.webp)

Introduction

Compliance training for financial institutions is no longer just a box-checking exercise. The regulatory environment has made that clear in the most expensive way possible. In 2023 alone, global financial penalties for AML non-compliance exceeded $6 billion, with regulators citing inadequate staff training and weak compliance cultures as root causes in the majority of enforcement actions. Banks, fintechs, community lenders, and insurance carriers face the same uncomfortable truth: having a compliance program on paper is not the same as having one that works.

In 2023 alone, global financial penalties for AML non-compliance exceeded $6 billion, with regulators citing inadequate staff training and weak compliance cultures as root causes in the majority of enforcement actions.

This post breaks down what effective compliance training actually looks like in 2026, why AML compliance software and KYC automation are now core infrastructure, and how institutions of every size can build a compliance culture that holds up under real regulatory scrutiny.

- Why Compliance Training for Financial Institutions Keeps Failing

- AML Compliance: The Foundation Banks and Fintechs Can't Skip

- How AML Compliance Software Transforms BSA/AML Programs

- What Is BSA/AML Compliance? A Checklist for Community Banks

- SAR Filing Efficiency: From Bottleneck to Streamlined Process

Onboard Customers in Seconds

Why Compliance Training for Financial Institutions Keeps Failing

Most compliance training programs fail for a specific, fixable reason: they're designed to satisfy auditors, not to change behavior. Annual 45-minute e-learning modules with multiple-choice quizzes score well on completion metrics but score poorly on the actual goal, which is reducing the risk of financial crime.

Regulators have noticed. The OCC's Comptroller's Handbook on BSA/AML explicitly calls out check-the-box training as inadequate, noting that examiners will assess whether training programs are tailored to employees' specific roles and risk exposures. That's a significant shift from accepting generic AML training as sufficient.

The Gap Between Annual Training and Real Behavioral Change

Studies from the Association of Certified Anti-Money Laundering Specialists (ACAMS) consistently show that knowledge retention drops below 30% within two weeks of a single-session training event. Role-specific, scenario-based training delivered in shorter bursts performs significantly better, with retention rates closer to 65-70% when reinforced with practical application.

Annual training works fine for checking a regulatory box. It does almost nothing for building genuine compliance instincts in front-line staff, relationship managers, or operations teams who encounter suspicious transactions daily.

What Regulators Look for in a Compliance Culture

Regulators assess compliance culture through observable behaviors, not training completion certificates. Examiners from the FDIC, OCC, and Federal Reserve look for evidence that employees understand their specific responsibilities, know how to escalate concerns, and feel psychologically safe doing so.

The FinCEN BSA/AML compliance guidance is direct on this point: the culture-of-compliance pillar requires demonstrable commitment from the board and senior management, not just sign-off on a policy document.

