Listen to our podcast 🎧

Introduction

90% of insurance fraud conversations start at the claims stage. The reason why it happens is because: that is where the loss becomes visible, that is where pressure builds, that is where decisions feel urgent.

But risk does not begin at claims. It begins much earlier, during policy issuance, where identity is accepted, risk is priced, and assumptions are locked into the system.

Across insurers, a familiar pattern keeps repeating. AML checks are performed. KYC compliance is documented. Systems appear aligned. Yet, months later, claims teams face identity mismatches, unusual payout behaviour, and cases that do not align with the original risk profile.

The issue is not the absence of anti-money laundering checks. The issue is where and how those AML checks are placed.

In this blog, we will discuss the essential AML and KYC strategies for insurance policy issuance, how to implement them efficiently, and how AI and automation can enhance risk detection and identity verification for claims directors.

Important AML Risk Checks in Insurance Policy Issuance Process That Cannot Be Skipped

Every insurance company must run these AML risk checks before a policy is issued:

1. Identity consistency checks across data sources

An AML check should not stop at verifying a document. It must confirm that identity behaves consistently across:

- Government records

- Address history

- Financial linkage

A valid ID does not confirm a valid identity. Most AML verification processes accept documents at face value. Considering long-term risks, it's not safe.

2. Sanctions and PEP screening with contextual validation

Standard online AML checks often flag names. They do not interpret context. A name match is not risk. A pattern is.

Claims teams later face cases where:

- Initial screening passed

- Context was ignored

- Risk surfaced during payout

3. Source of funds alignment at onboarding stage

Premium payments are rarely treated as risk signals. When payment behavior does not align with:

- Declared income

- Policy type

- Geography

It creates silent risk that surfaces later during claims.

4. Duplicate and synthetic identity detection

Most AML ID check systems confirm identity. They do not question uniqueness.

- Synthetic identities pass:

- Clean documents

- Clean watchlists

- Clean records

But fail when:

- Multiple policies connect later

- Claims cluster around linked identities

This is one of the most ignored gaps in AML checks for banks and insurers.

What is an AML Check and How It Works for Insurance

An AML check, or Anti-Money Laundering check, is a regulatory requirement designed to prevent financial crimes such as fraud, money laundering, and terrorism financing.

Just as banks perform AML checks to verify the legitimacy of their clients and transactions, insurance companies must ensure that policyholders are not engaged in illicit activities (any kind of fraud, money laundering, or terrorism financing).

Key Elements of AML Checks in Insurance Include:

- Customer Identification: Collecting personal details and verifying government-issued IDs to ensure the policyholder is legitimate.

- Screening Against Watchlists: Checking applicants against global sanctions lists, politically exposed persons (PEP) databases, and negative media reports.

- Transaction Monitoring: Tracking premium payments and claims for unusual or suspicious activity.

- Risk Assessment: Evaluating each policyholder with risk assessment techniques to identify potential financial crime involvement.

Why AML Checks Fail Even When Systems Are in Place?

Even with AML checks embedded across onboarding, insurers still face risk leakage. The reasons resources drain is because verification remains isolated, static, and disconnected from how identity and behavior evolve after policy issuance.

1. Checks pass, but identities do not hold- Most AML verification processes confirm documents at a single point. They do not validate whether identity remains consistent across time, transactions, or interactions. That gap only becomes visible when a claim is filed.

2. Compliance exists, but decision impact is missing- AML checks are completed, documented, and stored. But underwriting decisions rarely change because of them. When risk scoring does not influence approvals, AML checks become record-keeping instead of risk control.

3. Speed is prioritized over depth in digital onboarding- Online AML checks are designed to reduce friction. Applications move fast, but risk evaluation becomes shallow. The system clears profiles quickly, while hidden inconsistencies remain undetected until later stages.

4. Data remains fragmented- Onboarding, underwriting, and claims operate on different datasets. AML signals captured early do not travel forward. When claims teams reassess identity, they often work without the original verification context.

How to Implement AML Checks During Insurance Policy Issuance

Implementing effective AML checks is essential to protect insurance companies from fraud and financial crime. A well-structured process helps identify high-risk applicants, ensures compliance, and allows claims directors to manage risk efficiently. Below is a checklist for a successful AML implementation:

1. Customer Onboarding Verification

Collect accurate personal information and verify government-issued IDs during onboarding. This foundational step ensures applicants are legitimate and forms the first layer of AML risk checks in the insurance policy issuance process.

2. Screening Against Watchlists

Rigorously screen applicants against global sanctions lists, PEP databases, and negative media sources to identify high-risk individuals. Using automated tools for this step improves accuracy, speed, and consistency across all applications.

3. Risk-Based Assessment

Assign risk scores to each applicant based on location, financial background, and transaction history. High-risk applicants undergo enhanced scrutiny to minimize exposure to fraud.

4. Transaction and Policy Monitoring

Monitor premium payments, claims submissions, and overall policy activity for unusual or suspicious patterns. Real-time monitoring enables early detection of fraud or money laundering attempts, allowing timely intervention.

