.webp)

Introduction

CTR filing rules automation is no longer optional for financial institutions facing growing transaction volumes and shrinking compliance budgets. Every day, banks, credit unions, and fintechs process thousands of cash transactions that may trigger a Currency Transaction Report (CTR) obligation under the Bank Secrecy Act. Get the process wrong, and FinCEN penalties can reach $25,000 per violation per day. Get it right manually, and your compliance team burns hours on data entry that software handles in seconds.

Get the process wrong, and FinCEN penalties can reach $25,000 per violation per day.

This guide covers everything compliance officers and AML teams need: the exact thresholds, filing deadlines, exemption rules, and how modern aml compliance software is replacing manual CTR workflows in 2026.

- What Is a Currency Transaction Report and When Must You File?

- CTR Filing Rules Under the Bank Secrecy Act

- How CTR Filing Rules Automation Reduces Compliance Risk

- AML Compliance Software and Anti-Money Laundering Technology 2026

- SAR Filing Efficiency: Connecting CTRs to Suspicious Activity Reports

Onboard Customers in Seconds

What Is a Currency Transaction Report and When Must You File?

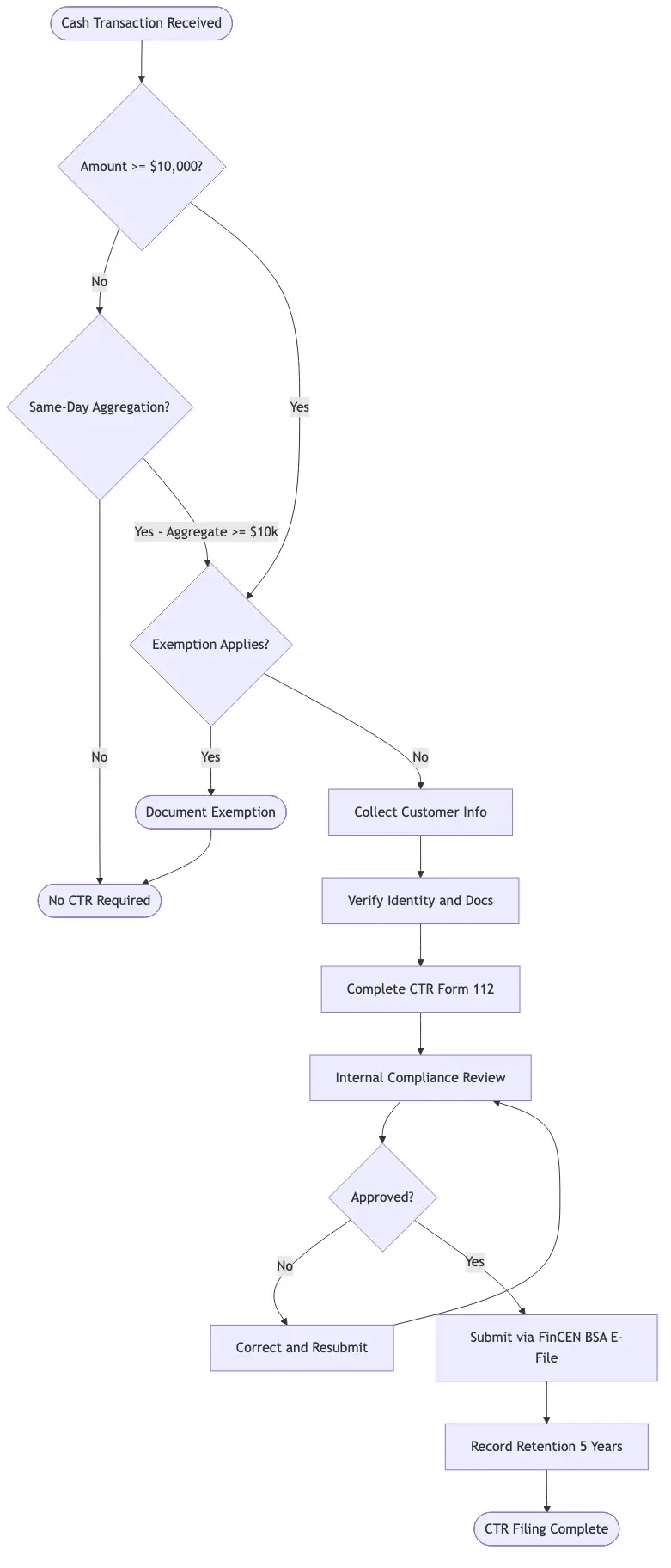

A Currency Transaction Report is a mandatory disclosure filed with FinCEN whenever a customer conducts a cash transaction exceeding $10,000 in a single business day. This applies to banks, credit unions, money services businesses, casinos, and certain non-bank financial institutions under the Bank Secrecy Act, enacted in 1970.