AML Compliance: The Foundation Banks and Fintechs Can't Skip

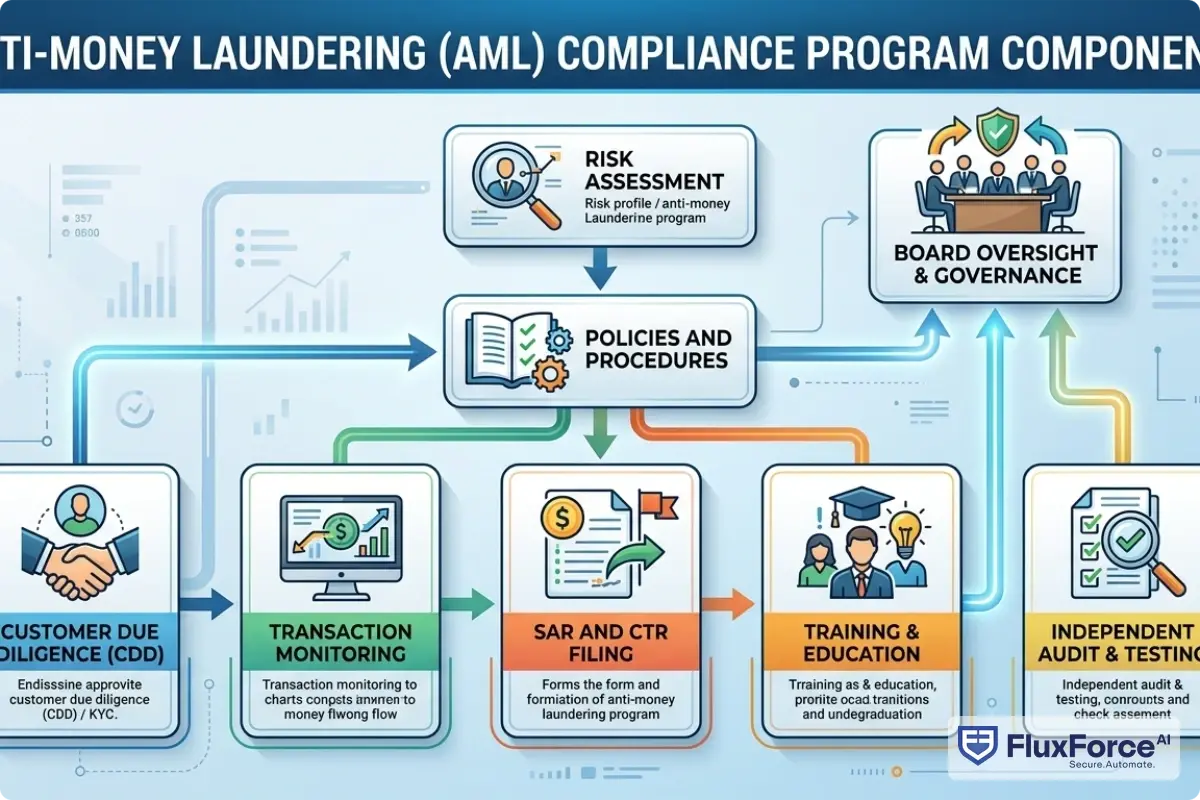

AML compliance is the set of policies, procedures, and controls that financial institutions use to detect, prevent, and report money laundering activity. For U.S. institutions, AML compliance is governed primarily by the Bank Secrecy Act (BSA) and administered by FinCEN, with examination authority delegated to the OCC, FDIC, Federal Reserve, and NCUA depending on the charter type.

For fintechs operating with banking-as-a-service partners or direct licenses, aml compliance fintech requirements carry the same regulatory weight as traditional banks, often with significantly less compliance infrastructure to support them.

AML Risk Assessment Guide for Structured Programs

A credible AML program starts with a documented risk assessment. The FFIEC BSA/AML Examination Manual describes this as the process by which an institution identifies, measures, and prioritizes its money laundering risks across customers, products, services, and geographies. Your aml risk assessment guide is not a static document, it updates when you launch new products, enter new markets, or when your customer base changes materially.

The practical components include: customer risk rating methodology, product and service risk evaluation by transaction type, geographic risk mapping for correspondent relationships, residual risk documentation after controls are applied, and an annual review process with board-level sign-off.

