.webp)

Listen to our podcast 🎧

Introduction

Payment AI models make thousands of decisions every minute. Most are correct. But when one isn't — a genuine customer blocked, a risky transfer approved and the question that follows is always the same: why did the model do that?

Financial institutions depend on AI Model Monitoring to evaluate every transaction in seconds. Yet many payment teams cannot clearly explain why a model blocked a genuine customer or approved a risky transfer. That gap is where compliance disputes start, where regulators push back, and where customers lose confidence in the institution's automated systems. Speed still matters. But a fast decision with no explainable reasoning is one audit away from becoming a serious problem.

The trust gap inside payment decisions

AI in payment processing analyzes hundreds of variables per transaction. The output is a risk score. The reasoning behind that score like which variables dominated, which patterns triggered the flag, what changed compared to this customer's normal behavior, stays inside the model. Risk and compliance teams don't see it. Auditors ask for it. And when organizations can't produce it, automated monitoring stops being a capability and starts being a liability. Explainable AI XAI addresses this problem by revealing how models interpret risk signals and how those signals change over time.

Fraud methods evolve quickly, and models can drift without notice. Real time fraud detection requires continuous visibility into model behavior, not occasional reviews. Institutions need monitoring that shows what the model learned, why performance shifted, and how to correct it before customers are affected. AI Model Monitoring supported by explainability builds this discipline and helps payment leaders balance speed, accuracy, and compliance.

AI model monitoring with explainability closes that gap. Not by slowing decisions down. By making every decision traceable, reviewable, and defensible the moment someone asks.

