.webp)

Introduction

An effective AML risk assessment guide is the first line of defense any financial institution has against money laundering, sanctions exposure, and regulatory action. Whether you run a global bank, a regional credit union, or a fintech handling payments at scale, regulators expect you to identify, document, and actively manage your money laundering risks before examiners arrive.

This guide walks through the complete process: from building your BSA/AML foundation to deploying modern aml compliance software that keeps pace with evolving threats in 2026.

- What Is an AML Risk Assessment?

- Step 1: Build Your BSA/AML Compliance Checklist

- How to Conduct Customer Risk Rating with KYC Automation

- Transaction Monitoring: SAR Filing Best Practices and CTR Filing Rules

- AML Compliance Software: What to Look for in 2026

Onboard Customers in Seconds

What Is an AML Risk Assessment?

AML risk assessment is a structured process financial institutions use to identify, measure, and mitigate the specific money laundering and terrorist financing risks they face, based on their products, customers, geographies, and delivery channels. The FFIEC BSA/AML Examination Manual describes it as the foundation of a sound AML program. Examiners use it to evaluate whether your controls actually match your risk exposure.

A well-executed assessment answers three questions:

- What risks does our business model create?

- How strong are our controls relative to those risks?

- Where do residual risks remain?

Regulatory pressure has intensified considerably. FinCEN issued more than $3.8 billion in civil money penalties across banking and fintech in 2023 alone. Examiners now expect dynamic risk assessments updated at least annually, not static documents filed and forgotten.

FinCEN issued more than $3.8 billion in civil money penalties across banking and fintech in 2023 alone.

The honest reality is that many institutions still treat risk assessments as checkbox exercises. That approach produces expensive surprises during exams, surprises that are completely avoidable.

Linking Risk Assessment to Your Broader Program

Your AML risk assessment guide should directly feed your transaction monitoring thresholds, SAR filing triggers, and customer onboarding rules. If those components are not aligned, you are running a compliance program with disconnected parts, and examiners notice that disconnect quickly.

Think of the risk assessment as the master document from which every other program element flows. When you change a product, enter a new market, or onboard a new customer segment, update the risk assessment first.

