.webp)

Introduction

SAR filing efficiency is the metric most compliance teams never track until they're buried under a backlog. If your analysts are spending 4-6 hours per suspicious activity report, manually pulling transaction data, writing narratives from scratch, and waiting on manager reviews, the problem isn't effort. It's process design.

The average mid-sized bank files between 200 and 500 SARs per year. Large institutions file tens of thousands. At 5 hours per SAR (a commonly cited benchmark in BSA examiner discussions), that's 1,000 to 2,500 analyst-hours annually at mid-sized institutions alone, before accounting for the 30-day filing deadline pressure that forces teams into reactive mode every month.

This post is for compliance officers, BSA officers, and AML program leads who want to understand where the bottleneck actually lives and what realistic improvements look like in 2026. We'll cover the structural issues in most SAR workflows, what AML compliance software can and can't solve, and how to think about this problem differently.

- Why SAR Filing Efficiency Breaks Down

- What the Numbers Actually Show

- The Five Bottlenecks Compliance Teams Miss

- How AML Compliance Software Changes the Equation for SAR Filing Efficiency

- SAR Filing Efficiency in Community Banks vs. Fintechs

Onboard Customers in Seconds

Why SAR Filing Efficiency Breaks Down

The honest answer is that SAR workflows were designed for a different volume. When a community bank filed 20 SARs a year, manual case management worked fine. Today, transaction volumes have multiplied, typologies have grown more complex, and regulators expect more detailed narratives. The workflow hasn't kept pace.

The Manual Review Trap

Most compliance teams still rely on alert queues that mix genuine suspicious activity with noise. Analysts spend a significant portion of their time on alerts that never become SARs. According to FinCEN's SAR Activity Review publications, the quality of SAR narratives has become a growing focus area for examiners, which means analysts now face dual pressure: move faster and write better.

The result is that skilled analysts spend their sharpest hours triaging false positives, leaving less cognitive energy for the SARs that actually matter.

Alert Fatigue Is Real

This isn't a soft HR problem. Alert fatigue in AML compliance has measurable consequences. When analysts review 50-100 alerts a day, pattern recognition degrades. The 47th alert of the afternoon gets less scrutiny than the third one of the morning. The FFIEC BSA/AML Examination Manual consistently identifies over-reliance on rule-based triggers as a root cause of inflated alert volumes and poor case quality.

The fix isn't asking analysts to work harder. It's reducing the irrelevant alert volume before it reaches them.