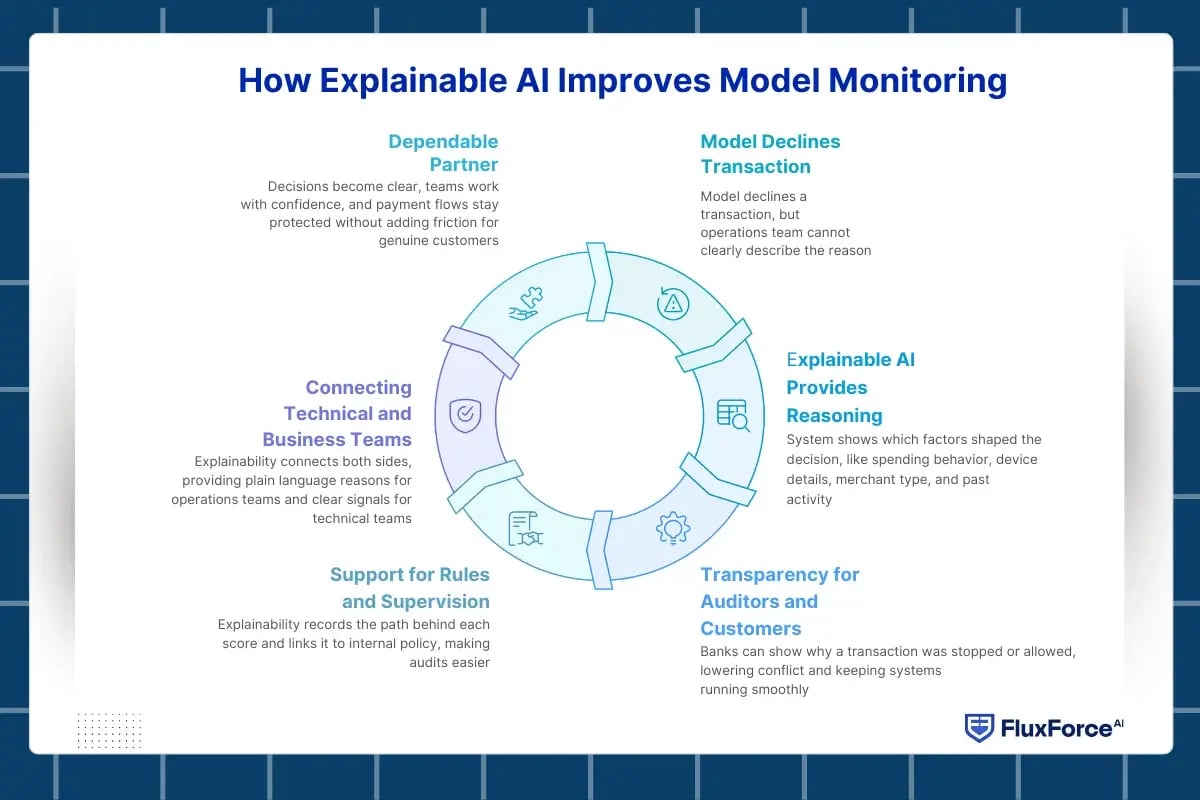

How Explainable AI Improves Model Monitoring ?

Why do teams still hesitate to trust AI decisions in real time payment systems?

Most monitoring tools show numbers but do not explain meaning. A model may decline a transaction, yet the operations team cannot clearly describe the reason to auditors or customers. This gap slows response and creates risk. How explainable AI improves model monitoring matters because monitoring must provide clear reasoning, not only alerts on a screen.

Explainable AI for payments changes the way teams view model results. Instead of a simple approve or decline signal, the system shows which factors shaped the decision. Spending behavior, device details, merchant type, and past activity become visible parts of the story. AI Model Monitoring then turns into a practical tool that helps investigators decide the next step.

From alerts to understanding

Explainable AI for payments changes what teams actually see when a model fires. A decline isn't just a score anymore. The system surfaces the specific factors that drove it: a spending amount 340% above this customer's 30-day average, a device that hasn't been seen on this account before, a merchant category that historically correlates with high dispute rates for this customer profile. AI model monitoring stops being a scorecard and becomes a working tool. Investigators don't have to guess. The reasoning is attached to the decision.

Transparency as everyday protection

Payment teams need to act fast, and they need to be able to justify what they did. Those two requirements used to conflict. Speed meant less documentation. Documentation meant slower decisions. AI transparency in payments resolves that conflict by generating the justification automatically, at the point of decision. When a customer calls to ask why their payment failed, the service team doesn't need to contact the fraud team, wait for an investigation, and call back. The explanation is already on record. That reduction in internal friction is measurable with fewer escalations, shorter handling times, and fewer repeat contacts in the same case.

Support for rules and supervision

AI governance in financial services demands evidence that models follow those rules day after day. With model monitoring in real time, explainability records the path behind each score and links it to internal policy. Audits become easier because teams can present simple and direct reasons for their actions.

Bringing technical and business teams together

Data scientists and compliance officers looking at the same model alert currently see two different things. One sees feature weights and confidence intervals. The other sees a decision that needs to be defensible under payment regulations. Without a shared layer, both teams spend time translating for each other rather than acting. Explainability in AI model monitoring creates that shared layer. Operations teams get plain-language reasons they can act on. Technical teams get structured feedback about which decisions are being questioned, which informs retraining. And compliance teams get documentation that already maps model logic to policy language. The investigation that previously took three people and two days takes one person and twenty minutes.

Real-Time AI Monitoring for Financial Transactions

Real time payment systems do not pause for reviews or weekly checks. Transactions flow across cards, wallets, and instant transfers throughout the day. If monitoring waits for end-of-day reports, the damage is already done. Real-time AI monitoring for financial transactions ensures that model behavior is examined at the same speed as money movement.

From an AI model’s dashboard point of view, understand how explainable AI strengthens model-driven fraud monitoring in live payment environments.

Beyond simple performance numbers

Approval rate and fraud percentage are the metrics most institutions track. They're also the last metrics to move when something goes wrong. By the time those numbers shift, the underlying problem has typically been running for days or weeks. Real AI model monitoring watches the leading indicators: the signals that change before performance metrics do.

- Are risk scores stable across channels?

- Are certain merchants suddenly receiving unusual decisions?

- Is customer behavior being interpreted correctly?

- Are input data fields arriving with the same quality as before?

Answering these questions protects revenue and customer trust at the same time.

