.webp)

Introduction

The most expensive line item in your fraud prevention budget might not be the tools you have bought. Reducing false positives in transaction monitoring is where the real money is: industry research estimates that 90-95% of alerts generated by traditional systems turn out to be false positives, and each one costs a compliance analyst 5-15 minutes to investigate. Scale that across thousands of daily alerts, and you are looking at millions in wasted analyst hours annually, plus the very real risk of fraud alert fatigue causing genuine threats to be missed.

Reducing false positives in transaction monitoring is where the real money is: industry research estimates that 90-95% of alerts generated by traditional systems turn out to be false positives, and each one costs a compliance analyst 5-15 minutes to investigate.

This guide breaks down exactly what drives false positive volume, how automated transaction monitoring powered by AI changes the equation, and the tactical steps that have helped banks cut their false positive rate fraud detection by 80% without sacrificing detection accuracy.

- Why Transaction Monitoring False Positives Cost More Than You Think

- How Does AI Detect Fraud Differently Than Rule-Based Systems?

- How to Reduce False Positives in AML: Proven Strategies

- AI Fraud Detection Software: Features That Actually Move the Needle

- Sardine vs Unit21: Choosing the Right Transaction Monitoring Software

Onboard Customers in Seconds

Why Transaction Monitoring False Positives Cost More Than You Think

The standard view of the false positive problem focuses on analyst time. That is real, but it is the smaller part of the transaction monitoring cost picture.

When alert volumes are consistently high, compliance teams start triaging by habit rather than evidence. Analysts learn which rules fire most often and discount those alerts subconsciously. That cognitive shortcut is exactly how fraud alert fatigue develops, and it is how genuine money laundering cases slip through after months of suspicious activity generating ignored alerts.

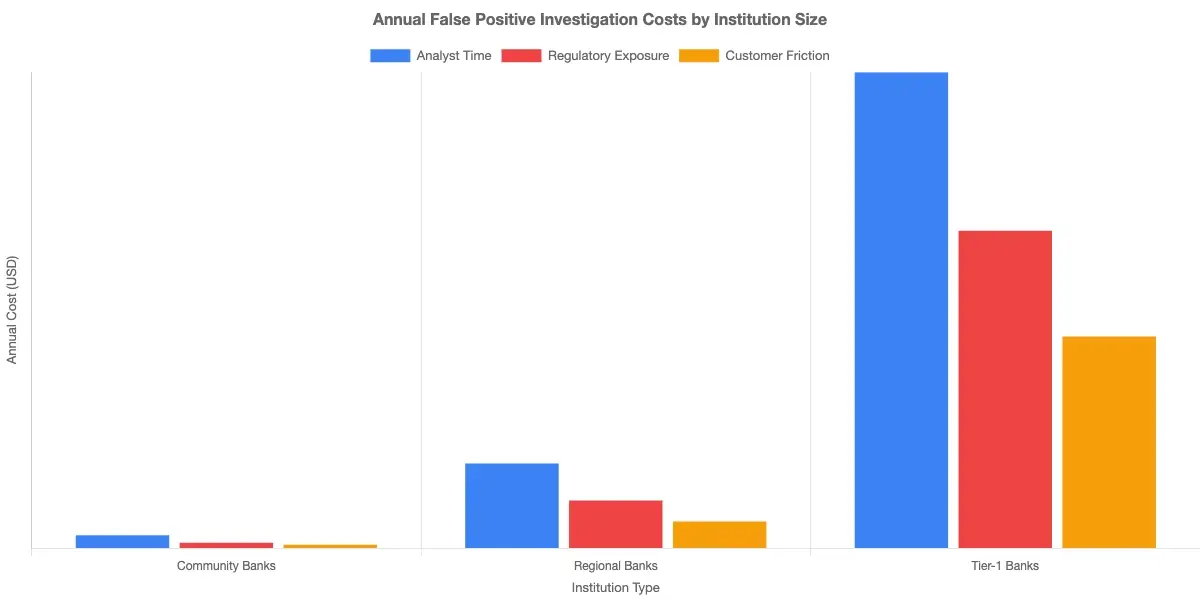

The Hidden Cost of False Positives in Fraud Detection

False positive cost fraud calculations in most compliance teams are narrow: analyst hourly rate times investigation minutes. The actual cost is considerably larger. Consider three components that rarely appear on the balance sheet:

- Regulatory exposure: Regulators do not distinguish between intentional misses and fatigue-driven ones. A bank that files a SAR late because analysts were overwhelmed by noise faces the same penalties as one that deliberately failed to file.

- Customer friction: Legitimate transactions flagged and blocked damage customer trust. Payment fraud prevention tools that block too aggressively push good customers to competitors who do not over-flag.

