Listen To Our Podcast🎧

Introduction

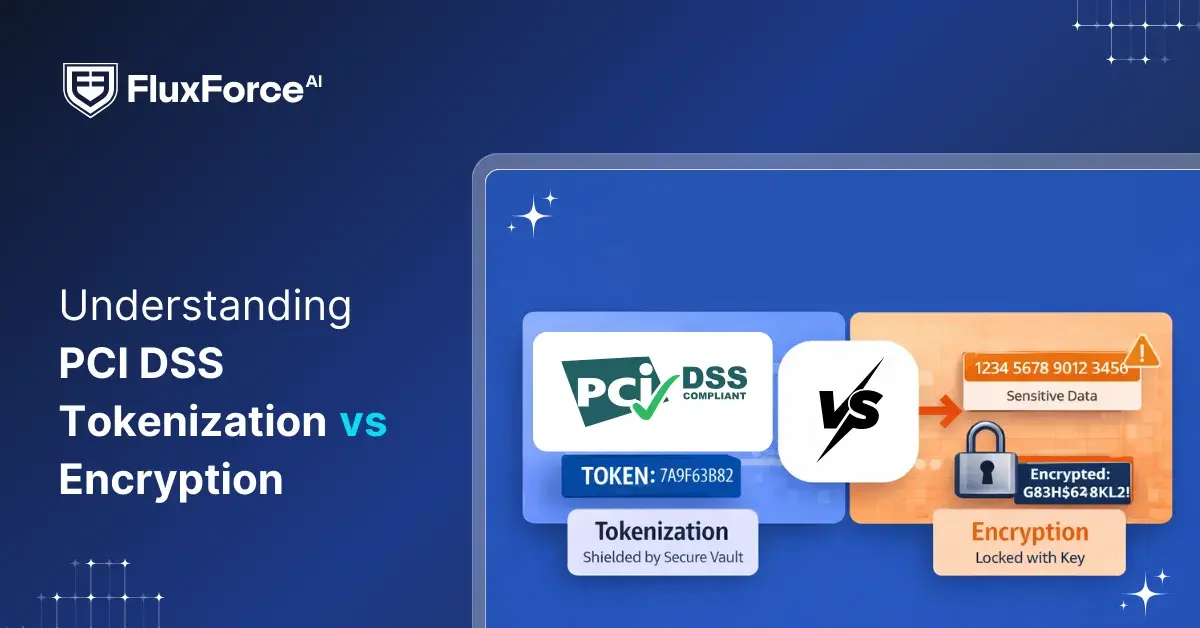

PCI DSS compliance strictly requires organizations to protect cardholder data at all times. Two widely used methods for securing this data are tokenization and encryption.

Encryption converts sensitive information into unreadable code, which can only be decrypted with a specific key. Tokenization, on the other hand, replaces the original data with a unique identifier or token that holds no exploitable value.

While both methods reduce payment risk, they differ in methodology, scope, and compliance impact.

This detailed guide explains how tokenization and encryption operate, highlights their strategic differences, and provides practical guidance on implementing them effectively to maximize credit card data protection and overall PCI DSS compliance.

Key PCI DSS Data Security Methods

For securing customer card details, which many companies have failed to protect over the years, several security techniques are now treated as baseline controls under PCI DSS.

- Data Encryption Across Transit and Storage- Transforms readable card numbers into scrambled ciphertext using mathematical algorithms.

- Tokenization for Payment Processing Systems- Replaces actual card data with randomly generated tokens stored in isolated vaults.

- Restricted Access Controls with Multi-Factor Authentication- Enforces strict permissions, determining which personnel can view cardholder data.

- Continuous Monitoring and Audit Logging- Records all interactions with payment systems for forensic analysis.

- Segmented Network Architecture for Data Isolation- Creates separate zones that isolate cardholder data environments from other corporate infrastructure.

Over the last few years, organizations have relied heavily on encryption and tokenization for protecting payment data, especially within modern payment gateways and distributed transaction systems.

Tokenization vs Encryption in PCI DSS: Strategic Differences

Before comparing the strategic impact, let’s get PCI DSS tokenization and encryption explained in operational terms. Both approaches protect cardholder information, but they control exposure in very different ways.

Tokenization replaces sensitive cardholder data with a unique, non-sensitive token, while the original data is securely stored in a controlled vault inaccessible to business systems.

How Tokenization Secures Cardholder Data

1. Data capture replacement- When a card transaction occurs, sensitive data such as PAN, CVV, and expiration date is sent to a tokenization system. The system immediately replaces it with a token before entering business applications.2. Token generation- The tokenization system creates a random, unique token that mimics the format of the original card data. This token can be used in all internal systems instead of the actual card number.

3. Secure vault storage- The real card information is stored in a highly secured vault. Only authorized tokenization services can access this vault, ensuring business systems never see the actual data.

4. Token usage in operations- Tokens are used for recurring billing, refunds, and reference-based transactions. This approach prevents sensitive card data from being processed or stored in internal applications.

5. Token-to-data mapping- When access to the real card number is needed, the token is mapped back to the original data within the secure vault. This process is tightly controlled and auditable.

6. Data transformation- Encryption changes cardholder data into ciphertext. Attackers who access the data cannot interpret card numbers, CVVs, or expiration dates without the decryption key.

7. Transmission security- Payment data moving between terminals, gateways, and processors is encrypted. Intercepted network traffic cannot expose actual card numbers, keeping cardholder data safe during transit.

8. Encrypted storage- Databases, backups, and logs store only encrypted values. If a hacker gains access to storage media, they cannot retrieve readable payment data.

9. Key control- Access to decryption keys is strictly limited to authorized systems. Regular key rotation and secure storage prevent misuse and accidental exposure.