Understanding decisions instead of counting alerts

When alert volume spikes, the first question is whether it reflects a genuine fraud wave or a model that's started misreading normal behavior. Without explainability, the only way to answer that is to pull a sample of flagged transactions, manually review each one, and draw conclusions from a subset that may not represent the full pattern. That process takes hours and still produces uncertainty. With explainability embedded in AI model monitoring, investigators see the decision drivers for every alert immediately. They can assess whether the model is responding to genuine risk signals or to noise within minutes, not hours. That difference matters at scale: an alert queue that takes eight analysts a full shift to clear with manual review takes two analysts two hours when the reasoning is already attached.

Model drift detection in real time

Payment environments evolve constantly. Holiday seasons, new products, or changes in customer habits can confuse even well-built models. Model drift detection in real time compares current outcomes with established behavior and highlights early warning signs such as:

- Gradual increase in customer complaints

- Sudden change in approval mix

- Different results for similar profiles

- Unusual concentration around specific devices or regions

How explainability reduces drift risk in live risk engines — including what governance structures catch it earliest — is covered in depth in our post on AI drift in real-time risk engines.

Operational rhythm for payment teams

Effective AI model monitoring is a daily operational discipline. In practice, that means reviewing explanations for the highest-risk decisions from the previous 24 hours every morning — not the scores, the reasoning behind them. It means comparing today's decision pattern against last week's baseline for the same transaction types. It means validating that the reasons the model is giving still match the policy rules the compliance team approved. And it means capturing investigator feedback on disputed decisions and routing it back to the model team, so the system improves from operational experience rather than only from retraining cycles.

Teams that follow this rhythm catch drift weeks earlier than teams that check accuracy metrics. They also produce significantly better documentation for regulatory review, because the record of daily oversight exists as a natural output of the process.

Linking monitoring with compliance needs

Every payment decision becomes an audit record. When regulators, auditors, or customers review a transaction, institutions need a clear view of the full decision path, including the data the model received, the score it generated, the policy rule applied, and the resulting action. Real time monitoring with explainability captures this information automatically at the moment of decision, indexes it by transaction ID, and makes it instantly retrievable. This creates faster investigations, stronger compliance operations, and reliable audit documentation.

Real-time monitoring supported by explainability protects both sides of the payment equation. Customers receive smoother experiences, and banks gain clear control over automated decisions without slowing innovation.