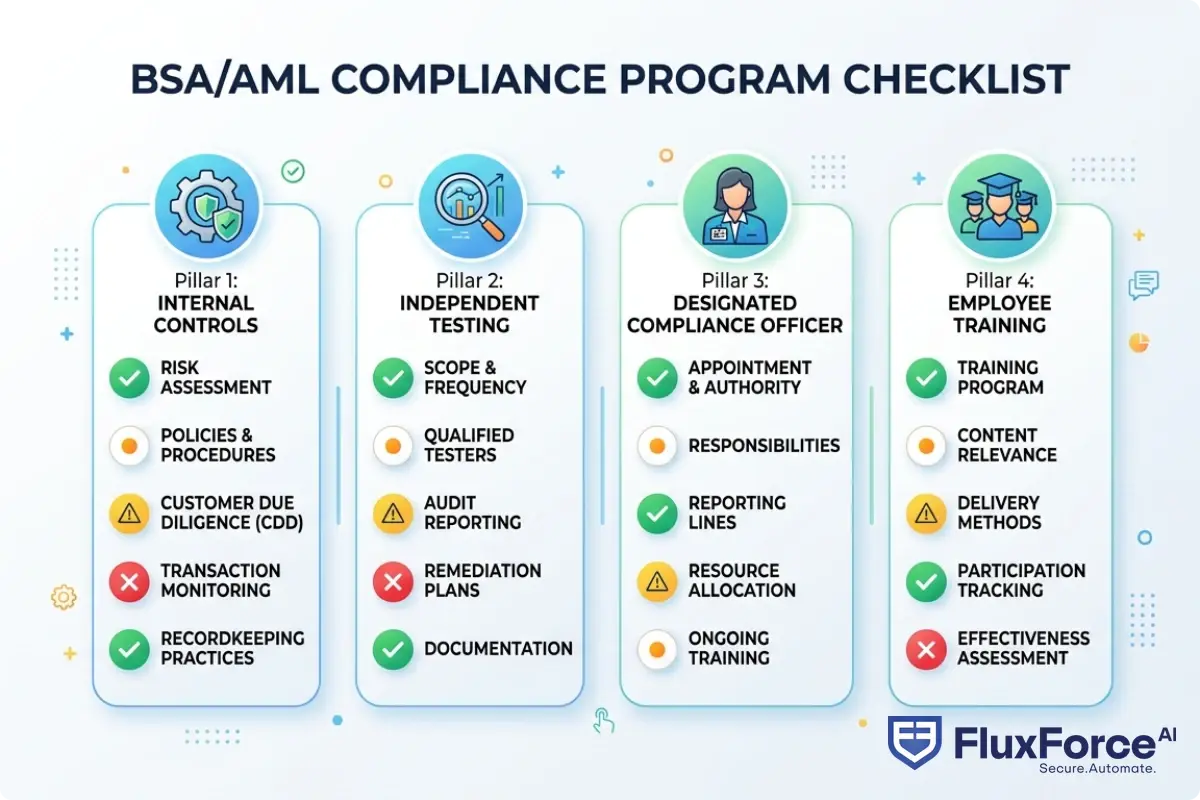

Step 1: Build Your BSA/AML Compliance Checklist

A bsa aml compliance checklist gives your team a repeatable starting point for each assessment cycle. The Bank Secrecy Act requires financial institutions to maintain written AML programs with four minimum pillars: internal controls, independent testing, a designated compliance officer, and ongoing training. Your checklist should map directly to these requirements.

The Five Core Risk Categories

Every BSA/AML compliance checklist should address five categories:

- Customer risk: Who are your customers? High-risk segments include politically exposed persons (PEPs), cash-intensive businesses, and customers in high-risk jurisdictions.

- Product and service risk: Wire transfers, prepaid cards, and correspondent banking relationships carry inherent AML exposure and are flagged consistently by regulators.

- Geographic risk: Do you serve customers or process transactions in countries on the FATF grey or black lists?

- Delivery channel risk: Digital-only onboarding and non-face-to-face account opening increase impersonation and structuring risk.

- Transaction risk: Volume, velocity, and patterns that fall outside expected behavior for a given customer profile.

Documenting your institution's formal risk appetite is a step that compliance teams often skip. It is not just about being defensible in an exam. It gives analysts a decision framework when edge cases arise. State clearly what risk levels your institution will accept and which ones require escalation to senior management.

Annual Review and Documentation Requirements

The FFIEC and FinCEN both expect your risk assessment to be a living document. That means triggering a review when you launch new products or enter new markets, updating customer risk ratings when beneficial ownership information changes, and reassessing controls after any SAR filing that reveals a systemic gap.

For AML compliance in fintech and payments operations, the documentation burden is the same as for large banks, with far fewer people to manage it. A structured checklist becomes even more critical under those conditions.

How to Conduct Customer Risk Rating with KYC Automation

KYC automation in 2026 has moved well beyond basic identity verification. Modern tools use machine learning to analyze behavioral patterns, cross-reference global watchlists in real time, and flag onboarding anomalies that human reviewers would miss at scale.

KYC and CDD Requirements for Banks

The kyc cdd requirements banks face are set out in FinCEN's Customer Due Diligence Rule, which requires financial institutions to collect and verify customer identity, beneficial ownership for legal entities (anyone owning 25% or more), the nature and purpose of the customer relationship, and ongoing monitoring to detect suspicious activity.

CDD is the baseline. For customers flagged as high-risk during onboarding or ongoing monitoring, the rules require considerably deeper investigation before and after account opening.

Automating Identity Verification in 2026

KYC automation 2026 tools deliver measurable value at scale. Some institutions report 60-70% reductions in manual review hours after deploying automated ID verification and watchlist screening. For a large bank processing tens of thousands of onboarding requests monthly, that math is compelling. For a fintech BSA AML small team, automation is not optional. It is the only way to keep pace with volume without adding headcount.