The CTR captures who made the transaction, the account details, and the exact cash amount. Filing a CTR does not flag the transaction as suspicious. It is a threshold-based reporting requirement, not a judgment call.

The $10,000 Threshold and Aggregation Rules

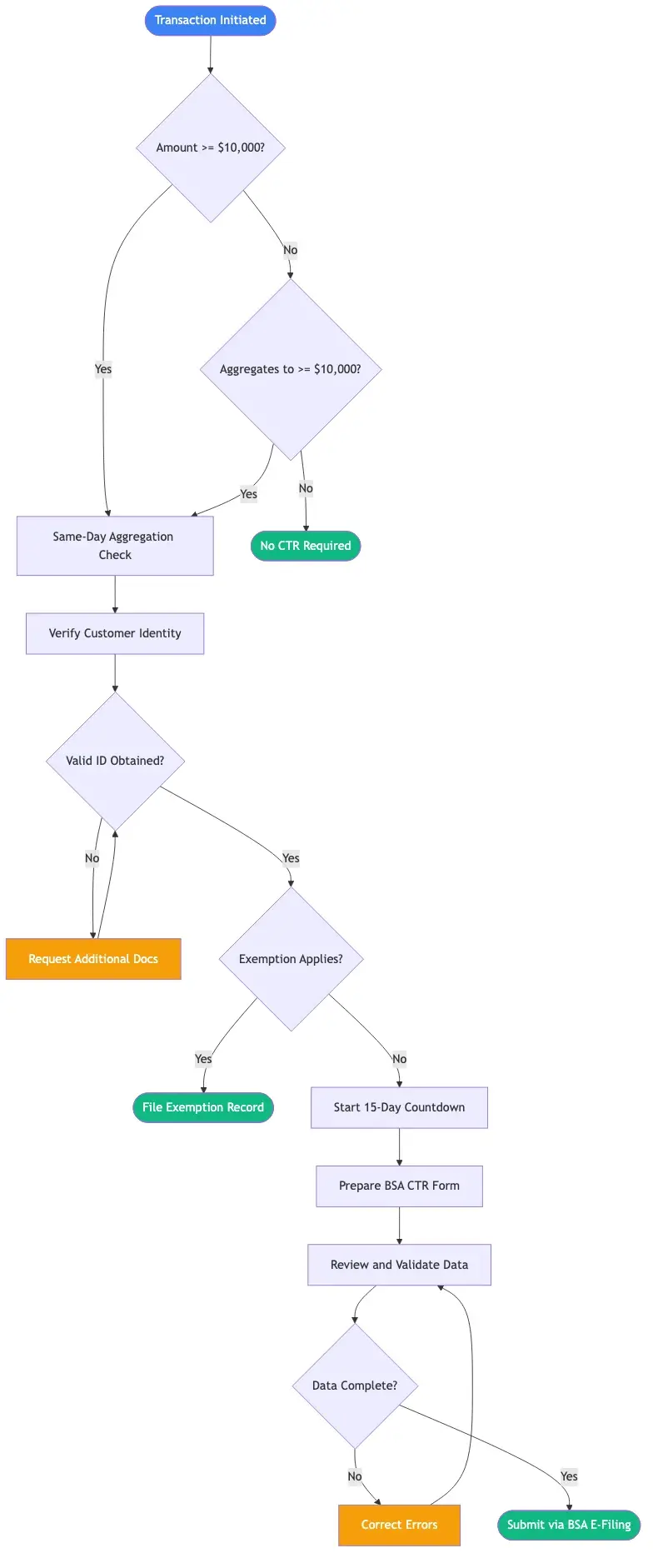

The $10,000 limit applies to the aggregate of all cash transactions by or on behalf of a single customer in a single business day. A customer depositing $6,000 in the morning and $5,000 in the afternoon crosses the threshold, triggering a CTR on both transactions combined.