What the Numbers Actually Show

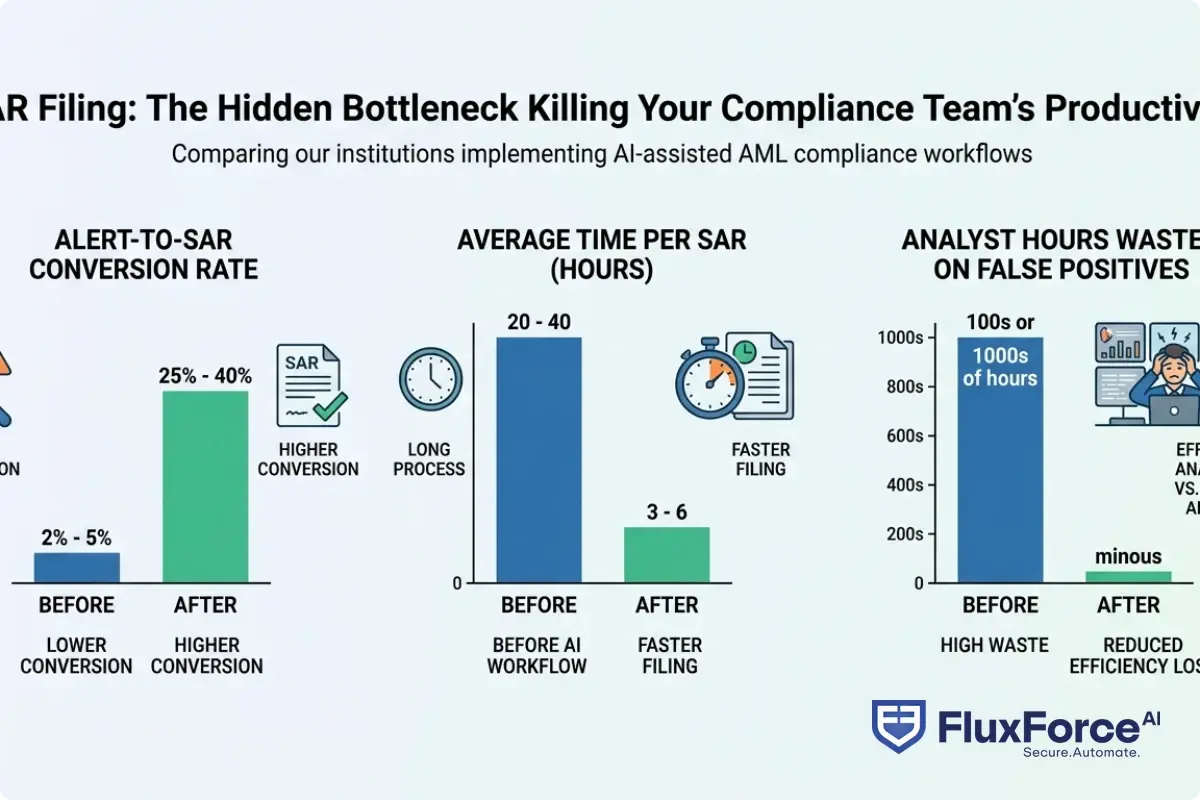

Let's get specific. Across institutions that have moved to AI-assisted AML workflows, the reduction in time-per-SAR typically falls in the 40-60% range. That's not a vendor projection. It's the result of removing three specific steps from the manual workflow: data aggregation, narrative drafting, and duplicate alert suppression.

Across institutions that have moved to AI-assisted AML workflows, the reduction in time-per-SAR typically falls in the 40-60% range.

A compliance team that files 300 SARs a year and saves 2.5 hours per SAR gets back roughly 750 analyst-hours annually. At a loaded labor cost of $80-120 per hour for a senior BSA analyst, that's $60,000-$90,000 in recovered capacity per year, before accounting for overtime costs, contractor support, or the regulatory risk of late filings.

The SAR filing deadline is 30 calendar days from the date the decision to file is made, with a 60-day extension available but not guaranteed. When teams are under pressure, quality drops. When quality drops, examiners notice.

The Five Bottlenecks Compliance Teams Miss

Most compliance managers focus on the obvious problems: not enough staff, too many alerts. The structural bottlenecks are subtler and harder to fix without intentional process redesign.

