.webp)

Introduction

The beneficial ownership CTA requirements introduced by the Corporate Transparency Act have forced every compliance team in banking and fintech to rethink how they collect, verify, and report ownership data. Passed as part of the National Defense Authorization Act in 2021 and enforced by FinCEN beginning January 2024, the CTA requires most U.S. corporations, LLCs, and similar entities to disclose who ultimately owns or controls them. For compliance officers, this isn't just a reporting checkbox. It changes how you run your AML compliance program, what your KYC workflows look like, and how you connect ownership data to SAR decisions.

This guide breaks down what the CTA actually requires, how it fits into a broader BSA/AML framework, and what tools and processes you need to stay compliant through 2026 and beyond.

- What Are Beneficial Ownership CTA Requirements?

- How Beneficial Ownership Rules Reshape AML Compliance

- BSA/AML Compliance Checklist for CTA Readiness

- CTA Compliance for Community Banks and Fintechs

- How KYC Automation Simplifies Ownership Verification in 2026

Onboard Customers in Seconds

What Are Beneficial Ownership CTA Requirements?

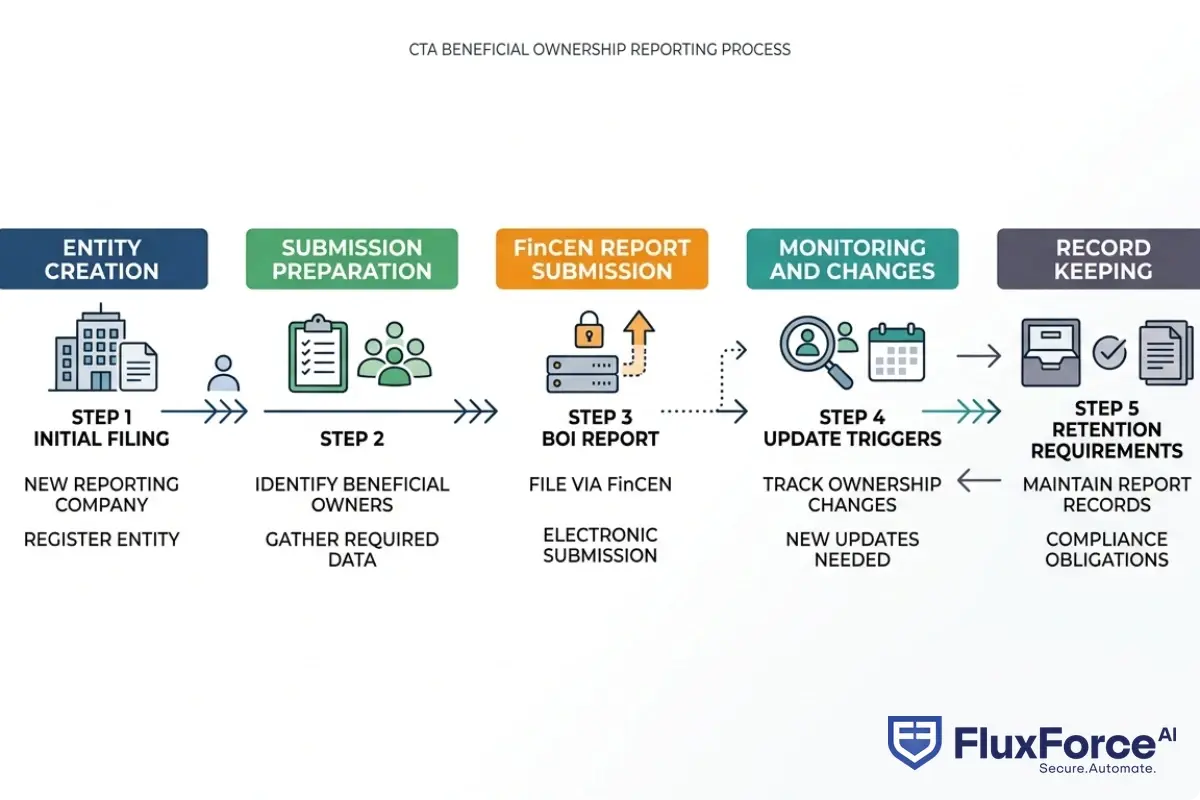

Beneficial ownership CTA requirements mandate that "reporting companies" file Beneficial Ownership Information (BOI) reports with the Financial Crimes Enforcement Network (FinCEN). A beneficial owner is any individual who directly or indirectly owns 25% or more of an entity's equity interests, or who exercises substantial control over the company.

A beneficial owner is any individual who directly or indirectly owns 25% or more of an entity's equity interests, or who exercises substantial control over the company.

The CTA covers an estimated 32.6 million existing entities as of 2024, with roughly 5 million new entities expected to file annually going forward. That scale makes this one of the most consequential AML transparency initiatives in U.S. history.

Who Must File a Beneficial Ownership Information Report?

Any domestic or foreign entity registered to do business in a U.S. state must file unless it qualifies for one of 23 specific exemptions. Exempt categories include:

- Large operating companies with more than 20 full-time U.S. employees, a physical U.S. office, and more than $5 million in annual revenue from U.S. sources

- Banks, credit unions, and registered investment advisers already subject to federal financial oversight

- Securities reporting issuers that file with the SEC

If your entity doesn't fit an exemption, you're in scope. Many shell companies, small LLCs, and holding structures that were previously invisible to regulators now have to surface their ownership chains.