This aggregation rule is designed to catch structuring: intentionally splitting transactions to stay below the threshold. Structuring is a federal crime under 31 U.S.C. § 5324, regardless of whether the underlying funds are from legal sources. Anti-money laundering technology built for multi-channel aggregation catches this far more reliably than manual branch-level review.

Who Must File and Exemptions

Most federally regulated financial institutions must file. The BSA allows "Phase I" and "Phase II" exemptions for publicly traded companies, listed businesses with stable transaction histories, and payroll accounts. These exemptions must be documented and reviewed annually. An outdated exemption applied to a customer whose business model has changed is a liability, not a protection.

Structuring and Aggregation: The Compliance Traps That Catch Teams Off Guard

Manual aggregation across teller systems, ATMs, and multiple branch locations is exactly where errors accumulate. A customer transacting at three different branches on the same day may not be caught by a single-system check. This is why aml compliance software built for multi-channel aggregation has become a baseline requirement for institutions with more than one location or payment channel.

CTR Filing Rules Under the Bank Secrecy Act

Understanding ctr filing rules means knowing both the technical requirements and the operational deadlines. FinCEN requires CTRs to be filed electronically via the BSA E-Filing System within 15 calendar days of the transaction date. There is no grace period. Each late or missing CTR is a separate violation.

BSA/AML Compliance Checklist for CTR Reporting

A working bsa aml compliance checklist for CTR reporting should include:

- Transaction monitoring: Real-time or end-of-day cash aggregation across all channels

- Customer identification: Verified name, address, SSN or TIN, and government-issued ID

- Beneficial ownership: For business accounts, identify owners with 25% or more control

- Exemption register: Active list of Phase I and Phase II exemptions with annual review dates

- E-filing credentials: BSA E-Filing System account maintained and tested quarterly

- Filing deadline tracker: 15-day countdown triggered automatically from transaction date

- Quality review: Supervisor sign-off before submission

For community banks running lean compliance teams, this checklist is the operational baseline. The FFIEC BSA/AML Examination Manual covers examiner expectations in detail, including which documentation gaps most commonly trigger Matters Requiring Attention.

Filing Deadlines and Penalties for Non-Compliance

Missing the 15-day window carries civil penalties up to $25,000 per day per violation. Willful violations can trigger criminal penalties up to $250,000 per violation. FinCEN has followed through: community banks have faced multi-million dollar fines for systematic CTR failures, not just isolated errors.

The practical problem is volume. A mid-size bank processing 2,000 cash transactions daily may generate 40 to 80 CTR-eligible events. Reviewing all of them manually within 15 days, at consistent quality, requires more staffing than most institutions can sustain.