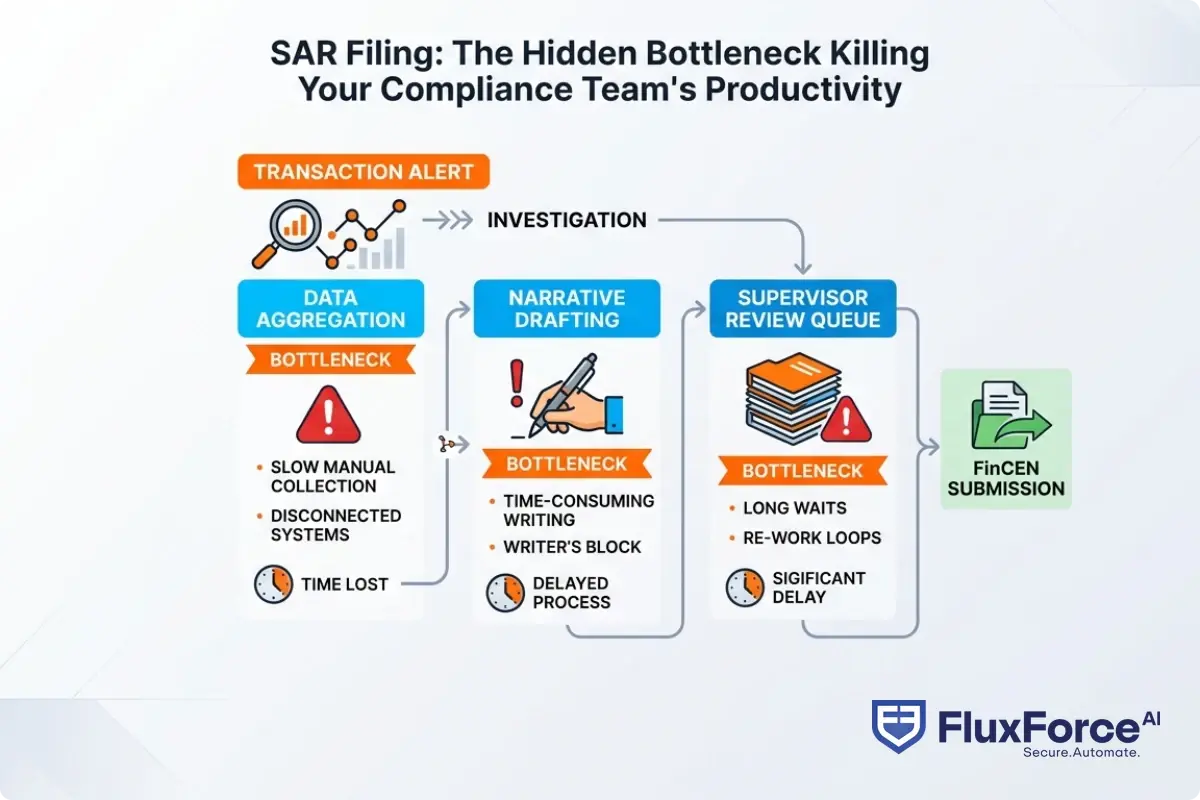

1. Fragmented data sources. SAR narratives require pulling data from transaction systems, core banking platforms, CRM tools, and sometimes external watchlist databases. When analysts switch between five systems per case, time evaporates. Teams managing CTR filing rules alongside SARs face compounded pressure: currency transaction reports carry their own 15-day deadline and different data requirements, creating two parallel data-pull workflows running simultaneously.

2. Unstructured narrative drafting. Every SAR needs a narrative explaining the suspicious behavior in plain language. Many teams start from a blank page. Templates exist, but they're generic. AI-assisted narrative drafting, trained on institution-specific filing history, can cut this step from 90 minutes to under 20.

3. Supervisor review queues. SARs require sign-off before filing. When supervisors are managing their own caseloads, review queues back up. This alone accounts for 20-30% of total cycle time at many institutions, and it's the bottleneck least likely to appear in any formal process map.

This alone accounts for 20-30% of total cycle time at many institutions, and it's the bottleneck least likely to appear in any formal process map.

4. Duplicate case detection failures. If the same subject triggers alerts in different months, teams often recreate case files rather than linking to prior SARs. This wastes investigation time and creates documentation risk during examinations.

5. Post-filing tracking gaps. After a SAR is filed, teams frequently lose visibility into whether a related case was filed, whether law enforcement responded, or whether the subject triggered new alerts in the following quarter. This breaks the continuity of suspicious activity monitoring that regulators expect.

How AML Compliance Software Changes the Equation for SAR Filing Efficiency

Good AML compliance software doesn't just automate alerts. It changes the structure of the workflow. The distinction matters because many institutions buy compliance software and then layer it on top of existing manual processes. That approach delivers disappointingly little.

The right sequence is workflow redesign first, software second. Technology should map to an intentional process, not replace a broken one with an automated version of the same thing.

What actually works in 2026:

- Unified case management. All relevant data (transactions, counterparty info, prior SARs, external watchlist hits) in one interface. Analysts stop toggling between systems.

- AI-assisted narrative generation. The system drafts a narrative based on case data. The analyst edits and approves. Not the other way around.

- Smart alert clustering. Related alerts on the same subject, account, or network are grouped before they reach the analyst. This reduces duplicate effort in a meaningful, measurable way.

- Built-in audit trails. Every decision is logged automatically. This reduces the documentation burden while improving readiness for examinations.

For a deeper look at how AML screening fits into broader risk frameworks, the post on AML screening in digital lending covers how payment risk teams are structuring their AML workflows to handle higher transaction volumes without proportionally expanding headcount.