Key Deadlines and Exemptions Under the CTA

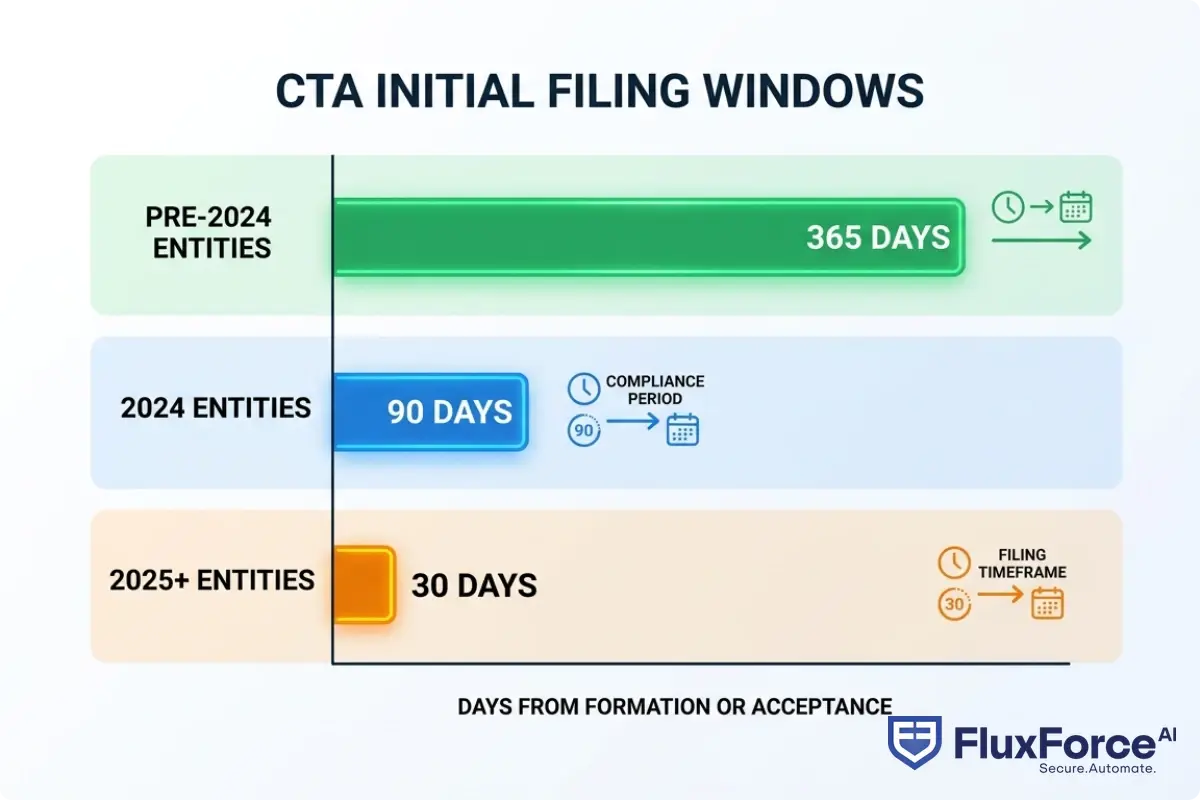

Entities formed before January 1, 2024 had until January 1, 2025 to file initial reports. Entities formed during 2024 had 90 days from formation. Entities formed on or after January 1, 2025 have 30 days to file. Updates must be submitted within 30 days of any ownership change.

FinCEN's enforcement approach includes civil penalties of up to $591 per day for willful non-compliance and criminal penalties of up to $10,000 and two years imprisonment for fraudulent filings. Those aren't soft guidelines.

FinCEN's enforcement approach includes civil penalties of up to $591 per day for willful non-compliance and criminal penalties of up to $10,000 and two years imprisonment for fraudulent filings.

How Beneficial Ownership Rules Reshape AML Compliance

For most institutions, the CTA doesn't replace existing AML compliance obligations. It adds another data layer on top of them. The question is whether your current program can absorb that layer without creating new gaps or duplicate processes.

AML Risk Assessment Guide for CTA-Regulated Entities

A proper aml risk assessment guide for the CTA era needs to address three new dimensions. First, evaluate which of your customers' entities are required to file BOI and whether their reported ownership matches what you have on file from onboarding. Second, assess how your transaction monitoring rules account for ownership-related risk signals. Third, determine how BOI data feeds into your customer risk scoring model.

The Financial Action Task Force (FATF) has consistently identified beneficial ownership transparency as a critical weak point in global AML frameworks. The CTA brings U.S. requirements closer to the standards FATF has recommended for over a decade, which matters especially for institutions with cross-border operations or correspondent banking relationships.