Anti Money Laundering Technology as a Force Multiplier

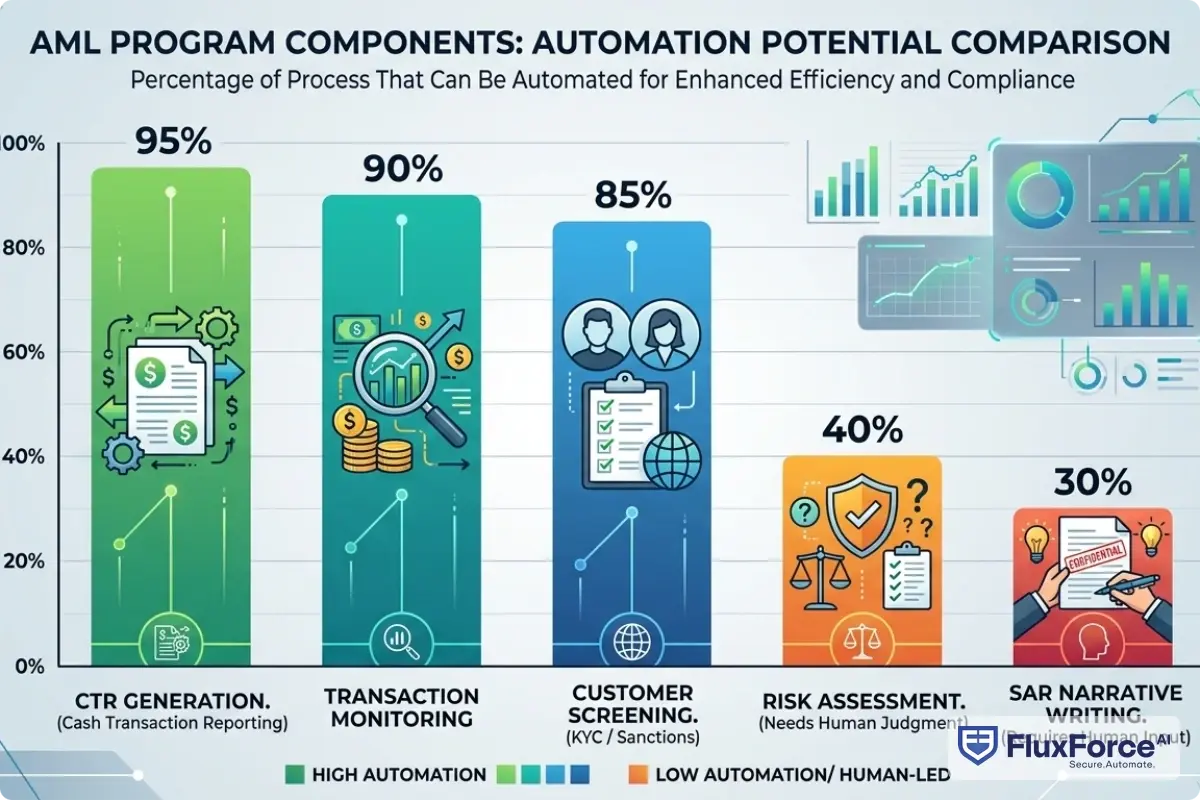

Anti money laundering technology has matured considerably over the past five years. Transaction monitoring systems, name screening platforms, and entity resolution tools now use machine learning models that significantly outperform rule-based systems in detecting complex layering schemes. The practical benefit: technology allows smaller teams to monitor larger transaction volumes without proportional headcount increases.

Technology only works as well as the data feeding it. Institutions frequently over-invest in monitoring platforms while under-investing in the data governance and model validation required to make those platforms accurate.

How AML Compliance Software Transforms BSA/AML Programs

AML compliance software has shifted from monolithic, on-premise systems to modular, API-first platforms that integrate with core banking systems, payment processors, and data providers. This lowers the barrier to entry for community banks and fintechs that previously couldn't afford enterprise-grade monitoring infrastructure.

When comparing platforms, consider:

| Capability | What to Look For |

|---|---|

| Transaction Monitoring | Configurable thresholds plus ML anomaly detection |

| Case Management | Audit trails, workflow assignment, SLA tracking |

| SAR Filing | Direct FinCEN integration or batch export |

| KYC/CDD | Automated screening plus ongoing monitoring |

| Reporting | Regulator-ready dashboards plus data export |

Anti Money Laundering Technology 2026: What's Actually Different

The biggest shift in anti money laundering technology 2026 is the adoption of network analytics and graph-based detection. Traditional transaction monitoring looks at individual transactions in isolation. Network analytics maps relationships between accounts, beneficial owners, and counterparties to identify coordinated patterns that look innocuous when viewed account-by-account.

Under eu ai act financial services provisions, AML systems that inform consequential decisions about customers require human oversight documentation, model transparency, and ongoing bias monitoring. U.S. institutions with EU operations need to be ahead of this requirement before examination cycles surface the gap.

Fintech BSA AML for Small Teams: Doing More With Less

Aml compliance fintech programs present a specific challenge: regulatory expectations match those of chartered banks, but team sizes are a fraction of what a regional bank carries. A fintech with 12 compliance staff supporting $2B in payments volume faces the same SAR filing obligations, CTR filing rules, and customer due diligence requirements as an institution ten times its size.

A fintech with 12 compliance staff supporting $2B in payments volume faces the same SAR filing obligations, CTR filing rules, and customer due diligence requirements as an institution ten times its size.

The practical answer for a fintech bsa aml small team is ruthless prioritization. Automate customer screening, transaction monitoring alerts, and CTR auto-generation. Reserve human judgment for complex SAR narratives, high-risk customer approvals, and model governance. AML Screening in Digital Lending offers a practical framework directly applicable to payments-focused compliance teams.

What Is BSA/AML Compliance? A Checklist for Community Banks

BSA/AML compliance is the practice of maintaining an anti-money laundering program that satisfies the requirements of the Bank Secrecy Act, its implementing regulations at 31 CFR Chapter X, and the AML/CFT Act of 2020. The five-pillar framework established by FinCEN requires every covered institution to maintain: a system of internal controls, independent testing, a designated BSA/AML compliance officer, training for appropriate personnel, and a customer identification program.