How CTR Filing Rules Automation Reduces Compliance Risk

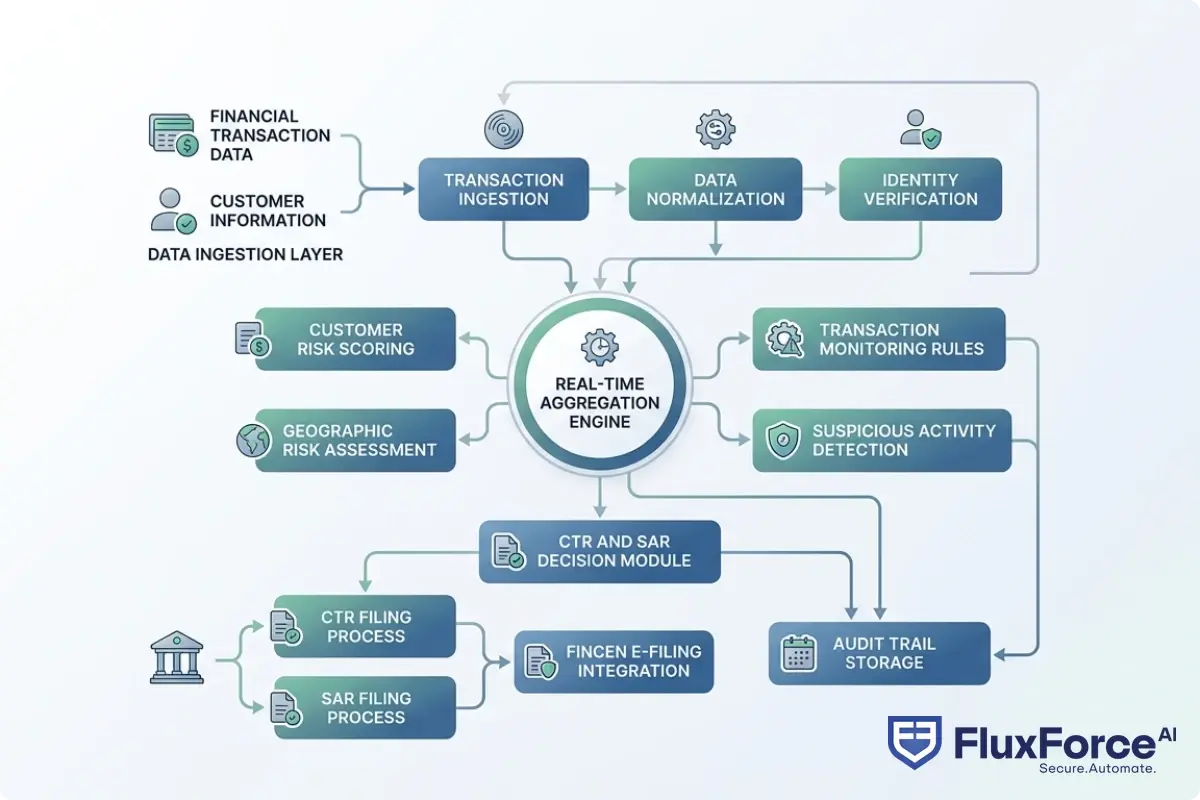

CTR filing rules automation means using software to detect, aggregate, validate, and submit CTR filings with minimal human intervention. Done well, it cuts filing time from hours to minutes, reduces data entry errors to near zero, and creates an auditable trail that regulators look for during examinations.

In 2026, platforms built around machine learning handle not just threshold detection but contextual decisions: does this pattern suggest structuring? Does this customer qualify for an exemption? Should this CTR trigger a parallel SAR review?

How Automated Monitoring Catches What Manual Review Misses

Manual review works for single, obvious transactions above $10,000. It fails for multi-branch aggregations, rapid cash cycles, or customers using multiple account holders on the same business day.

Manual review works for single, obvious transactions above $10,000.

Automated systems apply rules consistently across every channel, every time. If a customer's cash pattern shifts from $2,000 per week to $9,500 three times per week, the system flags it even if no single transaction hits the threshold. As analyzed in our deep-dive on how agentic AI fraud agents cut false positives by 80%, the same AI-driven approach that reduces alert noise in fraud detection applies directly to AML transaction monitoring.