Connecting CTA Data to Your AML Program

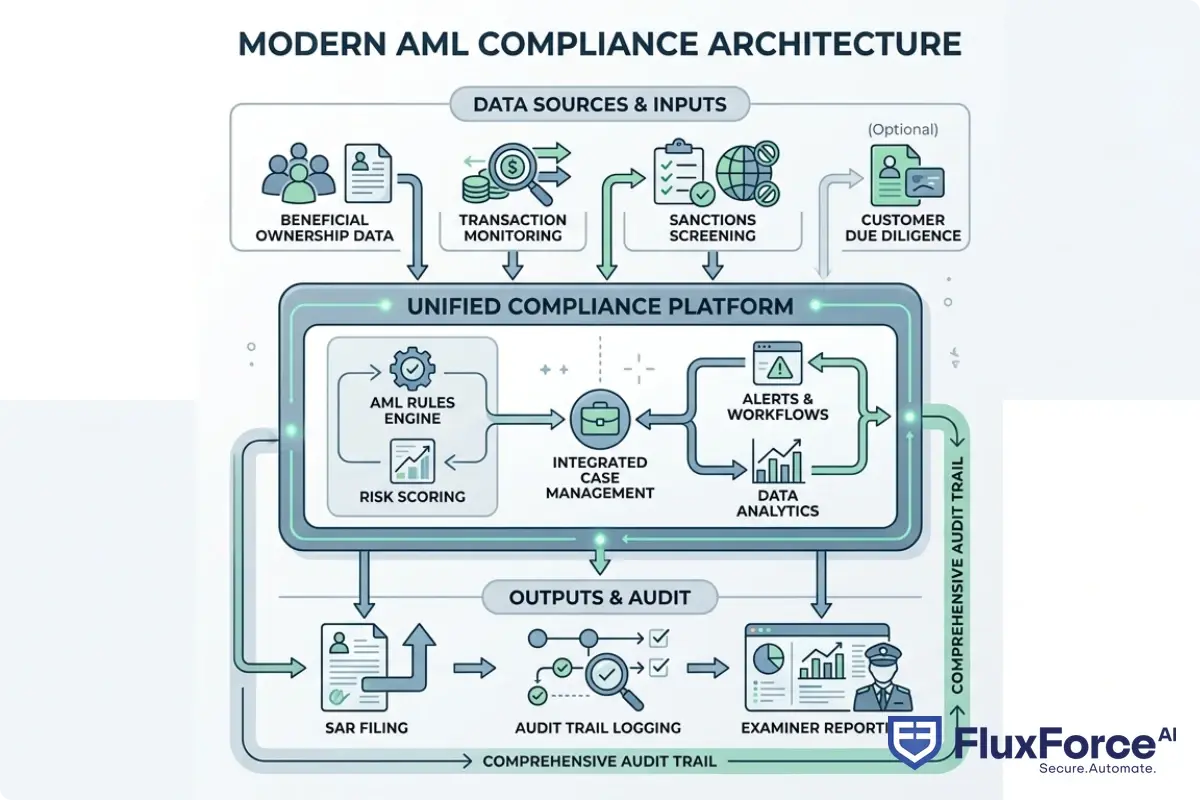

The honest answer here is that integrating BOI into AML workflows is trickier than it sounds. FinCEN's BOI database is not publicly accessible. Law enforcement and certain financial institutions can access it under specific protocols, but your compliance team cannot simply query it on demand. That means you need parallel verification processes: collecting ownership data directly from customers, validating it against available databases, and flagging discrepancies for review.

This is where AML screening and automated verification becomes essential. Manual verification across thousands of entities is a compliance bottleneck that grows faster than any team can scale to handle it.

BSA/AML Compliance Checklist for CTA Readiness

A bsa aml compliance checklist that doesn't account for CTA reporting is already outdated. Your program needs specific procedures for collecting BOI, validating it, and keeping it current as ownership structures change over time.

Core Elements of a BSA/AML Compliance Checklist

The Bank Secrecy Act requires covered institutions to maintain written policies, procedures, and controls. The CTA adds to this by requiring accurate and current ownership records. A checklist built for 2025 and beyond should include:

- Entity scoping: Identify which business customers are CTA reporting companies and which qualify for an exemption

- BOI collection: Gather full legal name, date of birth, residential address, and identifying document number for each beneficial owner

- Verification protocols: Cross-check submitted BOI against government-issued ID at onboarding and on any reported change

- Change tracking: Set up automated alerts when customers submit ownership updates or when discrepancies appear between BOI and KYC records

- Record retention: Keep BOI data for at least five years after the customer relationship ends

- Training updates: Revise AML training to cover CTA requirements and ownership-related red flags, including shell company indicators

This checklist differs from standard KYC in one important way: you're now responsible for tracking ownership structures continuously, not just at onboarding.

Fintech BSA/AML on a Small Team: What to Prioritize

For a fintech bsa aml small team managing compliance with limited headcount, the CTA creates real prioritization pressure. You can't build every control simultaneously. Focus first on your highest-risk customer segments: complex legal structures, customers in high-risk industries, and any entity showing signs of ownership layering.

Automate what you can. Automated alerts for ownership changes, API-connected identity verification, and risk-scored customer profiles will do more for a small team than adding more manual review steps. The goal is to concentrate capacity on genuinely high-risk situations rather than spending equal time on every entity in your portfolio.