SAR Filing Efficiency in Community Banks vs. Fintechs

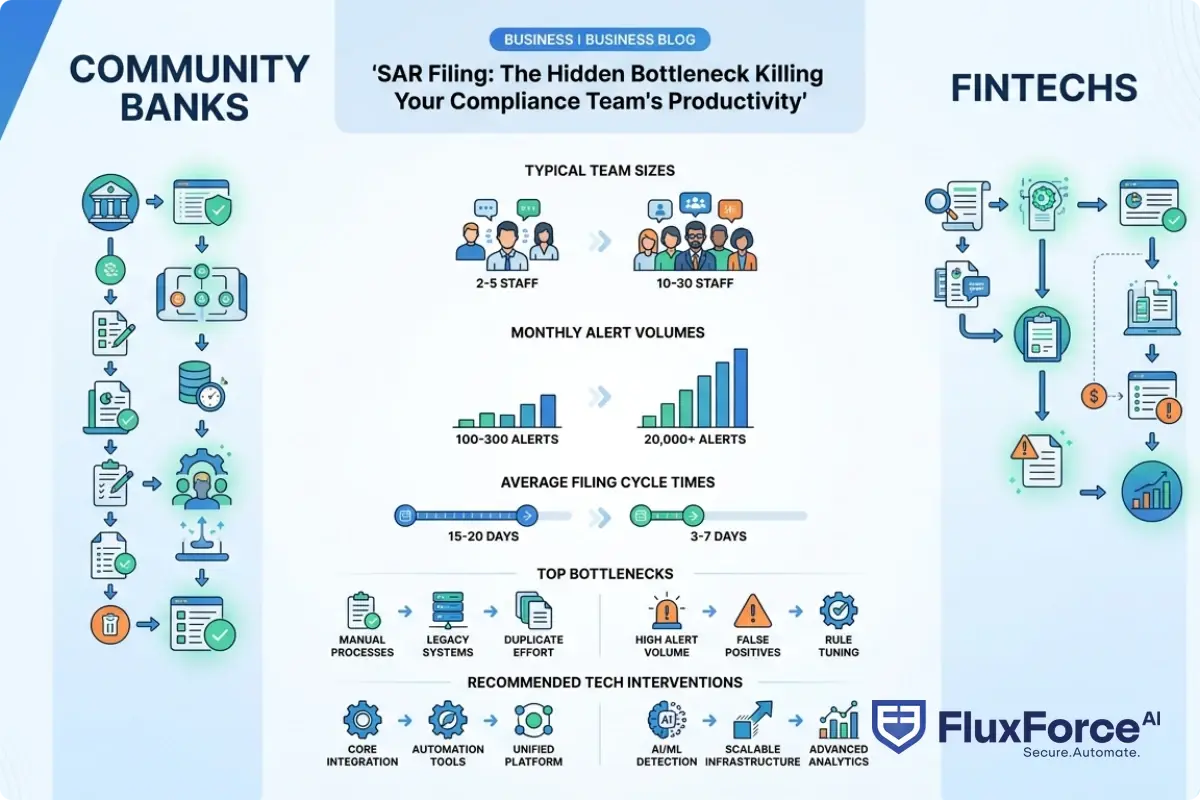

The problem looks different depending on where you sit. Community banks and fintechs both struggle with SAR filing efficiency, but the root causes differ enough that the solutions do too.

Community banks often have dedicated BSA officers managing the full AML program with a small team. The BSA/AML regulatory framework applies equally to a $500 million community bank as to a $500 billion institution, but the resources don't scale the same way. Community banks face the same filing requirements with a fraction of the technology budget. This is where purpose-built, right-sized aml compliance software matters most. Teams of 2-5 compliance professionals can't afford to spend 40% of their time on data aggregation tasks that software should handle automatically.

Fintechs face a different pressure. High transaction volumes, younger customer bases, and real-time payment rails mean alert volumes can spike fast. A BSA AML small team at a fintech might handle 3x the alert volume of a similarly-sized community bank because the transaction patterns are fundamentally different. The challenge is often immature processes, not lack of technology. Many fintechs have purchased sophisticated tools but haven't built the compliance operating procedures to use them effectively.

Both groups benefit from the same fundamental fix: reducing alert noise before it reaches analysts, and giving analysts better tools for the cases that deserve their full attention.

For compliance teams in insurance and adjacent regulated industries dealing with similar KYC and AML pressures, the AML risk checks in policy issuance strategy guide covers how verification workflows operate across different regulatory contexts with similarly constrained team sizes.

KYC Automation and Its Role in SAR Volume

Here's a counterintuitive point: better KYC at onboarding reduces SAR volume downstream. When you know more about a customer at the point of account opening, you calibrate their expected transaction behavior more accurately. Fewer deviations from expected behavior means fewer false positive alerts, which means fewer wasted analyst hours across the SAR filing process.