- Staff turnover: High alert volumes burn out experienced compliance analysts. Replacing a senior AML investigator typically costs 50-200% of their annual salary in recruiting and onboarding.

The FATF Recommendations on transaction monitoring effectiveness consistently note that alert volume without proper risk calibration produces diminishing returns and increasing regulatory scrutiny.

How Fraud Alert Fatigue Erodes Your Compliance Team

Fraud alert fatigue is not a morale problem. It is a measurement problem. When teams are evaluated on alert clearance rates rather than investigation quality, speed replaces thoroughness. Analysts start closing low-scoring alerts without proper documentation, and over time that becomes the default posture for the entire compliance operation.

The honest answer is that most compliance teams do not know their fatigue level until a regulatory exam surfaces investigation quality gaps. By then, the cultural habit is already embedded.

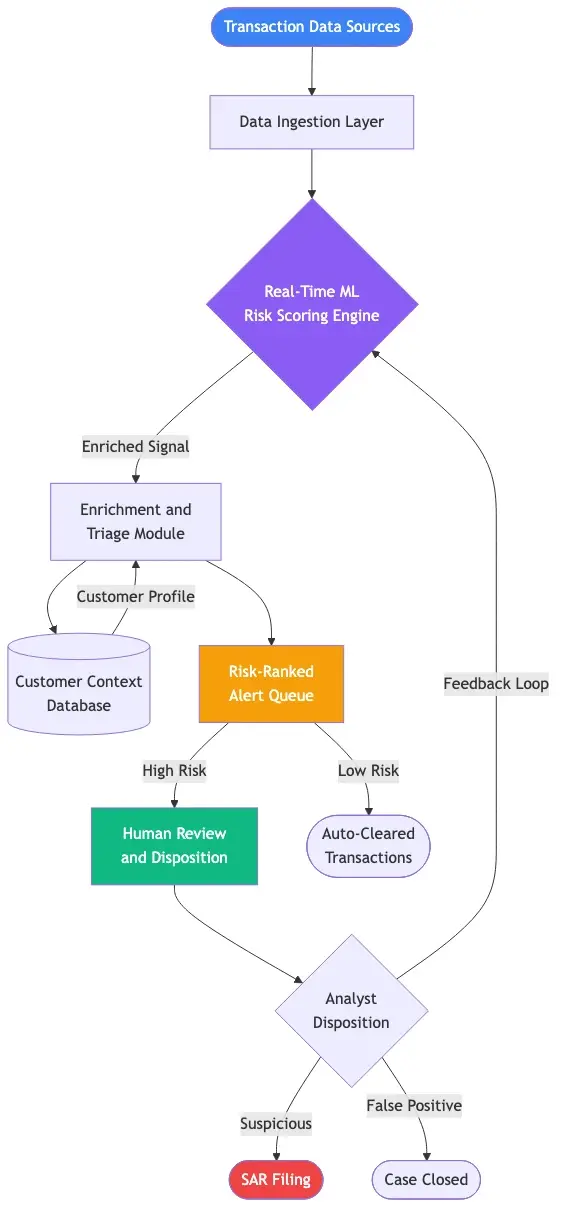

How Does AI Detect Fraud Differently Than Rule-Based Systems?

AI fraud detection does not replace rules, it makes them contextual. A rules-based system asks: "Did this transaction exceed $10,000?" An AI system asks: "Is this transaction unusual for this customer, given their history, peer group, geography, and the time of day?"

That shift from absolute thresholds to relative risk scoring is what drives the 80% reduction in false positives that well-implemented AI systems achieve. The false positive rate fraud detection drops because alerts are calibrated to behavioral context, not just transaction size.

That shift from absolute thresholds to relative risk scoring is what drives the 80% reduction in false positives that well-implemented AI systems achieve.

AI Fraud Detection Explained: From Rules to Risk Scores

AI fraud detection explained simply: instead of evaluating each transaction against a static rule set, the system builds a model of what normal looks like for each customer, merchant category, and channel. Transactions that deviate from that normal get a risk score. Only high-confidence anomalies generate alerts.

A $4,500 wire transfer from a business account that routinely moves $3,000-$6,000 gets a low risk score. The same amount from a personal savings account that has never sent a wire before gets a high score. Same dollar amount, entirely different behavioral context. This is ai fraud detection explained at its most practical: contextual scoring that eliminates noise created by one-size-fits-all thresholds.

Machine Learning Fraud Detection Models in Practice

Machine learning fraud detection typically uses a combination of supervised and unsupervised models. Supervised models learn from labeled historical data, confirmed fraud versus confirmed legitimate transactions. Unsupervised models identify statistical anomalies without needing labels, catching novel attack patterns that have not appeared in training data yet.

The combination matters because supervised models alone struggle with new fraud typologies, while unsupervised models alone generate too many false positives. Together, they balance sensitivity and specificity in a way no static rule set can. For a detailed look at how this applies to card fraud specifically, see our guide on AI-powered fraud detection strategy for risk heads.