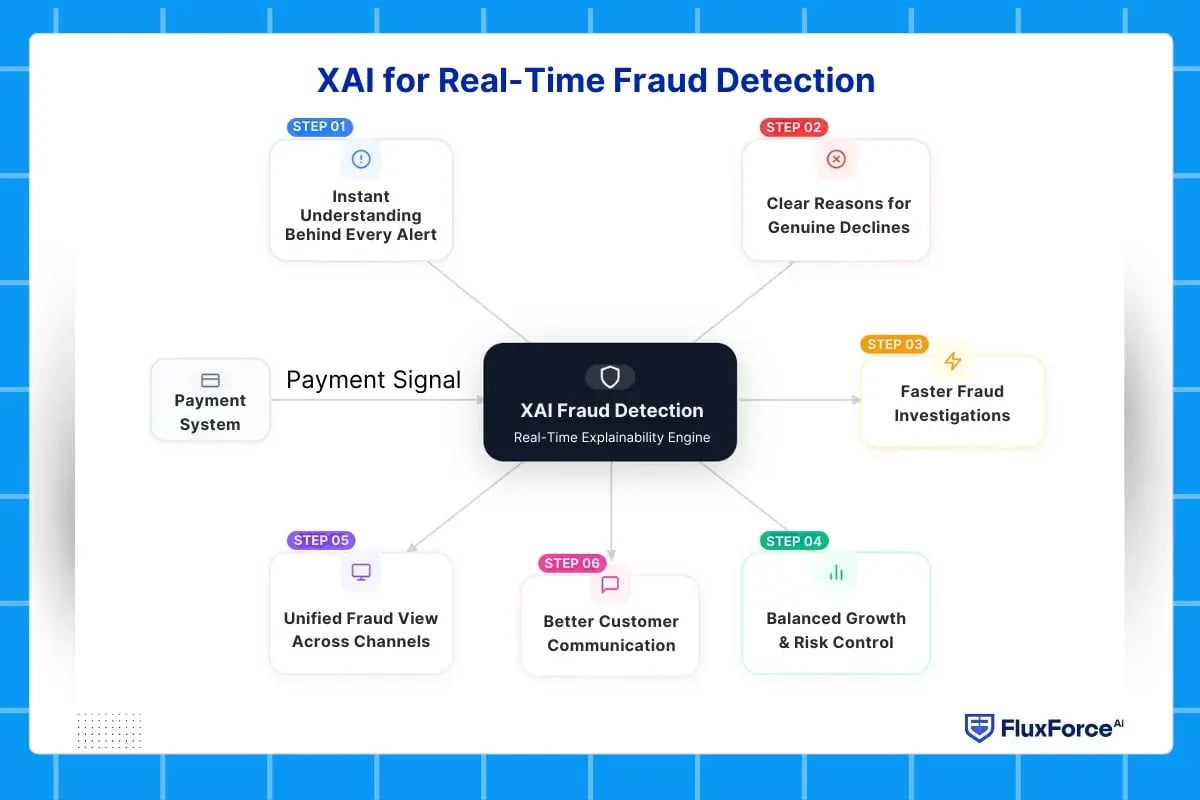

XAI for Real-Time Fraud Detection

Fraud detection in real time payment systems no longer depends only on identifying risky transactions.

Banks need to understand the reason behind every alert before taking action. Explainable AI connects detection with reasoning, helping teams see what the model observed and why a payment was flagged. This clarity improves speed, accuracy, and customer trust while keeping controls aligned with compliance.

Instant understanding behind every fraud alert

In real time payment systems, alerts arrive continuously, but a risk score alone does not guide action. XAI for real-time fraud detection reveals the exact signals that influenced the model, such as transaction behavior, device consistency, location patterns, and past activity. Operations teams move from reacting to alerts toward understanding the logic behind them.

Clear reasons for genuine payment declines

Legitimate payments often fail because models rely on broad correlations that remain hidden from users and analysts. Explainability exposes the specific factor that triggered the decision and shows whether that factor truly represents risk. This insight allows banks to refine controls instead of applying rigid blocks across all customers.

Faster investigations for fraud analysts

The typical fraud investigation without explainability follows the same inefficient path: open the transaction record, switch to the customer profile system, check the device history in a third tool, pull recent alerts from a fourth, then manually assemble a judgment. That sequence takes five to fifteen minutes per case. Multiply that by 200 alerts per analyst per shift, and a significant portion of working time is spent on context gathering rather than decision-making.

With explainability embedded in AI model monitoring, that context arrives with the alert. The main drivers behind the risk score are ranked by contribution. Comparable historical transactions are surfaced automatically for reference. The customer's recent behavior timeline is visible in the same view. And a plain-language summary of the decision is available for case documentation without requiring the analyst to write it from scratch. Investigation time per case drops. Consistency across analysts improves. And the documentation produced as a byproduct of each investigation is already formatted for compliance review.

Better communication with customers

Customer support teams need simple and accurate explanations when a payment fails. Explainable AI for payments provides human-readable reasons without exposing sensitive model logic. Clear communication reduces frustration, repeat queries, and chargeback disputes.

Balanced growth and risk control

Payment businesses aim to increase approvals without inviting fraud. Explainability shows how each rule or model change affects outcomes before deployment. Product and risk teams can expand to new segments with confidence instead of trial-and-error decisions.

Unified fraud view across channels

Cards, instant transfers, wallets, and merchant payouts each generate different data signals and operate under different transaction patterns. A behavior that's normal for a card transaction (high frequency, small amounts) might look suspicious in an instant transfer context. A model that treats all channels with the same scoring logic will produce inconsistent outcomes like too many false positives in one channel, too much fraud tolerance in another.