For smaller institutions, the bsa aml compliance checklist below covers the minimum requirements that examiners verify in every BSA/AML examination.

BSA AML Compliance Checklist: The Non-Negotiables

- Documented risk assessment completed within the past 12 months

- Written AML program adopted by the board

- Designated BSA Officer with documented authority and resources

- Customer Identification Program (CIP) procedures

- Customer Due Diligence (CDD) rule compliance, including beneficial ownership for legal entities

- Transaction monitoring system with documented rule rationale

- SAR filing procedures and timely submission records (30-day deadline after suspicious activity is identified)

- CTR filing for cash transactions over $10,000

- Annual independent AML program testing

- Role-specific training with documented completion and dates

- Procedures for responding to law enforcement requests (314(a) and 314(b))

BSA AML Compliance for Community Banks: Specific Considerations

BSA AML compliance community banks face a distinct set of challenges. Community banks typically have concentrated customer bases in specific geographies, strong local relationships that can complicate objective risk assessment, and limited compliance staff who wear multiple hats.

Examiners apply a risk-based approach. A community bank with a straightforward retail deposit book and no foreign correspondent relationships doesn't need the same monitoring sophistication as a global bank. What examiners do expect is that the program matches the institution's actual risk profile. For institutions navigating KYC/AML obligations across product lines, AML Risk Checks in Policy Issuance provides useful parallels for how CDD obligations apply in different contexts.

SAR Filing Efficiency: From Bottleneck to Streamlined Process

SAR filing is where compliance programs either demonstrate operational competence or reveal structural problems. The Suspicious Activity Report is a confidential disclosure to FinCEN that triggers law enforcement visibility into potential financial crime. Getting it wrong creates regulatory and legal exposure.

SAR filing efficiency matters because the window is narrow: institutions have 30 calendar days from the date suspicious activity is first identified to file, with a 60-day extension available for particularly complex matters. Most compliance teams that miss deadlines do so not because they didn't identify the activity, but because case management workflows were too slow to complete the narrative and supervisory review in time.

SAR Filing Best Practices That Survive Regulatory Scrutiny

A suspicious activity report guide for compliance analysts should emphasize the 5W structure: who, what, when, where, and why the activity is suspicious. A report that describes the activity with precision, explains why it deviates from expected behavior, and provides all available identifying information is exponentially more useful than a vague report that just logs a transaction amount.

SAR filing best practices include: documenting the detection date separately from the filing date, using specific dollar amounts and transaction dates rather than approximations, citing the pattern of activity rather than a single transaction, including all involved parties with identifying information, and explaining what normal behavior looks like for this customer type before describing the deviation.

SAR Filing Requirements 2026: What's Changed

SAR filing requirements 2026 reflect continued FinCEN focus on beneficial ownership and virtual asset reporting. The Corporate Transparency Act's beneficial ownership database, fully operational since 2024, gives compliance teams a new verification resource and additional data source for SAR subject identification.

The FATF Recommendations on digital assets provide the international baseline that domestic regulators are aligning with. For an in-depth look at how AI reduces false positive alerts generating unnecessary SAR review queues, How Agentic AI Fraud Agents Cut False Positives by 80% is worth reviewing before your next transaction monitoring calibration exercise.

KYC Automation in 2026: Rethinking Customer Due Diligence

KYC automation addresses one of the highest-volume, most error-prone processes in compliance: customer onboarding and ongoing monitoring. A mid-size bank processing 500 new business accounts per month through manual CDD review allocates roughly 8-12 hours of analyst time per complex account, before any enhanced due diligence is triggered.

KYC automation 2026 platforms use document verification APIs, identity graph databases, and automated screening to cut that time by 70-80% for standard-risk accounts, while flagging genuinely complex cases for human review.

KYC automation 2026 platforms use document verification APIs, identity graph databases, and automated screening to cut that time by 70-80% for standard-risk accounts, while flagging genuinely complex cases for human review.

KYC CDD Requirements for Banks: The Regulatory Baseline

The kyc cdd requirements banks must satisfy originate from FinCEN's CDD Rule (31 CFR 1020.220), which took effect in 2018 and was strengthened by the AML/CFT Act of 2020. The four core CDD elements are:

- Customer identification (CIP): Verify name, date of birth, address, and identification number for individuals

- Customer due diligence: Understand the nature and purpose of the customer relationship

- Beneficial ownership: Identify and verify individuals with 25% or more ownership or significant control of legal entities

- Ongoing monitoring: Update customer information and monitor transactions for activity consistent with the customer's profile

Enhanced Due Diligence Guide for High-Risk Relationships

An enhanced due diligence guide for relationship managers should specify what additional information is required, how it's verified, and what approval authority is needed before a relationship proceeds. For politically exposed persons (PEPs), foreign correspondent accounts, and private banking relationships, enhanced due diligence is mandatory rather than discretionary.