Some institutions report 60-70% reductions in manual review hours after deploying automated ID verification and watchlist screening.

Tools worth evaluating include document verification APIs that return confidence scores, liveness detection to prevent deepfake onboarding attempts, and perpetual KYC approaches that monitor customer data continuously rather than running periodic batch reviews. When a customer is flagged for enhanced review, the system should generate a pre-populated case file that reduces analyst prep time significantly.

The KYC and AML identity verification strategy used by insurance claims operations shows how this tiered escalation logic applies across financial service verticals beyond banking.

Transaction Monitoring: SAR Filing Best Practices and CTR Filing Rules

This is where the AML risk assessment guide moves from documentation to daily operations. Your monitoring thresholds, alert logic, and escalation procedures are the practical expression of everything you documented in your risk assessment.

SAR Filing Requirements in 2026

SAR filing requirements 2026 remain governed by FinCEN regulations. Mandatory 30-day filing deadlines apply, extendable to 60 days when no suspect is identified. A solid suspicious activity report guide should cover several points that compliance teams frequently misapply:

- SARs are required when a transaction involves $5,000 or more and the institution knows, suspects, or has reason to suspect it involves illegal activity.

- Continuing suspicious activity requires follow-up SARs every 90 days.

- Structuring, deliberately breaking transactions into sub-$10,000 amounts, must be reported even when the underlying transaction appears legal.

SAR filing efficiency is a real operational challenge. Large banks generate thousands of alerts per month, but conversion rates from alert to filed SAR often run below 5-10%. That gap is almost entirely false positives, representing enormous wasted analyst time.

Agentic AI fraud agents have demonstrated 80% reductions in false positives in production environments by contextualizing alerts against historical behavior, peer group analysis, and entity network relationships, rather than applying static rule thresholds alone.

Agentic AI fraud agents have demonstrated 80% reductions in false positives in production environments by contextualizing alerts against historical behavior, peer group analysis, and entity network relationships, rather than applying static rule thresholds alone.

SAR filing best practices include using narrative templates that satisfy FinCEN's five-W standard (Who, What, When, Where, Why), maintaining a SAR case management log for trend analysis, and conducting post-filing reviews to identify pattern-level systemic risks.

CTR Filing Rules You Must Know

CTR filing rules require a Currency Transaction Report for any cash transaction exceeding $10,000, including multiple transactions that aggregate above $10,000 in a single day with the same customer. Phase-in exemptions for certain business types are valid, but they must be documented and reviewed annually. Letting exemptions lapse without renewal is a common exam finding, and it is entirely avoidable with calendar-based review processes.