10. Data retrieval for processing- Systems decrypt card data only when needed for a transaction or reporting. This ensures cardholder information stays protected during all other operations.

Encryption transforms cardholder data into unreadable ciphertext. Only entities with proper cryptographic keys can decrypt the data for processing, while unauthorized access renders it useless.

How Encryption Protects Payment Card Data

PCI DSS Compliance Differences Between Tokenization and Encryption

With their different mechanisms, tokenization and encryption affect PCI DSS compliance in distinct ways. The following table highlights key compliance differences:

Simplify Compliance Complexity

Operational Use of Tokenization and Encryption in Payment Gateways

Modern payment gateways implement encryption and tokenization based on data sensitivity, transaction type, and PCI DSS compliance requirements. Each method protects cardholder information while minimizing system exposure and audit scope.

1. Encryption at Capture

Gateways encrypt cardholder data immediately as it enters the system. Encrypted data travels securely across networks, reducing interception risks. Authorized systems decrypt only when necessary for authorization or processing.

2. Tokenization for Stored Payments

Gateways convert card numbers into tokens for recurring transactions. Merchant systems store only tokens, keeping actual cardholder data out of business systems and reducing PCI DSS scope.

3. Hybrid Use in E-Commerce

Gateways often combine encryption and tokenization. Data is encrypted in transit, authorized by the processor, and then replaced with a token for merchant storage. This strategy protects data at every stage while enabling operational functionality.

4. Mobile Payments

Digital wallets generate tokens to replace card data on devices. Each transaction uses device-specific tokens, ensuring stolen tokens cannot be reused elsewhere. Encryption secures the data during transmission to the gateway.

5. Fraud Analysis and Compliance

Gateways may briefly decrypt data to evaluate fraud patterns. Temporary decryption occurs in isolated, monitored environments. After analysis, data is either re-encrypted or tokenized, minimizing exposure and maintaining PCI DSS compliance.

Considerations for Choosing Between Tokenization and Encryption

Choosing between tokenization and encryption depends on business needs, system architecture, and PCI DSS requirements.

When Companies Should Use Encryption

- Temporary Data Processing Needs: Operations requiring brief access to actual card numbers before permanent deletion. Authorization checks or one-time purchases don't justify tokenization infrastructure.

- Legacy System Constraints: Older platforms built around encrypted storage cannot easily integrate token vaults. Migration costs outweigh encryption's compliance burden for stable environments.

- Cross-Border Transaction Requirements: International payment networks sometimes demand original card data for routing decisions. Encryption allows controlled decryption at specific processing points.

- Backup and Disaster Recovery: Encrypted archives preserve actual cardholder data for system restoration. Token vaults require separate replication strategies that complicate recovery procedures.

- Real-Time Fraud Analysis: Advanced detection engines need plaintext data patterns. Encryption permits temporary decryption within secure processing zones for behavioural screening.

- Recurring Billing Operations: Subscription models storing credentials for future charges. Tokens eliminate risk while maintaining payment automation capabilities.

- Reduced Compliance Scope Goals: Organizations seeking minimal PCI DSS audit footprint. Tokenization removes cardholder data from most business systems entirely.

- Multi-Vendor Payment Ecosystems: Platforms sharing transaction data with partners or third-party processors. Tokens circulate safely without exposing actual credentials.

- Long-Term Data Retention: Customer profiles kept for years face extended breach exposure. Tokens remain worthless even if databases leak decades later.

- Mobile or Cloud-Native Applications: Distributed architectures where encryption key management becomes unwieldy. Centralized token vaults simplify security controls across deployments.

When Companies Should Use Tokenization

Implementing PCI DSS Tokenization and Encryption Together

Organizations often deploy tokenization and encryption together to maximize cardholder data protection while maintaining PCI DSS compliance. Encryption protects sensitive data during transmission and temporary processing, while tokenization removes stored card numbers from business systems.

Using both methods strategically reduces exposure, limits audit scope, and ensures regulatory requirements are consistently met without disrupting operational workflows. Combined implementation allows merchants to support recurring billing, secure online transactions, and digital wallets while keeping sensitive data isolated from internal systems.

Benefits of Combining Tokenization and Encryption

2. Reduced PCI scope- Systems that only handle tokens fall outside full PCI DSS assessment. Encryption ensures sensitive data is protected in systems that must remain in scope.

3. Lower breach risk- If internal systems are compromised, tokens are meaningless, and encrypted data cannot be read without keys. This layered approach mitigates financial and reputational damage.

4. Support for recurring and digital payments- Tokens allow repeated transactions without storing card numbers. Encryption protects sensitive data during processing, ensuring operational continuity with strong security.

5. Simplified compliance reporting- Combining methods streamlines audits. Tokenized systems reduce control requirements, while encrypted systems maintain regulatory coverage, making reporting more efficient and defensible.

6. Operational flexibility- Businesses can safely integrate e-commerce, mobile wallets, and subscription services without exposing sensitive information, keeping both security and functionality intact.

Conclusion

Implementing tokenization and encryption strategically ensures robust protection of cardholder data while maintaining PCI DSS compliance. Tokenization reduces exposure by replacing sensitive information with secure tokens, minimizing audit scope and operational risk.

Encryption safeguards data during transmission and processing, ensuring intercepted or stored information remains unreadable without keys. When combined, these methods provide end-to-end security, support recurring and digital payments, and strengthen regulatory confidence.

Organizations can maintain operational efficiency without compromising safety, reduce the impact of potential breaches, and simplify compliance reporting. Choosing the right approach—or a hybrid deployment—allows businesses to protect payment data effectively while meeting strategic, operational, and regulatory requirements.

Share this article