Key components: source of wealth documentation with independent verification, negative news screening beyond standard watchlist checks, senior management approval for relationship initiation, enhanced ongoing monitoring with more frequent review triggers, and annual relationship review regardless of transaction patterns. KYC for InsurTech provides a practical CDD implementation framework applicable across financial product types.

Turning Compliance Training at Financial Institutions Into a Strategic Asset

The goal is not a compliance program that satisfies regulators. The goal is a compliance program that prevents financial crime, protects the institution, and builds trust with customers and counterparties.

Compliance training for financial institutions that actually builds culture does four things differently from check-the-box programs:

- Role specificity: Tellers get teller training. Relationship managers get training on CDD for commercial clients. Generic training fails because it applies to no one specifically.

- Scenario realism: Training uses cases drawn from the institution's own customer types, products, and geographic markets.

- Leadership visibility: When the CEO and board chair take the same training as front-line staff, the compliance culture message is credible. When training is something the board delegates entirely to the compliance department, staff notice the difference.

- Feedback loops: Training connected to actual suspicious activity cases (appropriately anonymized) teaches staff what real compliance decisions look like in practice.

CTR Filing Rules and How Automation Reduces Error Rates

CTR filing rules require financial institutions to file a Currency Transaction Report with FinCEN for any cash transaction over $10,000. The 15-calendar-day filing deadline is strict, and errors in CTR filings, such as wrong identification, missing aggregation, or incorrect business classification, are a common examination finding.

Automation reduces CTR errors substantially. Systems that automatically aggregate cash transactions across accounts, apply exemption logic for qualified businesses, and pre-populate identification fields from the core banking system reduce manual entry errors to near zero. For teams evaluating the trade-off between manual processes and automation, Manual Compliance vs. AI Automation covers both the efficiency gains and governance considerations in detail.

EU AI Act Financial Services: Compliance Implications in 2026

The eu ai act financial services provisions classify transaction monitoring and customer risk scoring systems as high-risk AI when they inform consequential decisions about individuals. For institutions operating in or with EU counterparties, AML models need documented governance: training data provenance, model performance metrics, human oversight procedures, and bias assessments.

The practical approach is to integrate AI governance into your existing model risk management framework rather than creating a parallel process. U.S. institutions with EU operations should map their AML AI systems against the high-risk categories now, before examination cycles surface the gap.

- Most compliance training programs fail for a specific, fixable reason: they're designed to satisfy auditors, not to change behavior.

- AML compliance is the set of policies, procedures, and controls that financial institutions use to detect, prevent, and report money laundering activity.

- AML compliance software has shifted from monolithic, on-premise systems to modular, API-first platforms that integrate with core banking systems, payment processors, and data providers.

- BSA/AML compliance is the practice of maintaining an anti-money laundering program that satisfies the requirements of the Bank Secrecy Act, its implementing regulations at 31 CFR Chapter X, and the AML/CFT Act of 2020.

- SAR filing is where compliance programs either demonstrate operational competence or reveal structural problems.

Conclusion: Making Compliance Training for Financial Institutions Stick

Compliance training for financial institutions sits at the intersection of regulatory obligation and genuine risk management. Getting it right requires more than annual e-learning and a complete BSA/AML policy binder. It requires role-specific training, technology that handles high-volume routine tasks, rigorous SAR filing and CTR filing processes, and KYC automation that frees analysts to focus on genuinely complex decisions.

The institutions that build a real compliance culture treat aml compliance as infrastructure. AML compliance software, anti money laundering technology, and kyc automation 2026 tools provide the foundation. But the culture is built by leadership, reinforced by training, and tested by how the organization responds when suspicious activity actually hits the queue.

Start with the BSA/AML compliance checklist, run an honest risk assessment against your current control environment, and identify where manual processes create the most timeline and quality risk. That's where technology investments pay off fastest, and where a culture of compliance becomes something regulators see rather than just something compliance teams claim to have.

Onboard Customers in Seconds

Share this article