Real Time Fraud Detection: Processing Millions of Signals Per Second

Real time fraud detection is only valuable if the latency is low enough to matter. For card transactions, you have 200-300 milliseconds to approve or decline before the customer experience degrades. Real time fraud detection banks deploy uses inference engines that score transactions in under 50ms, pulling enriched customer context from in-memory data stores rather than live database queries.

This speed constraint is why production AI models for real-time scoring tend to be simpler than research models. A gradient boosting model with 50-100 features running in production is more operationally reliable than a deep neural network requiring GPU inference per transaction.

How to Reduce False Positives in AML: Proven Strategies

This is where theory meets practice. Reducing false positives in transaction monitoring does not happen from buying a new platform, it happens from systematic calibration work that most teams skip because it is unglamorous.

Behavioral Baselines and Customer Segmentation

The single most effective way to reduce false positives in transaction monitoring is to stop evaluating all customers against the same risk profile. A wholesale business moving $2 million daily should not be scored against the same thresholds as a retail savings account.

Proper customer segmentation groups accounts by industry, transaction velocity, typical counterparties, and geographic footprint. Thresholds are set per segment, not globally. This step alone can cut false positive volume by 40-50% before any ML model is deployed. To see how this connects to false positives fraud detection in digital lending specifically, the AML screening strategy for payments risk officers covers segmentation approaches in detail.

This step alone can cut false positive volume by 40-50% before any ML model is deployed.

Dynamic Thresholds vs. Static Rule Sets

Static rules are easy to audit and easy to game. Dynamic thresholds, set by ML models that recalibrate weekly or monthly based on observed behavior, are harder to audit but considerably more accurate. How to reduce false positives in AML at scale means accepting that your thresholds need to evolve as transaction patterns change.

The practical challenge: regulators want to see documented rationale for alert thresholds. Dynamic ML thresholds require explainability tooling such as SHAP values, feature importance rankings, and audit logs of model updates, so that when an examiner asks why an alert fired (or did not fire), your team has a clear answer ready.

Feedback Loops That Actually Get Used

Most transaction monitoring software has a feedback mechanism. Most compliance teams do not use it properly. When an analyst closes an alert as a false positive, that disposition should feed back into the scoring model to adjust future behavior. In practice, teams close alerts in a legacy case management system that is not connected to the scoring model at all.

The fix is integration, not new features. Connect your case management workflow to your scoring model so analyst dispositions directly tune alert thresholds. Teams that implement this feedback loop typically see their false positive rate fraud detection improve by 15-25% within 90 days, without any model changes.

AI Fraud Detection Software: Features That Actually Move the Needle

Buying ai fraud detection software is not the same as solving the false positive problem. The tools matter less than the configuration, and the configuration requires people who understand both the fraud patterns and the scoring models driving alerts.

That said, platform choice does constrain what is possible. The transaction monitoring cost of a poorly chosen platform includes not just licensing fees but the ongoing engineering effort required to work around its limitations.

AI Fraud Detection in Banking: What Good Looks Like

AI fraud detection in banking requires a platform that handles regulatory constraints alongside technical requirements. Three things to evaluate before signing a contract:

- Explainability by default: Every alert should surface the top 3-5 features that drove the risk score. Regulators require this. So do analysts who need to decide in 30 seconds whether to escalate.

- Real-time enrichment: The scoring model should pull device fingerprint, IP reputation, velocity data, and counterparty history in the same API call, not as sequential lookups that add latency.

- Customer context persistence: The model needs 12-24 months of transaction history to build a reliable behavioral baseline. Short lookback windows produce more false positives, not fewer.

Real-Time Fraud Detection Banks Rely On

The most effective real time fraud detection banks deploy combines pre-computed customer profiles (updated in near-real-time) with in-flight transaction scoring. This hybrid approach keeps latency under 100ms while still using deep behavioral history to inform each decision.

Synthetic identity fraud is a useful test of any platform's real-time capabilities. Synthetic identities look clean at the account level, normal transaction histories, on-time payments, steadily building credit. The fraud signal only emerges in behavioral patterns across accounts: shared device fingerprints, overlapping addresses, coordinated account opening timing. Detecting this requires graph analytics running in real time, not overnight batch jobs. For more on this specific threat, see our deep-dive on detecting synthetic identity fraud in real-time.

Transaction Monitoring System for Banks: Key Integration Points

A transaction monitoring system for banks that runs in isolation is inherently limited. The highest-performing implementations integrate with four systems:

- Core banking system: For account status, relationship history, and balance trends

- KYC/CDD platform: For customer risk ratings that directly inform monitoring thresholds

- Case management system: For feedback loops and SAR filing efficiency

- Sanctions screening: To avoid duplicate alert generation for the same underlying event

The sanctions screening automation strategy for CISOs covers how integrated screening reduces redundant alerts across compliance functions.