5. Documentation and Audit Trails

Maintain comprehensive records of onboarding, screenings, risk scores, and monitoring outcomes. Proper documentation provides transparency, ensures audit readiness, and demonstrates compliance with regulatory requirements.

6. Periodic Review and Updates

Regulations and fraud tactics evolve rapidly. Regularly update watchlists, refine risk models, and review AML protocols to ensure the system stays effective and aligned with current compliance standards.

How to Implement AML Checks During Insurance Policy Issuance Without Friction ?

AML checks must work within issuance speed, not against it. The focus should stay on placing verification where it influences decisions, without slowing approvals or creating unnecessary manual intervention.

#1 Make AML checks part of underwriting decisions

An AML check should directly affect whether a policy is approved, priced, or limited. If verification runs separately from underwriting logic, it adds compliance value but does not reduce actual risk exposure.

#2 Introduce layered identity verification early

Relying on a single AML ID check creates gaps. Identity must be validated through multiple signals, including document authenticity, data consistency, and behavioural indicators, so risk is identified before policy issuance.

#3 Connect payment behavior with AML verification

Premium transactions carry early signals of risk. When payment patterns do not align with declared profiles, the AML verification process should trigger reassessment instead of waiting for anomalies during claims.

#4 Keep verification continuous, not one-time

AML checks should extend beyond onboarding. As policy activity changes, risk should be recalculated. This ensures that identity verification remains relevant throughout the lifecycle, not just at entry.

The Importance of Integrating AML Screening into Digital Insurance Onboarding

With the rise of digital insurance platforms, traditional AML and KYC processes have become less effective. Conducting AML checks online is now essential to verify applicants quickly and accurately. Here's how insurers can strengthen digital onboarding with AML screening:

Automated Identity Verification

Using AML ID check tools, insurers can instantly verify government-issued documents and personal details. This reduces manual errors and ensures applicants are legitimate from the start.

Real-Time Watchlist Screening

Integrating automated screening against sanctions lists, PEP databases, and negative media sources allows instant detection of high-risk applicants. This ensures suspicious profiles are flagged immediately for further review.

Seamless Digital Workflow

Embedding AML screening into digital insurance onboarding ensures compliance checks occur without disrupting the applicant experience. Policies can be issued faster while maintaining full regulatory adherence.

Continuous Monitoring and Updates

Digital onboarding systems enable ongoing monitoring of policies and transactions. Coupled with regular updates to watchlists and verification protocols, this approach ensures that AML risk checks in the insurance policy issuance process remain effective over time.

Benefits for Claims Directors

By adopting these strategies, claims directors can focus on high-risk cases, reduce fraud exposure, and improve operational efficiency, making the onboarding process safer and faster.

-1.png?width=1200&height=628&name=hubspot%20blog%20(6)-1.png)

