.webp)

Introduction

Sanctions screening automation is no longer optional for financial institutions that want to stay compliant without drowning in manual alerts. For banks, fintechs, and insurers running lean compliance teams, the sheer volume of watchlist matches, false positives, and regulatory deadlines makes purely manual review unsustainable. This post breaks down how modern sanctions screening automation works, what to look for in aml compliance software, and how your team can build a defensible program without adding headcount.

- What Is Sanctions Screening Automation and Why Does It Matter?

- The Hidden Costs of Manual AML Compliance Reviews

- How Sanctions Screening Automation Works in Practice

- AML Compliance Software: Core Features That Matter

- SAR Filing Efficiency: How Automation Reduces Reporting Delays

Onboard Customers in Seconds

What Is Sanctions Screening Automation and Why Does It Matter?

Sanctions screening automation is the use of software to automatically match transactions, customers, and counterparties against government and regulatory watchlists in real time, without requiring an analyst to review each alert manually.

Watchlists include OFAC's SDN list, the EU Consolidated Financial Sanctions List, HM Treasury's UK Sanctions List, and dozens of PEP (Politically Exposed Persons) databases. Manual screening against all of these lists across thousands of daily events is not feasible at scale.

Automation matters because regulators do not grade on a curve. FinCEN, OFAC, and the FCA have issued substantial penalties to institutions whose screening processes were slow, inconsistent, or poorly documented. In 2023, OFAC collected over $1.5 billion in civil penalties, with a significant share tied to screening failures. Automation closes the gap between transaction volume and compliance capacity.

In 2023, OFAC collected over $1.5 billion in civil penalties, with a significant share tied to screening failures.

How Does Automated Screening Differ from Manual Review?

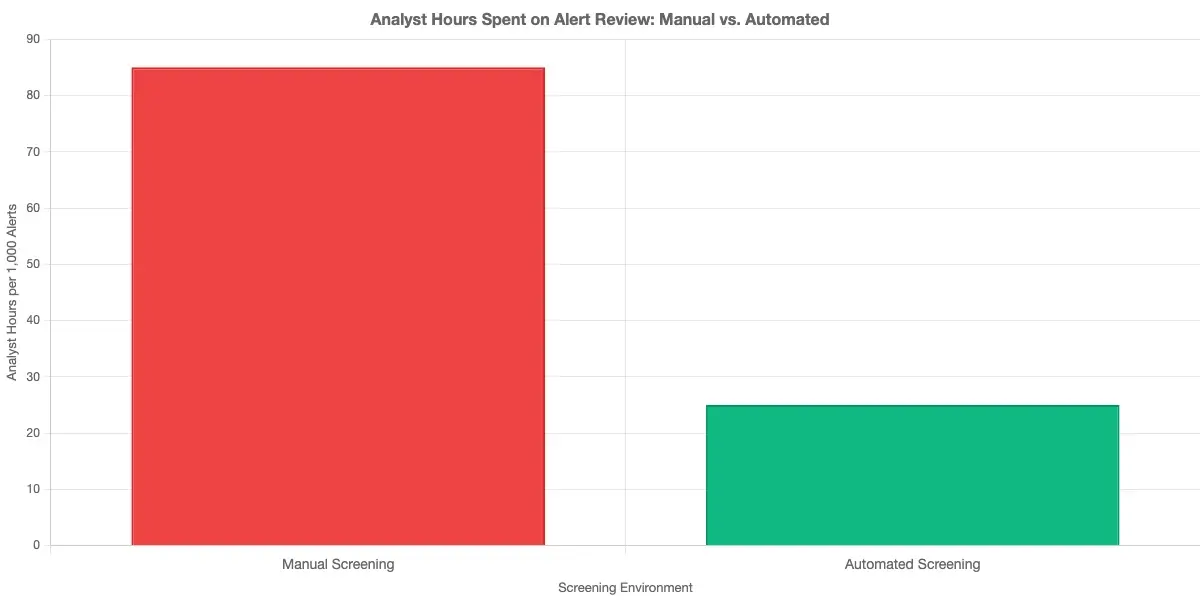

Manual review means an analyst receives a flagged alert, cross-references it against watchlists, assesses risk, and makes a disposition decision. That process takes anywhere from 10 minutes to several hours per alert, and it scales linearly with volume.