Reducing False Positives in Transaction Monitoring

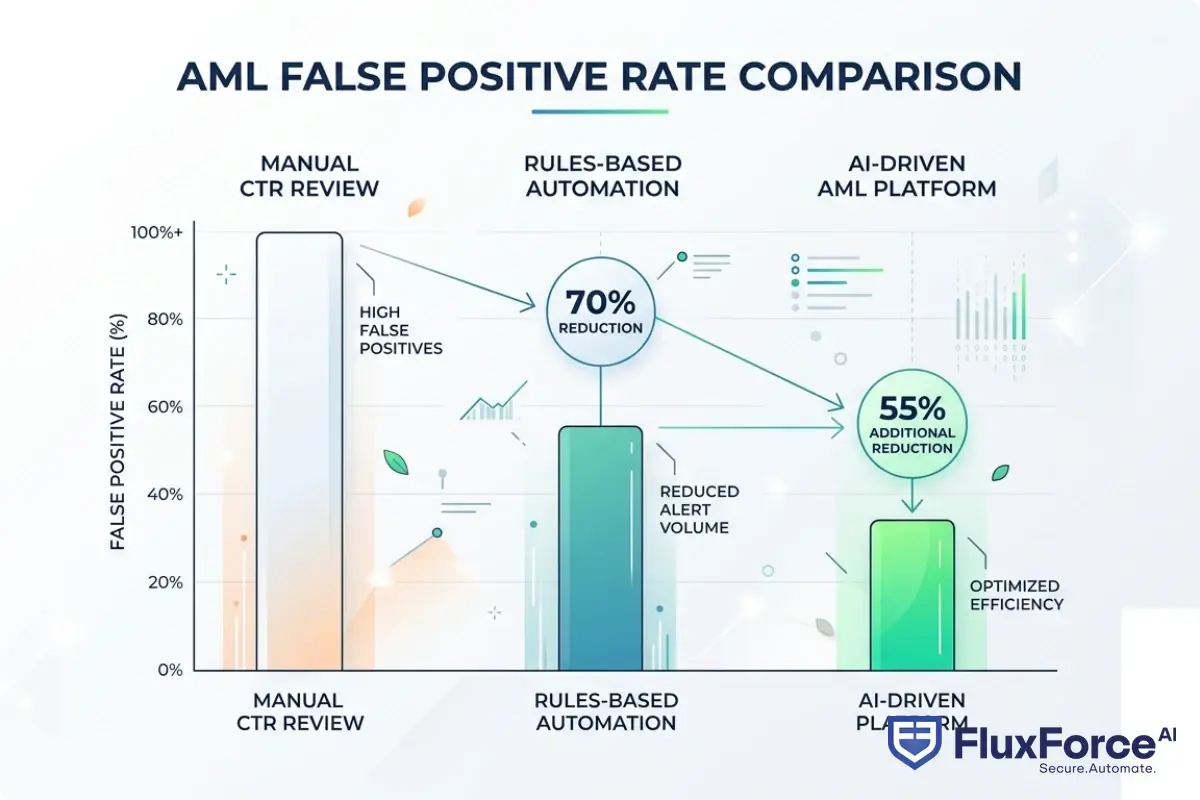

One honest limitation of automation: early rules-based systems generated enormous false positive rates. Some institutions reported 90 to 95% of alerts being non-actionable. Staff reviewing false positives are not reviewing real risk, and alert fatigue causes genuine red flags to be missed.

Modern aml compliance software addresses this with risk scoring instead of binary triggers. Rather than flagging every transaction near $10,000, the system scores each event against customer history, geographic norms, business type, and seasonal patterns. Only high-confidence matches go to human review.

AML Compliance Software and Anti-Money Laundering Technology 2026

The aml compliance fintech space has consolidated significantly since 2022. What was once a fragmented market of point solutions (one tool for transaction monitoring, another for CTR filing, another for SAR management) is shifting toward integrated platforms covering the full AML workflow from customer onboarding through regulatory reporting.

Key Features of Modern AML Compliance Platforms

Compliance officers evaluating aml compliance software in 2026 should look for:

- Real-time transaction aggregation across ACH, wire, cash, and digital wallets

- Automated CTR generation with pre-populated FinCEN fields from your core banking system

- Integrated SAR workflow that flags suspicious activity alongside CTR filing

- Case management with audit trails, notes, and supervisor approval workflows

- API-first architecture for integration with existing core banking systems

Moving to API-first compliance infrastructure has made it far easier to add AML capabilities without a full core banking replacement. Our piece on AI-powered API gateways for fintech compliance covers the architecture decisions involved.

EU AI Act Considerations for Financial Services

For institutions serving European markets, eu ai act financial services requirements add a new compliance layer. AML systems using AI for risk scoring are likely classified as "high-risk AI systems" under the Act, meaning documentation, explainability, and human oversight requirements apply to your AML platform. Anti-money laundering technology 2026 deployments for EU-facing operations should incorporate these requirements into procurement specifications now.

The EU AI Act's obligations for high-risk systems began phasing in during 2025. Institutions deploying opaque AI-based AML models without explainability face dual exposure: FinCEN or FCA enforcement on one side, and EU AI Act non-compliance on the other.

SAR Filing Efficiency: Connecting CTRs to Suspicious Activity Reports

CTRs and SARs serve different functions but frequently arise from the same transaction data. A CTR is mandatory and objective: triggered by a dollar threshold. A SAR is judgment-based: filed when a bank suspects illegal activity regardless of transaction size. Good sar filing efficiency means managing both in parallel without doubling the compliance workload.

SAR Filing Best Practices

The suspicious activity report guide from FinCEN sets minimum standards, but sar filing best practices go further:

- Document the decision-making process: Not just what you filed, but why. Regulators want evidence that judgment was applied.

- Apply the 30-day rule correctly: SARs must be filed within 30 calendar days of initial detection, with a 60-day extension if no suspect is identified.

- Avoid over-filing and under-filing equally: Over-filing trains regulators to discount your reports. Under-filing creates enforcement exposure.

- Coordinate CTR and SAR workflows: A $12,000 cash deposit that is both CTR-eligible and suspicious requires both reports simultaneously.

For institutions managing sanctions alongside SAR requirements, our analysis of sanctions screening automation for CISOs covers how integrated platforms handle both from a single case management interface.