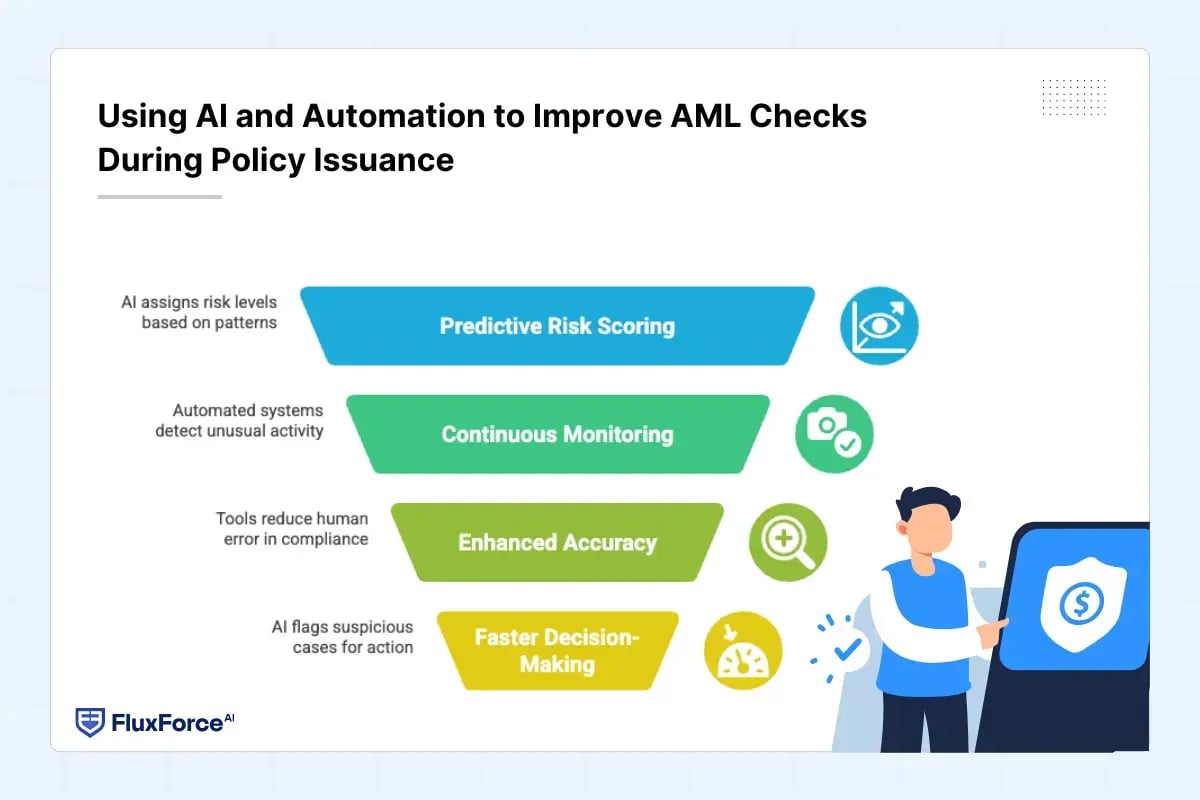

Using AI for AML Checks in Insurance Policy Issuance: Where It Helps

AI is being added to AML checks to improve speed and detection, but its impact depends on how it is applied within the verification process, not just on its presence.

Where AI improves AML verification

AI strengthens AML checks by identifying patterns across large datasets that manual reviews miss. It connects identity signals, transaction behavior, and historical risk to highlight profiles that require closer evaluation.

Where AI creates false confidence

AI-driven AML checks can still approve risky profiles if the underlying data lacks depth. Clean inputs produce clean outputs. When identity verification is weak at source, automation only accelerates flawed decisions.

Where AI needs control

AI should support prioritization, not replace judgment. Risk-prioritized cases still require human review, especially where identity signals conflict. Without that balance, automated AML verification can miss critical inconsistencies.

What Needs to Change in AML and KYC Strategy for Insurance Leaders ?

Most gaps in AML processes are not due to missing checks but to how and where they are applied. Below are some KYC/AML identity verification strategies for insurance claims directors that focus on placement, usage, and connection to actual decisions.

1. Move AML checks closer to underwriting decisions

AML checks often run during onboarding but do not affect whether a policy should be issued or adjusted. When verification directly impacts approval, pricing, or limits, risk gets addressed early instead of shifting to claims teams later.

2. Treat identity verification as something that evolves

A single AML check at onboarding cannot represent a customer across months or years. Customer behavior changes over time. Payment patterns, contact details, and usage signals shift. Verification should adjust alongside these changes instead of staying fixed.

3. Use claims experience to improve onboarding checks

Claims teams often uncover patterns that were not visible during policy issuance. If those insights do not feed back into the AML verification process, the same types of profiles continue to pass initial checks without scrutiny.

4. Share responsibility across teams, not just compliance

AML checks are still seen as a compliance task in many insurers. But underwriting relies on accurate identity. Claims depend on it during payouts. Fraud teams act on it during investigations. Keeping ownership limited creates gaps between these functions.

5. Measure outcomes, not completion

Running AML checks is not the goal. What matters is whether those checks reduce fraud cases, improve claim processing time, and limit repeated verification efforts. Without this shift, the process continues without real impact.

Key KYC/AML & Identity Verification Strategy for Claims Directors

For claims directors, processing claims while protecting against financial crimes is a critical responsibility. Without strong KYC and AML strategies, they risk compliance failures and increased exposure to fraud.

Here are some effective strategies designed to strengthen verification, monitoring, and reporting within daily operations.

- Risk-Based Onboarding: Not all applicants pose the same risk. Implement risk scoring during the AML verification process to identify high-risk clients for enhanced checks.

- Layered Verification: Combine AML checks, government ID verification, and watchlist screening to ensure comprehensive compliance.

- Real-Time Monitoring: Use online AML checks and automated monitoring tools to track policy activity and flag suspicious transactions immediately.

- Regular Review and Updates: Stay updated with evolving regulations, sanctions list, and KYC compliance requirements. For example, KYC compliance requirements for insurance companies in 2025 may require additional identity verification measures or enhanced reporting.

- Training and Awareness: Ensure all staff involved in policy issuance understand AML and KYC requirements. Well-informed claims directors can make better decisions on flagged accounts or high-risk applicants.

- Documentation and Audit Trails: Maintain detailed records for every step of the AML verification process. An AML check is not just compliance—it ensures accountability and regulatory readiness.

Conclusion

AML checks are present across insurance workflows, but their placement continues to limit their effectiveness. Policy issuance remains the stage where risk enters, yet verification often lacks depth and continuity at this point.

Claims teams are then required to reassess identity under pressure, which increases delays and operational effort. This pattern continues because AML checks are treated as steps rather than decision drivers.

A more aligned approach connects verification with underwriting, extends it across the lifecycle, and uses claims insights to refine future checks. This does not require more systems, but clearer integration of existing ones.

When AML verification starts influencing decisions early and remains active throughout the policy lifecycle, insurers reduce both fraud exposure and operational inefficiencies without slowing business.

Share this article