Automated systems match entities using fuzzy logic, phonetic algorithms, and AI-based name matching to reduce false positives before they reach a human reviewer. The system assigns a risk score to each potential match, with high-confidence true matches routed for immediate action and low-probability alerts filtered or auto-cleared. In production deployments, this cuts analyst workload by 60-80%.

Key Regulations Driving Sanctions Screening Adoption

AML compliance sits at the intersection of multiple overlapping regulatory frameworks: the Bank Secrecy Act (BSA), the USA PATRIOT Act, OFAC regulations, and, for EU-based institutions, the 6th Anti-Money Laundering Directive (6AMLD). The EU AI Act for financial services, which entered enforcement phases in 2025, also applies to AI-powered screening tools, requiring explainability and audit logging for decisions that affect customers.

The Hidden Costs of Manual AML Compliance Reviews

Most institutions underestimate what manual aml compliance actually costs. The obvious line item is analyst headcount. The less obvious costs are harder to see until something goes wrong.

False positives are the primary drain. Industry data suggests 95-98% of AML alerts in rule-based screening systems are false positives. Each one requires human review time. At scale, a team of five analysts might spend their entire week clearing alerts that turn out to be legitimate transactions, with only a handful of hours left for genuine risk assessment work.

False Positives and Analyst Burnout

The false positive problem is more serious than throughput alone. Analysts who spend eight hours a day reviewing noise become desensitized. Alert fatigue is a documented phenomenon in compliance operations, and it correlates directly with missed true positives. When everything looks like a false alarm, the genuine match blends in.

Automation changes the nature of the work. Analysts shift from rote alert clearing to judgment-based review of high-confidence matches, which requires human expertise and cannot be automated away.

The Compliance Bottleneck in Growing Institutions

For fintechs and community banks, the compliance bottleneck is acute. A fintech processing $50M in daily payment volume with a two-person compliance team faces a structural problem: the team cannot keep up with screening volume as the business grows, but hiring is expensive and qualified AML analysts are scarce.

A fintech processing $50M in daily payment volume with a two-person compliance team faces a structural problem: the team cannot keep up with screening volume as the business grows, but hiring is expensive and qualified AML analysts are scarce.

Sanctions screening automation allows the compliance function to scale with transaction volume without a proportional increase in headcount. That is the core economic argument, and it explains why adoption is accelerating across aml compliance fintech deployments worldwide.