CTA Compliance for Community Banks and Fintechs

The CTA's impact varies considerably by institution type. For a large bank with a dedicated compliance function and existing beneficial ownership procedures, the adjustment is real but manageable. For smaller institutions, the calculation is different.

BSA/AML Compliance for Community Banks Under the CTA

BSA/AML compliance for community banks presents specific challenges: these institutions typically serve local business customers with complex ownership structures, operate with smaller compliance teams, and work under tighter technology budgets than their larger counterparts. The CTA provides no smaller-institution carve-out for reporting obligations.

Community banks need to work through several practical questions. Do your existing KYC forms collect the information the CTA requires? Is there a documented process for reviewing customer-submitted BOI updates? Do examiners understand how your CTA procedures integrate with your overall BSA/AML program documentation?

The practical advantage community banks have is existing customer relationships built over years. That familiarity can accelerate ownership verification compared to institutions onboarding customers with no prior history. Lean on that relationship data when scoping your BOI collection effort.

AML Compliance Fintech Considerations in 2026

AML compliance fintech platforms face a different version of this problem. Many fintechs serve customers who are themselves small business entities, and the growth model depends on frictionless onboarding. Inserting beneficial ownership collection into that flow without creating meaningful drop-off is a genuine product design challenge.

The solutions that work in practice involve progressive disclosure: collect the minimum required at onboarding, then trigger BOI collection based on risk score or transaction behavior. This approach, paired with solid kyc automation 2026 tooling, keeps the user experience workable while satisfying the underlying regulatory requirement.

For more detail on building compliance workflows that work inside a digital-first product, this guide on KYC/AML identity verification strategy covers the underlying architecture decisions that apply directly here.

How KYC Automation Simplifies Ownership Verification in 2026

KYC automation has moved from optional to operationally necessary in the CTA era. Manual ownership verification doesn't scale when you're managing thousands of entities, each potentially with multiple beneficial owners, each requiring document verification and ongoing monitoring as structures change.

KYC/CDD Requirements for Banks and the CTA

KYC/CDD requirements for banks under FinCEN's Customer Due Diligence rule already required collecting beneficial ownership information for legal entity customers. The CTA extends this concept to the entities themselves, requiring them to proactively report their ownership structures rather than waiting to be asked by their financial institution.

For banks, this creates a useful cross-check opportunity: compare what customers report to FinCEN against what they disclosed during KYC onboarding. Discrepancies are a meaningful risk signal. Banks that integrate BOI cross-checking into their periodic customer review cycles will catch ownership obfuscation that would otherwise go undetected.

Enhanced Due Diligence Guide for High-Risk Beneficial Owners

Not all beneficial owners carry the same risk profile. An enhanced due diligence guide for CTA compliance should identify which ownership profiles trigger EDD: politically exposed persons (PEPs), owners with prior regulatory sanctions, owners connected to high-risk jurisdictions, and complex multi-tier ownership structures where ultimate control is difficult to trace.

EDD for beneficial owners typically involves adverse media screening, sanctions list checks against OFAC, UN, and EU designations, source of wealth analysis, and periodic re-verification. The kyc automation tools that handle this at scale are now mature. Agentic AI systems that run continuous screening on ownership data and flag changes in real time significantly reduce manual review burden without sacrificing coverage.

For a practical look at how AI reduces false positives in continuous ownership monitoring, see how agentic AI fraud agents cut false positives by 80%.

For a practical look at how AI reduces false positives in continuous ownership monitoring, see how agentic AI fraud agents cut false positives by 80%.