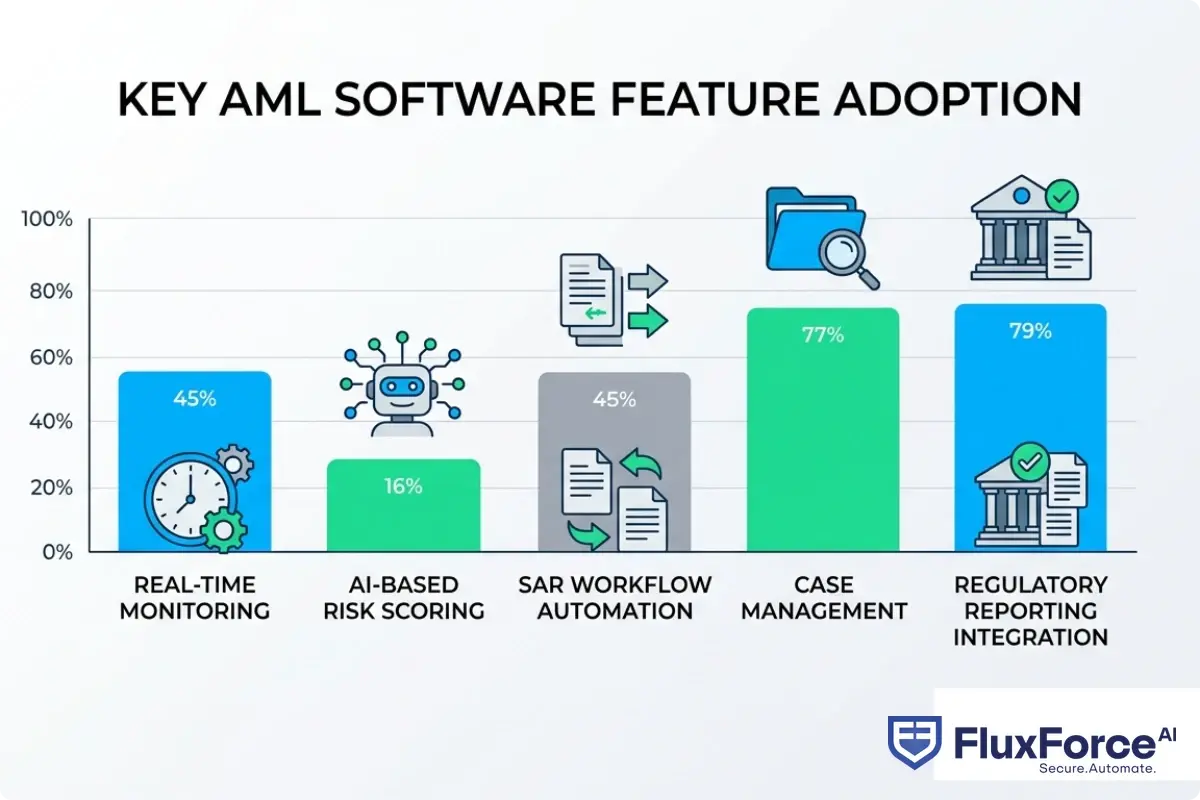

AML Compliance Software: What to Look for in 2026

The right aml compliance software integrates transaction monitoring, case management, SAR filing automation, and regulatory reporting in a single platform. Buying four separate point solutions that do not share data creates exactly the kind of fragmentation that produces compliance gaps.

Core Features to Evaluate

When assessing anti money laundering technology for your institution, prioritize:

- Real-time transaction screening: Batch-based monitoring misses fast-moving schemes. Real-time processing is the baseline expectation now, not a premium feature.

- AI-based risk scoring: Static rule engines generate excessive false positives. Machine learning models trained on your own transaction history outperform generic rule sets by a significant margin.

- SAR case management: From alert to narrative to filing should be a single workflow, not three separate systems with manual data transfer between them.

- Audit trail and explainability: You must be able to show examiners exactly why an alert was generated and how analysts reached their resolution decision.

- API integration: Your AML compliance software needs to connect with your core banking system, onboarding platform, and external data providers without requiring custom development for each connection.

Anti-Money Laundering Technology Trends in 2026

Anti money laundering technology 2026 is moving in three directions: network analytics that map relationships between entities rather than analyzing transactions in isolation; behavioral biometrics for real-time anomaly detection during digital sessions; and federated learning models that allow institutions to collaborate on model training without sharing raw transaction data.

The eu ai act financial services provisions, which began phasing in during 2025, add a compliance dimension to AI adoption. High-risk AI systems used in AML contexts must meet transparency and human oversight requirements, a consideration that should factor into your software selection process if you operate in or serve EU markets.

The tradeoffs between manual compliance and AI automation are worth working through carefully before committing to a technology direction.

Enhanced Due Diligence for High-Risk Customers

The enhanced due diligence guide most institutions rely on draws directly from FATF Recommendation 19 and FinCEN's CDD Rule. EDD is not just more paperwork. It is a materially deeper investigation into source of funds, business purpose, and expected transaction activity.

What Triggers an EDD Review

EDD is required, not optional, for these customer categories:

- Politically Exposed Persons (PEPs) and their immediate family members

- Correspondent banking relationships with foreign financial institutions

- Private banking clients managing substantial assets for high-net-worth individuals

- Customers flagged during ongoing monitoring for unexplained changes in activity patterns

- Any customer whose jurisdiction appears on the FATF list of high-risk and other monitored jurisdictions

The Enhanced Due Diligence Process, Step by Step

- Collect and verify source of wealth documentation: tax returns, business ownership records, investment account statements.