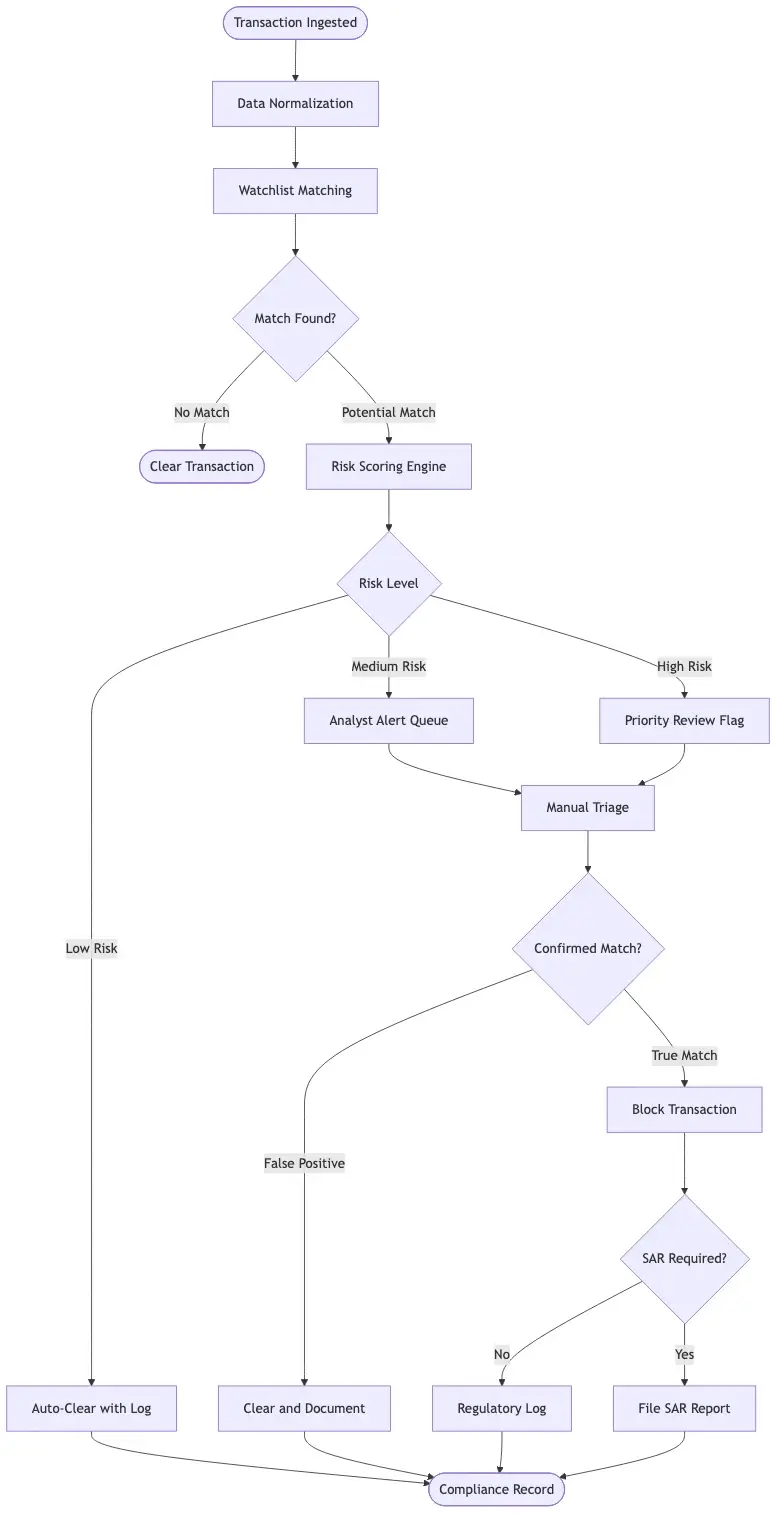

How Sanctions Screening Automation Works in Practice

Understanding the mechanics helps when evaluating vendors and building your internal process. Sanctions screening automation follows a consistent architecture, though implementations vary in sophistication.

The process starts at the point of customer onboarding or transaction initiation. The system captures entity data (name, date of birth, nationality, address, account numbers) and sends it to a matching engine that compares the input against one or more watchlists using:

- Exact matching: direct string comparison for account numbers, identification numbers, and unique identifiers

- Fuzzy matching: Levenshtein distance and similar algorithms to catch typos and transliteration variants

- Phonetic matching: Soundex, Metaphone, and Double Metaphone for name variants across languages

- AI-based entity resolution: machine learning models trained on historical match/no-match decisions

The output is a scored list of potential matches. Compliance teams set thresholds: matches above a certain score go to analyst review, matches below are auto-cleared with a documented rationale.

Real-Time Watchlist Matching and Fuzzy Logic

Real-time screening is the standard for transaction monitoring, but match quality varies significantly between vendors. Fuzzy logic handles the most common screening challenge: sanctioned entities do not always appear in databases under the name they use in a given transaction. Transliteration from Arabic, Cyrillic, or Chinese scripts produces dozens of legitimate name variants, and a system relying on exact matching will miss many of them.