XAI creates a common interpretation layer across all channels: the same explanation format, the same decision factors reviewed consistently, the same policy rules applied and documented. This means a fraud analyst can review an alert from any channel and immediately understand the decision logic without needing to understand the specifics of that channel's model. It also means compliance can verify channel consistency in a single review rather than running separate assessments for each payment type.

How to Detect Model Drift in Payment Systems ?

Payment behavior never stays constant. New merchants, seasonal spending, and changing fraud tactics slowly shift the data that AI models rely on.

When this shift goes unnoticed, approval rates fall and false alerts rise. Explainability strengthens AI model monitoring by showing not only that drift occurred, but also where and why it started.

Behavioral signals that indicate drift

Drift doesn't announce itself with a performance alert. It appears first in explanation patterns. The same customer profile that scored as low-risk three months ago now scores as medium-risk, but the transaction behavior hasn't changed. A merchant category that generated occasional flags now generates frequent ones, but no new fraud pattern has been confirmed. An input field that used to be a minor contributor to the risk score is now the dominant driver.

These shifts are invisible in accuracy metrics until they've accumulated enough volume to move the numbers. But they're visible in explanation data immediately. Model drift detection in real time, backed by explainability, catches these pattern changes as they emerge, often two to four weeks before they show up in approval rate or fraud percentage.

Understanding the cause behind performance drop

Traditional monitoring only reports declining accuracy. XAI connects the decline to specific features such as merchant category, geography, or payment method. Teams can see whether the change comes from genuine customer behavior or from a new fraud strategy. This understanding prevents blind retraining.

Continuous validation inside payment gateways

Monitoring AI models in payment gateways requires daily validation. Explainability tracks which factors influence approvals across millions of transactions. If a single rule begins to dominate decisions, governance teams receive clear evidence that the model is losing balance.

Collaboration between risk and data teams

Explainability creates a shared view for different functions. Data scientists analyze technical metrics, while risk managers review business impact. The same explanation layer serves both groups, turning AI risk management in fintech into a coordinated process instead of isolated reviews.

Safe retraining decisions

Retraining a payment model is a risk event. A full retrain on new data can resolve drift in one segment while introducing instability in another. Without explainability, the decision of how much to retrain and which population to retrain on is based primarily on aggregate performance metrics.

Explainable AI (XAI) makes retraining a surgical decision. Before retraining, teams can identify exactly which segments, merchant categories, or behavioral patterns are driving the performance gap. They retrain on targeted data. After retraining, they can compare the explanation patterns from the new model against the previous version segment by segment, confirming that improvements in affected areas didn't create new anomalies elsewhere. Banks that manage retraining this way report significantly fewer post-deployment issues and faster stabilization times compared to institutions that retrain on full data without segment-level explainability review.

Regulatory readiness through documented reasoning

Regulators reviewing payment AI systems want to see two things: that the institution detected when model behavior changed, and that it responded in a documented, controlled way. "We noticed the accuracy metric dropped and ran a retrain" doesn't satisfy that expectation. What satisfies it is a complete change record: when the shift appeared in explanation patterns, which segments were affected, what analysis was performed, what retraining decision was made, who approved it, and how post-deployment monitoring confirmed stabilization.

When every drift event includes an explanation trail automatically, that change record is a byproduct of normal operations rather than a retroactive assembly exercise. Under DORA's operational resilience requirements and the EU AI Act's model oversight provisions, institutions that can produce this documentation on demand are in a fundamentally different regulatory position than those that can't.

Conclusion

Real time payment systems demand speed, accuracy, and accountability at the same time. Traditional monitoring methods can detect anomalies, but they often fail to explain them. Explainable AI changes this by connecting every model decision with clear reasoning. AI model monitoring becomes a business capability instead of a technical checkpoint.

Banks that adopt explainability gain stronger control over fraud detection, compliance, and customer experience. Teams understand why a payment is blocked, how risk scores are formed, and when models begin to drift. This understanding reduces false positives, protects revenue, and builds trust with regulators and users.

The future of payments depends on systems that are both intelligent and transparent. XAI ensures that innovation does not come at the cost of governance. Financial institutions that combine real time analytics with explainability will manage risk with confidence and scale digital payments without losing visibility.

Share this article