- Obtain management or board-level approval before onboarding or continuing the relationship.

- Set enhanced monitoring parameters with lower alert thresholds and shorter review intervals.

- Document the rationale for proceeding in writing. Noting that you completed EDD is not sufficient. The conclusion must be risk-based and specific.

- Schedule an annual review, or more frequently if new risk indicators emerge.

AML Compliance for Fintech and Community Banks

AML compliance fintech and community bank compliance share a common challenge: lean teams managing significant regulatory obligations. BSA/AML compliance community banks face roughly the same program requirements as large institutions, with a fraction of the staff and budget.

BSA/AML for Community Banks and Small Institutions

Community banks often struggle with three specific gaps: inadequate transaction monitoring thresholds calibrated for their actual customer base, over-reliance on vendor rule sets built for larger institutions, and limited access to the data analytics talent that bigger banks hire in-house.

The fix is not always more technology. It is right-sized technology. An institution with 15,000 customers should not run the same monitoring configuration as one with two million. Thresholds, peer groups, and escalation triggers all need to reflect your actual risk profile, not a generic template.

How Small Fintech Teams Handle BSA/AML Compliance

Fintech BSA AML small team operations succeed when they automate the high-volume, low-judgment tasks: ID verification, watchlist screening, CTR preparation. This frees human review capacity for the narrow slice of alerts that genuinely require analyst judgment.

Regulatory change management is another area where small teams get caught short. Build a process for monitoring FinCEN guidance updates, FFIEC examination procedure revisions, and state-level regulatory changes. A compliance calendar with formal review dates prevents the scramble that happens when teams learn about updates from exam findings rather than proactive tracking.

AML risk checks in insurance policy issuance illustrate how this operational discipline translates across financial services verticals, including non-bank financial institutions with similar BSA obligations.