The best anti money laundering technology 2026 implementations use machine learning to continuously improve match accuracy based on analyst feedback. When an analyst clears a false positive, that signal trains the model to recognize similar patterns, reducing future noise in the alert queue.

Risk Scoring and Alert Prioritization

Risk scoring is where sanctions screening automation creates real operational leverage. Instead of a binary match/no-match result, the system assigns a probability score and contextualizes it with customer risk factors: jurisdiction, transaction type, counterparty history, and product type.

High-risk alerts go to senior analysts. Low-risk auto-cleared events are logged with full audit trails. This tiered approach means the 2% of alerts that genuinely need human attention actually get it, which is exactly what regulators expect to see in an effective sanctions screening and AML compliance program.

AML Compliance Software: Core Features That Matter

Not all aml compliance software is built the same. When evaluating platforms, these are the capabilities that separate adequate from defensible.

Watchlist Coverage and Update Frequency

A screening tool is only as good as its watchlists. Coverage must include OFAC's SDN and Non-SDN lists, the EU Consolidated List, the UN Security Council List, HM Treasury, and relevant domestic lists. PEP databases and adverse media feeds add depth for kyc automation workflows.

Update frequency matters as much as coverage. OFAC can add or remove entries with little advance notice. A system that refreshes watchlists daily creates a window of exposure. The best platforms update in near real-time, within minutes of regulatory changes.

Audit Trails and Regulatory Reporting

Regulators will ask to see your screening logs. They want to know which lists were checked, when, with what result, and who made the disposition decision. AML compliance software must generate complete, tamper-evident audit trails for every screening event.

This is also where integration with your CTR filing rules and SAR workflows matters. When a screening match triggers a review that results in a suspicious activity report, the system should connect those events in a single case record. Fragmented workflows, where screening lives in one system and SAR filing lives in another, create documentation gaps that examiners find.

SAR Filing Efficiency: How Automation Reduces Reporting Delays

SAR filing efficiency is one of the most measurable benefits of compliance automation. The Bank Secrecy Act requires suspicious activity reports to be filed within 30 calendar days of detecting a suspicious transaction (or 60 days if additional investigation is needed). Missing that deadline is a BSA violation, full stop.

Manual SAR processes are slow because they involve multiple handoffs. A screening alert triggers an analyst review, which may escalate to a compliance officer, which requires gathering transaction records, documenting the suspicious pattern, drafting the SAR narrative, and submitting through FinCEN's BSA E-Filing System. Each step adds time, and coordination across teams adds more.

SAR Filing Best Practices for Compliance Teams

Automation compresses this timeline by pre-populating SAR fields from case management data. When a transaction is flagged and investigated, the system has already captured entity information, transaction details, and the analyst's investigation notes. The SAR draft generates automatically, requiring only narrative review and supervisor sign-off before submission.

This is not just faster. It is more accurate. Pre-populated forms pulled from structured data contain fewer transcription errors than manually drafted filings, reducing the risk of deficient SARs that FinCEN may return for correction. For a detailed look at how sar filing best practices integrate with payment AML workflows, the AML Screening in Digital Lending analysis covers the payment risk perspective in depth.

SAR Filing Requirements 2026: What's Changing

FinCEN has signaled continued focus on SAR quality over quantity. Rulemaking under the Anti-Money Laundering Act of 2020 emphasizes that institutions should file high-quality, actionable SARs rather than defensive filings of low-confidence alerts. Automated case management systems support this by providing analysts with full transaction context to write specific, useful narratives rather than generic descriptions.

The practical implication for sar filing requirements 2026 is clear: automation that improves narrative quality will be more defensible than volume-based manual filing. The suspicious activity report guide published by FinCEN remains the authoritative reference for formatting and content requirements, and institutions investing in AI-assisted narrative tools are positioning themselves well for increased examiner scrutiny.

