and $7 million before accounting for customer churn effects.

The false positive rate fraud detection teams should target for pig butchering-specific monitoring is below 20% on the analyst-facing alert queue. Achieving this requires composite behavioral scoring as a pre-filter rather than routing every threshold breach to a human reviewer. How Agentic AI Fraud Agents Cut False Positives by 80% covers the agentic workflow layer that makes this pre-filtering practical at scale.

How to Reduce False Positives in AML Programs

How to reduce false positives in AML is a systems-level challenge, not just a threshold-tuning exercise. The interventions with the largest measured impact are:

- Customer-level segmentation: Apply different alert thresholds for distinct risk profiles. A high-net-worth customer who regularly makes large international transfers needs a different behavioral baseline than a retail customer who has never sent a wire.

- Analyst feedback loops: Every analyst decision, whether clearing, escalating, or filing a SAR, must feed back into the model as a labeled training example. Without this loop, models drift and false positive rates climb over 12 to 18 months.

- Destination reputation scoring: Maintain a live risk score for payee destinations that updates based on incoming fraud reports and network analysis. A destination appearing in 15 pig butchering cases last month carries materially higher risk than one appearing in zero.

- Sequence context scoring: Score transactions in the context of the preceding 30 to 90 days, not in isolation. A single $15,000 wire may be low risk. The same wire preceded by two $8,000 wires over six weeks is a meaningfully different pattern.

These four changes together typically reduce analyst workload by 40 to 60% on pig butchering alerts while maintaining or improving detection coverage. Reducing False Positives: Rule-Based Systems vs. AI-Driven Solutions benchmarks the performance difference across implementation approaches in detail.

Transaction Monitoring Software: Sardine vs Unit21 and the AI Layer

The sardine vs unit21 comparison surfaces in almost every fraud team RFP process for automated transaction monitoring, and it is worth addressing directly for pig butchering detection capability. Both platforms offer rule-based monitoring augmented with machine learning, but the differentiators for long-con investment fraud are specific and worth understanding before you commit to an implementation path.

What Sardine vs Unit21 Means for Pig Butchering Detection

Sardine's approach is device and behavioral biometrics-first. Its monitoring layer captures how a user interacts with their device: typing cadence, scrolling behavior, session duration, and navigation patterns. For pig butchering, where a victim uses their own device but is being coached through transactions by a scammer via a separate call or message thread, this layer can surface the anomaly of a customer spending three hours on a mobile banking session they normally complete in four minutes.

Unit21's strength is in case management and analyst workflow tooling. Its alert enrichment integrations reduce the time-to-decision on complex multi-transaction cases like pig butchering, where context from multiple data sources is required before an analyst can reach a quality decision. The platform's custom rule-building layer allows fraud teams to add pig butchering-specific logic on top of the base ML scoring model.

For most mid-tier banks, neither platform is a complete solution for pig butchering detection without significant customization. The behavioral sequence modeling for long-con fraud requires training on your own customer data across a 180-day lookback window, not just enabling a vendor-provided feature.

AI Fraud Detection Software Evaluation Criteria

When evaluating ai fraud detection software specifically for pig butchering, the criteria that carry the most weight are:

- Lookback window length: Can the model maintain a behavioral baseline over 180 days? Some platforms cap at 30 or 60 days, which is insufficient for fraud that unfolds across months.

- Graph analysis capability: Does the platform include native network analysis, or does graph modeling require a separate vendor integration?

- Feedback loop tooling: How easily can analyst decisions feed back as training labels? Weak feedback mechanisms produce model drift within 12 months, and false positive rates climb accordingly.

- Transaction monitoring cost at scale: What is the per-alert and per-account pricing model? High false positive rates on pig butchering models can generate unexpectedly large transaction monitoring cost if pricing is alert-volume-based.

For teams working through the build-versus-buy decision on fraud detection infrastructure, the framework in Card Fraud Analytics: AI-Powered Fraud Detection Strategy for Risk Heads addresses the core tradeoffs directly.

Onboard Customers in Seconds

Conclusion

Pig butchering scam detection requires a fundamentally different approach than most fraud programs are built for today. The fraud operates below rule thresholds, spreads its behavioral signals across a 60 to 180-day timeline, and involves fully authorized transactions from customers who believe they are making rational investment decisions. Rules-based automated transaction monitoring will not catch it consistently.

The path forward combines ai fraud detection models that build individual behavioral baselines, graph analysis that surfaces network-level signals on receiving accounts, and a proactive customer outreach workflow that can interrupt the fraud chain before the final large transfers are executed. Payment fraud prevention at this level requires real investment in tooling, feedback loops, and analyst workflow design. The alternative is absorbing six-figure losses per case and watching customers lose their savings to operations that spent months earning their trust. The technology to catch pig butchering early exists today. The question is whether your compliance program is configured to use it.

Share this article