SAR Filing Efficiency and CTR Filing Rules Under the CTA

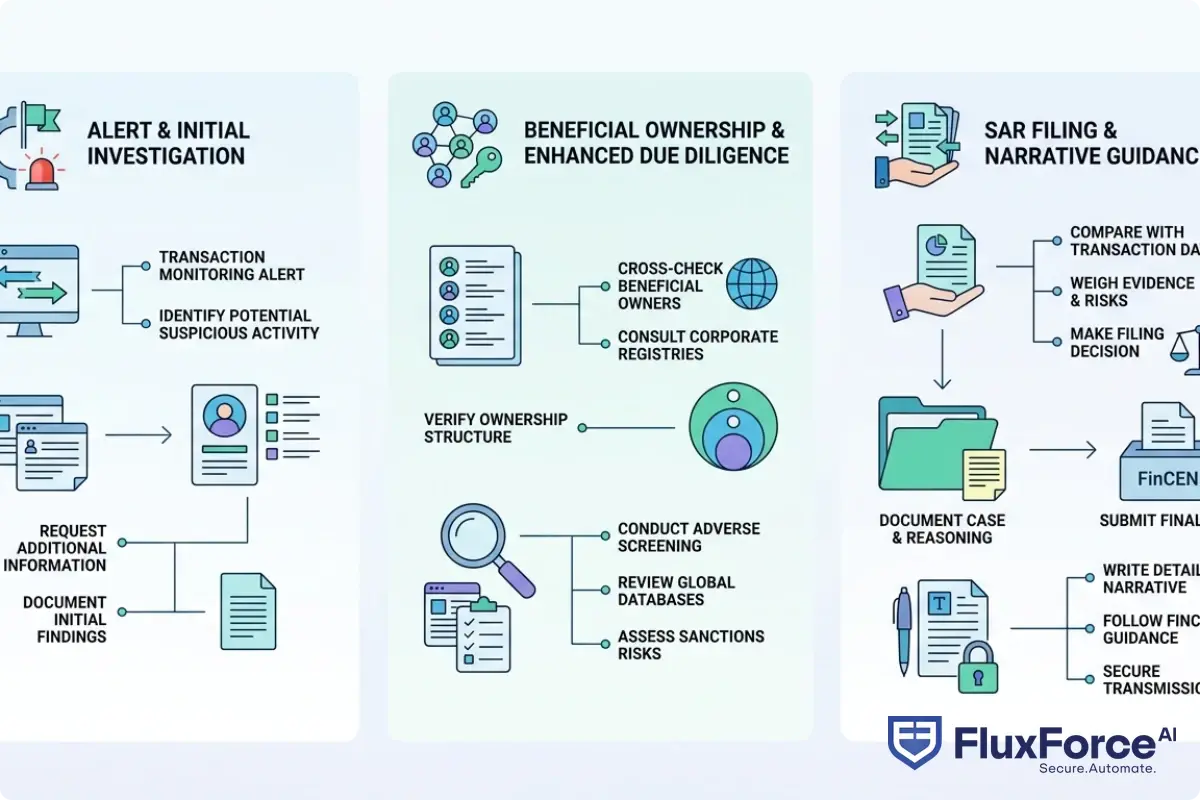

The CTA changes the analytical context for SAR decisions. When a financial institution identifies suspicious activity tied to a business customer, the beneficial ownership data now available through the CTA reporting regime can help connect that activity to the actual individuals behind the entity.

SAR Filing Best Practices for Ownership-Linked Activity

SAR filing best practices in the CTA era include one new analytical step: verify whether the involved entity has filed a BOI report and whether the reported ownership matches what you have on file. An entity registered in a state that hasn't filed a required BOI report is itself a potential red flag worth documenting in your case notes.

The sar filing requirements 2026 environment is more interconnected than it was two years ago. FinCEN's updated guidance makes clear that SARs should include beneficial ownership information when relevant to the suspicious activity being reported. If BOI on file links a suspicious account to a known bad actor or PEP, that connection belongs in the SAR narrative.

Suspicious Activity Report Guide: Connecting BOI to SAR Decisions

A practical suspicious activity report guide for compliance analysts covers not just filing mechanics but the analytical process of connecting ownership data to transaction patterns. Key questions to work through: Does the entity's reported ownership structure match its transaction behavior? Are transfers moving in ways inconsistent with the stated business purpose? Do beneficial owners appear in any adverse screening databases?