KYC Automation in 2026: Meeting CDD and EDD Requirements

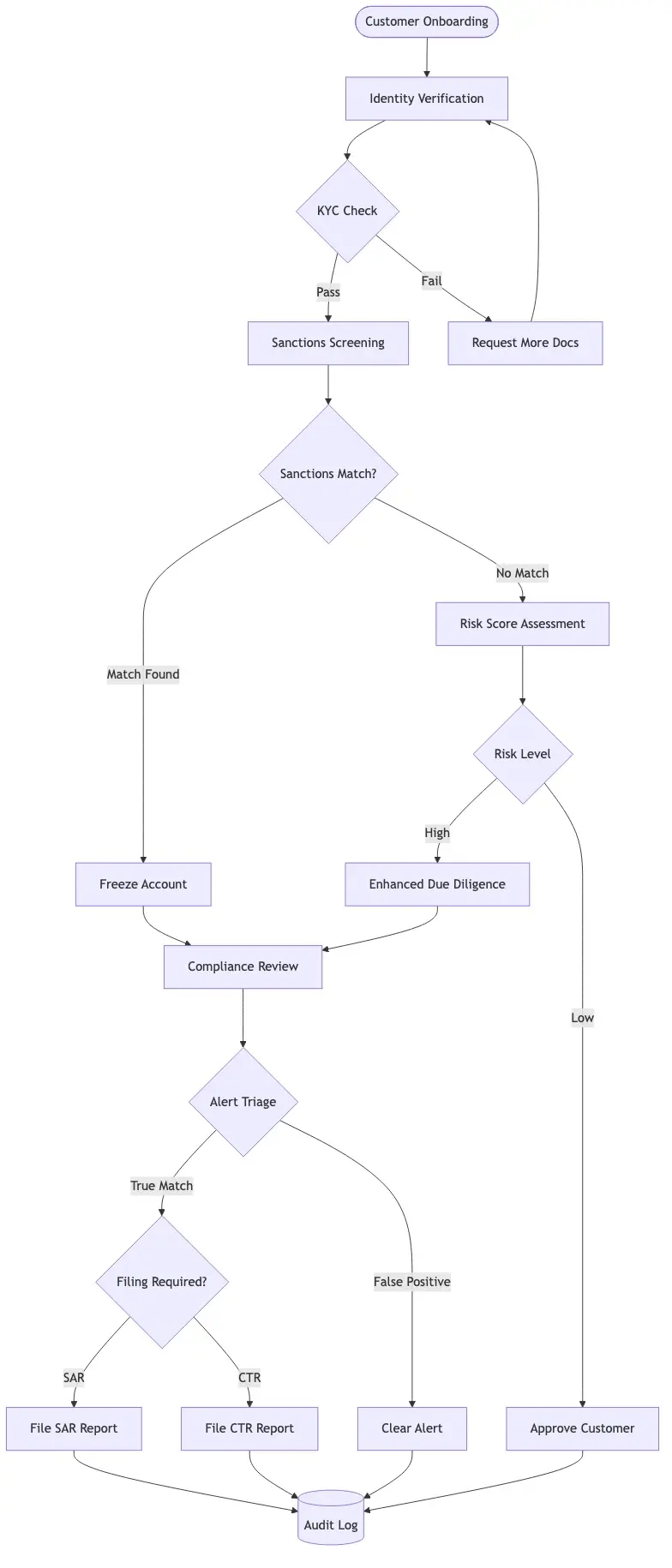

KYC automation 2026 is where most institutions are investing right now. The Customer Due Diligence (CDD) Final Rule under the BSA requires covered financial institutions to collect and verify beneficial ownership information for legal entity customers, maintain updated customer risk profiles, and conduct ongoing monitoring.