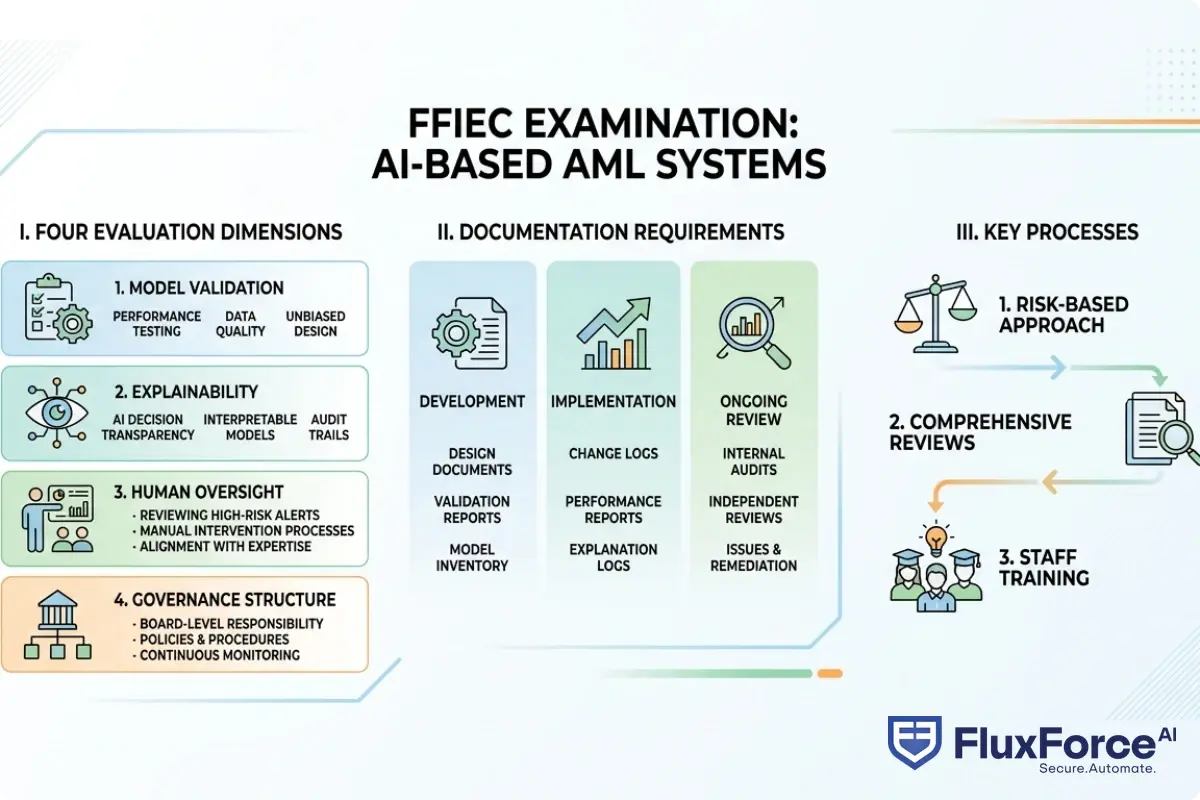

How FFIEC Examiners Evaluate AI-Driven AML Systems

As AI-driven monitoring becomes standard practice, the FFIEC's examination approach has adapted accordingly. Interagency guidance on model risk management sets out expectations that directly affect how institutions should deploy and document their AML models.

FFIEC Exam AI Systems Review

FFIEC exam ai systems reviews focus on four areas:

- Model validation: Has an independent party validated the model's inputs, logic, and outputs against historical data? Validation should be documented and repeated when the model is retrained or significantly updated.

- Explainability: Can your compliance team explain to an examiner, in plain language, why a specific transaction generated an alert? Black-box outputs are increasingly unacceptable to examiners.

- Human oversight: Are there documented procedures for human review of AI-generated decisions? Fully automated SAR filing without human review is not an acceptable configuration under current guidance.

- Governance: Who owns the model? Who approves changes? Is there a model inventory? These governance structures must exist before an exam, not be assembled during one.

Institutions that can answer all four questions with documentation in hand tend to pass AI-related exam scrutiny without findings.

EU AI Act and Financial Services Implications

The eu ai act financial services provisions have direct AML implications. Transaction monitoring systems used for risk scoring may qualify as high-risk AI under the Act's classification framework. If your institution operates in or serves EU markets, that triggers requirements for conformity assessments, technical documentation, and mandatory human oversight provisions.

These requirements align reasonably well with what the FFIEC already expects from US institutions, but they add specific documentation burdens that go beyond existing US guidance. Coordinating your AML AI governance framework across both regulatory regimes now is considerably easier than retrofitting compliance after an enforcement action.

- AML risk assessment is a structured process financial institutions use to identify, measure, and mitigate the specific money laundering and terrorist financing risks they face, based on their products, customers, geographies, and delivery channels.

- A bsa aml compliance checklist gives your team a repeatable starting point for each assessment cycle.

- KYC automation in 2026 has moved well beyond basic identity verification.

- This is where the AML risk assessment guide moves from documentation to daily operations.

- The right aml compliance software integrates transaction monitoring, case management, SAR filing automation, and regulatory reporting in a single platform.

Onboard Customers in Seconds

Conclusion

A complete AML risk assessment guide is not a document you file annually and revisit only when examiners call. It is an operational framework that continuously informs your customer risk ratings, transaction monitoring thresholds, SAR filing decisions, and technology investments.

The institutions that manage aml compliance well share a few traits: they treat risk assessment as a living process, they use aml compliance software to automate what does not require human judgment, and they invest in explainable AI systems that can survive regulatory scrutiny. For fintech teams and community banks, the path forward involves choosing right-sized tools, not building a compliance organization that mirrors a large bank's headcount.

If your current AML program feels like it is reacting to the last examination rather than preparing for the next one, start with a fresh risk assessment that maps your actual risk profile honestly and drives every downstream control decision from there.

Share this article