For sar filing efficiency, automated workflows that pre-populate SAR fields from transaction monitoring alerts and KYC data save analysts meaningful time per case. For context on where AI specifically helps in this process, deploying agentic AI compliance agents in 90 days is worth reviewing before you scope your automation build.

CTR filing rules haven't changed under the CTA, but BOI data adds analytical value here too. CTRs filed for cash transactions over $10,000 have a richer context layer when you can cross-reference the entity's beneficial ownership data against the individuals named in the transaction.

Anti-Money Laundering Technology for Beneficial Ownership Tracking

The gap between what the CTA requires and what legacy compliance systems can deliver is significant. Most older AML platforms were built for transaction monitoring, not entity relationship tracking. Anti-money laundering technology capable of handling the CTA needs to do both simultaneously.

Anti-Money Laundering Technology 2026: What's Changed

Anti-money laundering technology 2026 looks meaningfully different from what compliance teams were using three years ago. Three shifts stand out. First, graph-based entity resolution that models ownership hierarchies and identifies when the same individual appears as a beneficial owner across multiple distinct entities. Second, continuous monitoring rather than periodic review, with real-time alerts when ownership data changes or matches adverse events. Third, regulatory AI that understands the specific rules it enforces rather than applying generic statistical pattern detection.

The eu ai act financial services framework, now in effect for high-risk AI applications in the EU, also shapes how institutions with European operations can deploy AI in compliance decisions. Systems used for customer risk scoring and AML determinations that materially affect customers now require explainability, documented human oversight mechanisms, and ongoing accuracy monitoring to remain compliant with EU requirements.

AML Compliance Software for Automated BOI Verification

AML compliance software designed for the CTA era should support entity-level risk scoring, direct integration with identity verification providers, configurable ownership change alerts, and audit trails that satisfy both FinCEN and state examiner requirements. Platforms built specifically for this regulatory environment, rather than retrofitted from generic KYC tools, tend to handle complex multi-tier ownership structures better as your customer portfolio grows.

The comparison between manual compliance processes and AI automation is useful context for teams deciding how much to automate. For most institutions managing more than a few hundred business customers, manual BOI verification is not sustainable at any meaningful scale.

For institutions dealing with supplier or third-party risk alongside customer risk, the parallel challenges in high-risk supplier KYC/AML validation apply the same core verification principles to a different operational context.

- Beneficial ownership CTA requirements mandate that "reporting companies" file Beneficial Ownership Information (BOI) reports with the Financial Crimes Enforcement Network (FinCEN).

- For most institutions, the CTA doesn't replace existing AML compliance obligations.

- A bsa aml compliance checklist that doesn't account for CTA reporting is already outdated.

- The CTA's impact varies considerably by institution type.

- KYC automation has moved from optional to operationally necessary in the CTA era.

Onboard Customers in Seconds

Conclusion

The beneficial ownership CTA requirements represent a structural change to how corporate transparency works in U.S. financial services, not a temporary compliance project to complete and set aside. Programs that treat BOI reporting as a one-time effort rather than an ongoing operational capability will find themselves exposed when FinCEN scales up enforcement and when examiners start asking how ownership data connects to your AML decisions.

The institutions positioned to handle this well are those that invest now in aml compliance software capable of automating BOI collection and verification, integrate ownership data into SAR and CTR filing workflows, and build the kyc automation infrastructure to keep ownership records current at scale. The requirement is the same whether your team is a five-person BSA function at a community bank or a dedicated AML operations center at a major institution: know who owns your customers' businesses, verify it continuously, and use that data in your risk decisions.

For teams looking to accelerate CTA readiness, deploying regulatory compliance agents in 90 days offers a practical path to getting ownership verification workflows into production without building everything from scratch.

Share this article