Manual KYC is inherently point-in-time. You verify a customer at onboarding, file the records, and may not revisit them for years. Automated KYC creates continuous monitoring that refreshes customer profiles against adverse media, PEP databases, and sanctions lists on a scheduled basis, flagging material changes for analyst review.

KYC/CDD Requirements for Banks: What Examiners Check

KYC CDD requirements banks are examined against the four pillars of the CDD Rule: customer identification, beneficial ownership, understanding the nature and purpose of the customer relationship, and ongoing monitoring. Examiners focus heavily on the fourth pillar because it is where manual programs most often fall short.

Automated ongoing monitoring runs in the background without requiring analyst intervention unless a change is detected. When a customer's name appears on a newly added watchlist entry, or when adverse media coverage emerges, the system creates a review task with the relevant context already attached. For compliance teams managing AML checks across product lines, the AML Risk Checks in Policy Issuance post covers how these kyc cdd requirements banks face apply in insurance and lending contexts as well.

Enhanced Due Diligence Guide for High-Risk Customers

Enhanced due diligence (EDD) is required for customers and relationships that pose elevated risk: PEPs, customers in high-risk jurisdictions, businesses with complex ownership structures, and relationships with unusual transaction patterns. The FATF guidance on customer due diligence and enhanced measures identifies the specific factors that trigger EDD and the depth of review required.

Automation helps by scoring customer risk at onboarding and triggering EDD workflows automatically when thresholds are met. This prevents the inconsistency that comes from analyst discretion determining which customers receive enhanced review. Documented, consistent triggers are exactly what examiners want to see in your enhanced due diligence guide and program documentation.

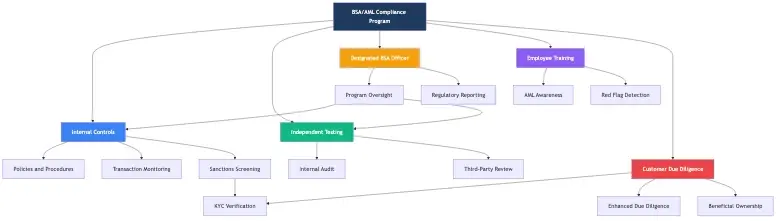

Building Your BSA/AML Compliance Checklist

A practical bsa aml compliance checklist covers five operational areas. This is a working reference for compliance officers assessing their current program, not an exhaustive regulatory manual.

1. Written AML Program Your written program must address all five BSA pillars: internal controls, independent testing, a designated BSA officer, training, and customer due diligence. Update it when your business model changes, not just when regulations do.

2. Risk Assessment Your aml risk assessment guide should document risk across products, services, customers, and geographies. Screening thresholds should map to your risk assessment findings. If your screening logic is not tied to your documented risk profile, that is a gap examiners will find.

3. Customer Identification Program (CIP) CIP procedures must include the minimum information required under 31 CFR 1020.220 and your process for verifying that information. Automation can match applicant data against authoritative identity databases in seconds, replacing manual document review for standard cases.

4. Ongoing Monitoring and Screening Document the lists you screen against, your update frequency, your match threshold logic, and your escalation procedures. This is where sanctions screening automation delivers the most direct and measurable operational value.

5. SAR and CTR Filing Document your SAR decision process, your CTR filing rules for cash transactions exceeding $10,000, and your exemption documentation procedures. Examiners will review whether your SAR narratives are specific and actionable.

BSA/AML Compliance for Community Banks

BSA/AML compliance for community banks presents a specific challenge: small institutions face the same regulatory requirements as their larger peers but often lack equivalent technology budgets. Cloud-based AML compliance software has materially changed this equation. Institutions with under $1 billion in assets can now access enterprise-grade screening through SaaS platforms with pre-built core banking integrations and per-transaction pricing, without multi-year enterprise contracts or dedicated IT infrastructure.