KYC automation in 2026 goes beyond identity verification. It includes behavioral baseline modeling, enhanced due diligence for higher-risk customers, and continuous monitoring that updates risk scores as customer activity evolves. When a customer's risk profile shifts, the system flags it, rather than waiting for a rule-based alert to trigger six months later when the pattern has already expanded.

This doesn't eliminate SARs. Genuinely suspicious activity should still be reported, and the threshold for filing hasn't changed. But it concentrates analyst attention on cases that are actually suspicious, rather than spreading it across a mix of real and phantom alerts.

The relationship between kyc compliance software and SAR filing efficiency is direct: better data in means better decisions out. Teams that have integrated KYC automation with their case management systems consistently report lower false positive rates, typically in the 20-35% reduction range for institutions moving from rule-only to hybrid ML/rule approaches.

Teams that have integrated KYC automation with their case management systems consistently report lower false positive rates, typically in the 20-35% reduction range for institutions moving from rule-only to hybrid ML/rule approaches.

Sanctions screening is a related layer. When sanctions screening is automated and integrated with the alert queue, analysts don't have to manually check OFAC lists per case. That's another 15-20 minutes per SAR recovered. The sanctions screening automation guide covers how CISOs are integrating this into their broader compliance architecture without creating parallel workflows.

Building a BSA AML Compliance Checklist That Supports SAR Efficiency

A checklist won't solve a structural problem, but a well-designed one prevents the small errors that slow individual SARs down and accumulate into significant cycle time losses. Here's what a working BSA AML compliance checklist for SAR filing should include:

- Alert disposition documented before case is opened (reason for escalation, not just alert ID)

- Subject research complete (prior SARs on file, watchlist status, full account history, related party review)

- Transaction data pulled from all relevant accounts and relevant timeframes

- Narrative draft reviewed against FinCEN SAR instruction guidance on a field-by-field basis

- Supporting documentation attached (screenshots, transaction ledgers, source data files)

- Supervisor review scheduled with expected turnaround time noted in the case file

- Filing deadline tracked against investigation open date, with escalation trigger if deadline is within 5 days

- Post-filing entry made in case management system, with continuing activity flag if warranted

The problem isn't that compliance teams don't know these steps. It's that they're not systematically enforced because there's no workflow tool making them mandatory gates before the case advances. The difference between a team that averages 18 days per SAR and one that averages 28 days is usually found in steps 3, 6, and 7.

For teams building broader compliance automation programs, the comparison of manual compliance versus AI automation approaches is worth working through before making tooling decisions, particularly for institutions that are uncertain whether their process maturity is ready for automation.