SAR Filing Requirements for 2026

sar filing requirements 2026 maintain the core FinCEN structure but incorporate updated guidance: separate filing categories for ransomware, business email compromise, and cryptocurrency fraud; cross-referencing with FinCEN's Beneficial Ownership database (operational since 2024); and stricter narrative quality standards requiring specific, factual language rather than template-generated boilerplate.

BSA/AML Compliance for Community Banks and Fintech Teams

The compliance burden does not scale down for smaller institutions. A community bank with $500 million in assets faces the same ctr filing rules as a $100 billion bank. The difference is available resources.

A community bank with $500 million in assets faces the same ctr filing rules as a $100 billion bank.

BSA/AML Compliance for Community Banks

bsa aml compliance community banks face a specific challenge: long-standing customer relationships that make objective screening harder. A local business owner depositing $15,000 from a weekend market is a trusted customer, but the CTR still applies. The risk is that familiarity breeds procedural complacency.

The best model for community banks: automate routine CTR filings, reserve human judgment for exemption reviews and SAR decisions, and document every step. Most exam failures trace back to documentation gaps, not wrongdoing. Our post on regulatory compliance reporting for payments risk officers covers this documentation discipline in practical terms.

Fintech BSA/AML for Small Teams

fintech bsa aml small team operations face a different constraint: high transaction volumes with compliance staff of two or three people. A neobank processing 50,000 transactions per day cannot manually review CTR candidates. The aml risk assessment guide for these teams points one direction: automate everything automatable, and invest in tools that surface only decisions requiring human judgment.

Cloud-native AML platforms now handle full BSA compliance at a fraction of enterprise costs, with APIs that plug directly into payment stacks. Our analysis of AML screening strategies for payments risk officers covers platform considerations relevant to fintech teams operating at scale with limited headcount.

KYC Automation and Enhanced Due Diligence for Banks

CTR compliance does not exist in isolation. Every CTR filed requires verified customer identity. Every SAR filed requires understanding who the customer is and what normal behavior looks like. That makes kyc automation 2026 a direct dependency of AML compliance, not a parallel workstream.

KYC/CDD Requirements and Enhanced Due Diligence

kyc cdd requirements banks must meet under FinCEN's Customer Due Diligence Rule include verified customer identification, beneficial ownership disclosure for legal entities (25% or more equity), risk-based customer profiles assigned at onboarding, and ongoing monitoring to flag behavioral deviations.

For high-risk customers, the enhanced due diligence guide adds source of funds documentation, tighter monitoring thresholds, and more frequent periodic reviews. kyc automation 2026 tools now complete identity verification in under 60 seconds using document scanning, liveness detection, and sanctions screening in a single API call. The FATF Recommendations on customer due diligence remain the international framework most national regulators, including FinCEN, use as the basis for CDD program requirements.

One honest tradeoff: kyc automation tools are only as effective as the data they check against. Sanctions lists have known coverage gaps and documents can be forged. Automation reliably catches known bad actors and accelerates legitimate onboarding. It does not replace human judgment for complex geopolitical exposure or adverse media reviews.

- A Currency Transaction Report is a mandatory disclosure filed with FinCEN whenever a customer conducts a cash transaction exceeding $10,000 in a single business day.

- Understanding ctr filing rules means knowing both the technical requirements and the operational deadlines.

- CTR filing rules automation means using software to detect, aggregate, validate, and submit CTR filings with minimal human intervention.

- The aml compliance fintech space has consolidated significantly since 2022.

- CTRs and SARs serve different functions but frequently arise from the same transaction data.

Onboard Customers in Seconds

Conclusion

CTR filing rules automation sits at the center of how financial institutions are rebuilding aml compliance for 2026. The $10,000 threshold has not changed since 1970, but the transaction volumes, money laundering techniques, and multi-channel complexity around it have changed everything.

Manual CTR processing is a liability now, not just an inefficiency. Modern aml compliance software makes accurate, on-time filing with full audit trails achievable at a fraction of manual cost. The same platforms that handle CTR automation also connect sar filing efficiency, kyc automation 2026, and ongoing monitoring into one workflow. Institutions that have made that shift are spending less on compliance operations and passing exams more cleanly. The gap between them and those still relying on manual processes is widening every quarter. That is what ctr filing rules automation delivers in practice.

Share this article