Institutions with under $1 billion in assets can now access enterprise-grade screening through SaaS platforms with pre-built core banking integrations and per-transaction pricing, without multi-year enterprise contracts or dedicated IT infrastructure.

The honest answer on cost is that modern aml compliance fintech vendors have compressed what once required a six-figure annual contract into subscription models that scale with transaction volume. This changes the build-versus-buy calculus for community banks considerably.

AML Risk Assessment Guide: Ongoing Monitoring

Your risk assessment is a living document. Update it at least annually, and more frequently when you add new products, enter new markets, or observe shifts in your customer risk profile. Automated monitoring tools can feed data directly into your risk assessment process, flagging emerging patterns based on real transaction activity rather than waiting for your next annual review cycle. That kind of continuous feedback loop is what separates a program that passes examination from one that merely documents compliance.

Anti-Money Laundering Technology for Fintechs and Small Teams

Anti money laundering technology now applies to money services businesses of all sizes, including digital payment platforms, lending apps, and crypto exchanges. A 10-person fintech processing $100M in annual payment volume faces the same core BSA requirements as a regional bank with a full compliance department.

Anti-money laundering technology has matured enough that fintechs can deploy credible, examiner-ready compliance programs without dedicated compliance engineering teams. The key is choosing platforms with pre-built regulatory logic rather than building screening rules from scratch, which takes months and introduces significant model risk.

Fintech BSA/AML for Small Teams: Where to Start

Start with your product. What transactions does your platform process? Who are your customers? What jurisdictions do you serve? Your screening configuration should map directly to those answers.

For a fintech bsa aml small team, the math is straightforward: automation is the only realistic way a two-person compliance function covers the alert volume of a growing payments business. Start with a single integrated platform covering customer screening, transaction monitoring, and SAR case management. Fragmented tools create fragmented audit trails, and examiners notice gaps. The How Agentic AI Fraud Agents Cut False Positives by 80% analysis is a useful reference for how AI-driven alert management specifically benefits smaller compliance operations managing high transaction volumes.

EU AI Act Financial Services Considerations

The eu ai act financial services provisions that entered enforcement in 2025 classify AI-based AML screening as a high-risk application. This means your AI screening tools must meet requirements for transparency, explainability, human oversight, and bias testing. Vendors operating in EU markets should provide documentation of model validation, training data provenance, and model drift monitoring.

This is not a reason to avoid AI-based screening. It is a reason to ask vendors the right questions and document your oversight process. Regulators on both sides of the Atlantic are moving toward requiring explainable AI in compliance decisions, and the institutions that build their programs on auditable, documented AI tools now will spend far less time defending them during examination.

- Sanctions screening automation is the use of software to automatically match transactions, customers, and counterparties against government and regulatory watchlists in real time, without requiring an analyst to review each alert manually.

- Most institutions underestimate what manual aml compliance actually costs.

- Understanding the mechanics helps when evaluating vendors and building your internal process.

- Not all aml compliance software is built the same.

- SAR filing efficiency is one of the most measurable benefits of compliance automation.

Onboard Customers in Seconds

Conclusion

Sanctions screening automation is the operational foundation of a modern AML compliance program. Whether you are managing a community bank's bsa aml compliance checklist, running a fintech bsa aml small team, or scaling enterprise kyc automation across product lines, the core principle holds: automation does not replace compliance judgment, it directs that judgment where it matters most.

The institutions that navigate 2026 and beyond without regulatory penalties will be those that match transaction volume with screening capacity, file accurate and timely SARs, and maintain audit trails that hold up under examination. Manual review cannot reliably deliver all three at scale.

If you are evaluating aml compliance software or looking to modernize your current process, start with your risk assessment. Map your screening gaps to your documented risk profile, then build the technology around those gaps. Risk first, technology second: that is the sequence regulators expect to see. For a broader view of how AI-powered compliance automation fits within your security architecture, the Manual Compliance vs. AI Automation analysis covers the tradeoffs in depth.

Share this article