Sardine vs Unit21: Choosing the Right Transaction Monitoring Software

The sardine vs unit21 comparison comes up constantly in fintech and challenger bank procurement discussions. Both are credible platforms built by strong teams, but they solve different parts of the false positive problem.

Sardine: Strengths for High-Volume Payment Fraud Prevention

Sardine is strongest in payment fraud prevention at the transactional layer. Its device intelligence and behavioral biometrics capabilities detect account takeover attempts and synthetic identity fraud signals that most rule-based systems miss entirely. For organizations whose primary problem is real-time payment fraud on ACH, card, or crypto rails, Sardine is worth serious evaluation.

The limitation is that Sardine's AML and compliance monitoring capabilities are less developed than its fraud detection features. If compliance monitoring is the primary use case rather than payment fraud, additional tooling will likely be needed alongside it.

Unit21: Case Management and Investigation Workflow

Unit21's strength is in the alert management and investigation workflow layer. Its no-code rule builder lets compliance teams create and tune detection logic without engineering support. The audit trail and SAR filing workflow are well-designed for the regulatory environment most financial institutions operate in.

The honest limitation: Unit21's machine learning capabilities are less sophisticated than platforms built natively on behavioral AI. If cutting-edge machine learning fraud detection is the priority rather than better rule management, the scoring models may not perform as well as purpose-built alternatives.

When Neither Tool Fits

For large tier-1 banks, neither the sardine vs unit21 options may be the right transaction monitoring software choice. The complexity of a multi-product, multi-jurisdiction bank with legacy core banking infrastructure often requires a more customizable platform, combined with a purpose-built ML scoring layer on top.

The real question is not which vendor wins a feature comparison. It is which solution your team can implement, tune, and maintain in a regulated environment. A sophisticated platform that a team cannot configure correctly will produce more false positives than a simpler one they understand well.

Automated Transaction Monitoring: Cutting Alert Volume Without Cutting Accuracy

Automated transaction monitoring has a complicated reputation in compliance circles because early implementations promised automation and delivered more noise, not less. The problem was not automation, it was automating the wrong things.

The right automation targets low-value, high-volume work: alert triage, data enrichment, and preliminary investigation gathering. When an alert fires, an automated workflow should immediately pull customer risk rating, prior SAR filings, adverse media hits, counterparty information, and recent transaction history. That pre-population saves 8-12 minutes per alert, which across 500 daily alerts translates to 70-100 analyst hours recovered every single day.

Synthetic Identity Fraud and Why Automation Matters

Synthetic identity fraud illustrates why manual processes cannot keep pace with modern fraud patterns. According to McKinsey research on financial crime and fraud, synthetic identity fraud costs U.S. lenders an estimated $6 billion annually. These are not simple patterns a trained analyst can spot in a transaction history, they require graph analytics comparing data points across thousands of accounts simultaneously. That is a computation problem that automation solves, freeing analyst judgment for cases that actually need it.

Automation does not replace the analyst. It handles data aggregation and pattern recognition so analysts can apply their expertise where it matters.

Payment Fraud Prevention at Scale

Payment fraud prevention at scale requires rethinking what prevention means. Traditional models try to block fraud at the transaction level. Modern approaches layer account-level behavioral monitoring, network-level relationship analysis, and device-level fingerprinting to build defense in depth.

NIST's Digital Identity Guidelines (SP 800-63) provide the technical framework many banks use to standardize how behavioral signals feed into risk scoring architectures. If your team is rebuilding your scoring architecture from scratch, it is worth reviewing before committing to an implementation approach.

- The standard view of the false positive problem focuses on analyst time.

- AI fraud detection does not replace rules, it makes them contextual.

- This is where theory meets practice.

- Buying ai fraud detection software is not the same as solving the false positive problem.

- The sardine vs unit21 comparison comes up constantly in fintech and challenger bank procurement discussions.

Onboard Customers in Seconds

Conclusion

Reducing false positives in transaction monitoring by 80% is achievable, but it requires more than a procurement decision. The pattern across institutions that hit this target is consistent: they segment customers properly before setting thresholds, they connect analyst feedback loops to their scoring models, and they invest in explainability tooling that makes ML-driven alerts defensible to regulators.

Automated transaction monitoring and ai fraud detection are force multipliers for teams that have already done the foundational calibration work. Institutions that skip that work and buy a new platform first typically see their false positive volume shift, not shrink.

If your team is evaluating where to start, the agentic AI approach to cutting false positives covers how purpose-built fraud agents operate differently from traditional automation. The goal is not zero alerts, it is ensuring every alert that reaches an analyst is worth their time.

Share this article