What SAR Filing Efficiency Looks Like in Practice

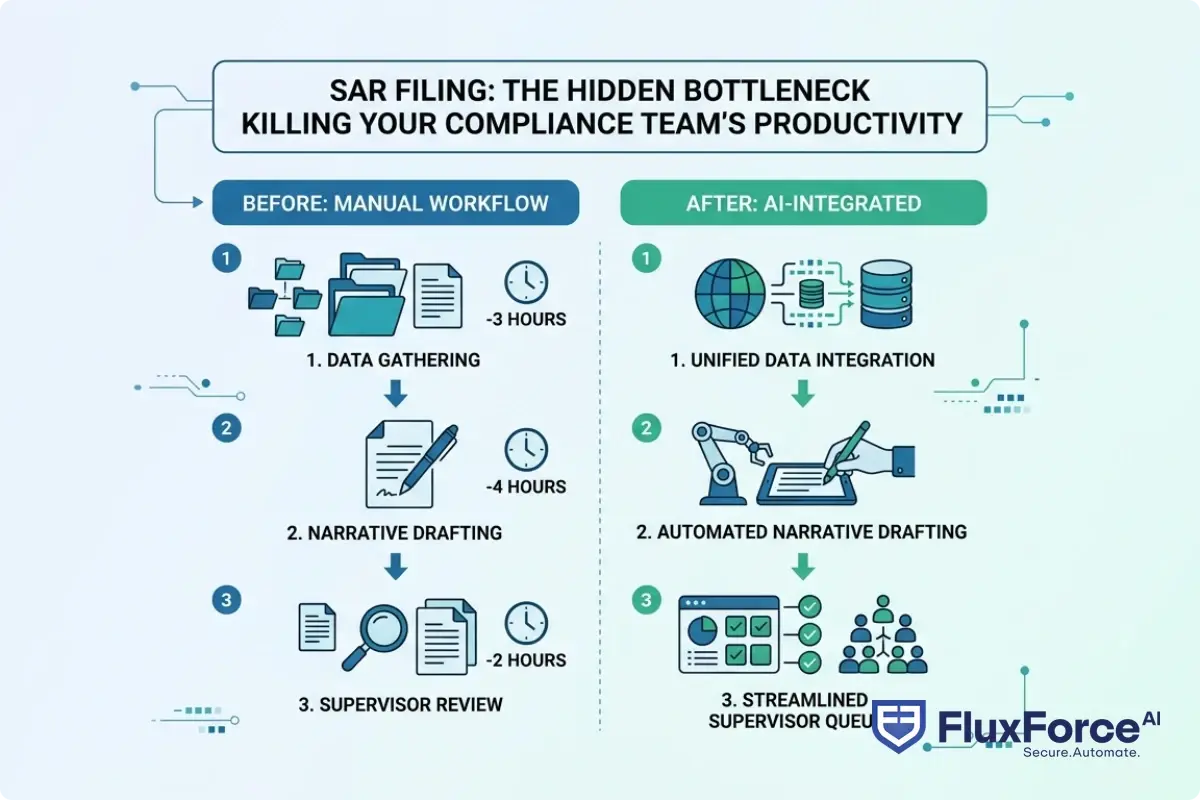

A regional bank with $8 billion in assets and a compliance team of 12, including 4 analysts dedicated to SAR filing, reduced its average time-per-SAR from 6.2 hours to 2.8 hours over 18 months. They made three targeted changes rather than overhauling everything at once.

First, they integrated their transaction monitoring system directly with their case management platform. Data aggregation became automatic. Analysts no longer pulled reports manually from three separate systems before they could even begin reviewing a case.

Second, they implemented AI-assisted narrative drafting. The tool pre-populated narratives using prior filed SARs for similar typologies, which analysts then reviewed and edited. Average narrative time dropped from 85 minutes to 22 minutes. The quality of narratives, measured by examiner feedback in the following cycle, improved.

Third, they created a dedicated supervisor review queue with defined SLA targets. Reviews were completed within 24 hours in 94% of cases, down from an average wait time of 4.2 days previously.

The cycle time reduction freed approximately 850 analyst-hours annually. They reinvested those hours into proactive enhanced due diligence reviews and typology analysis, both areas that had been chronically underfunded due to SAR backlog pressure. That's the real payoff of SAR filing efficiency: not fewer SARs filed, but more accurate ones filed faster, with analyst capacity redirected toward higher-value AML work.

For teams dealing with fraud that sits adjacent to AML typologies, the analysis of how agentic AI cuts false positives by 80% shows how similar workflow logic applies in fraud detection contexts where alert volume and analyst fatigue create the same capacity constraints.

- The honest answer is that SAR workflows were designed for a different volume.

- Most compliance managers focus on the obvious problems: not enough staff, too many alerts.

- Good AML compliance software doesn't just automate alerts.

- The problem looks different depending on where you sit.

- Here's a counterintuitive point: better KYC at onboarding reduces SAR volume downstream.

Onboard Customers in Seconds

Conclusion

SAR filing efficiency isn't a staffing problem or a pure regulatory problem. It's a workflow design problem, and it's one that can be addressed methodically without waiting for a budget cycle or a regulatory examination to force the issue. The teams making the biggest gains share a common pattern: they mapped their actual process, identified exactly where time was lost, and selected technology to close those specific gaps.

If your compliance team is averaging 5-7 days per SAR end-to-end, you're performing reasonably. If you're at 15-30 days, there's a structural issue that more headcount won't fix. Start with the bottleneck: alert noise, data fragmentation, narrative drafting, supervisor queues. Each requires a different intervention.

AML compliance demands are increasing in 2026, not leveling off. The institutions that get SAR filing efficiency right now are building compliance infrastructure that scales with transaction volume. Those that don't will be managing the same capacity crisis with a larger team each year. The time to redesign the workflow is before the next examination cycle, not during it.

Share this article