.webp)

Listen to our podcast 🎧

Introduction

Loan teams in digital lending spend up to 70% of their time gathering and entering data from bank statements, tax returns, and financial documents . Different formats, missing pages, and mismatched numbers turn what should be a quick review into a long and frustrating process. By the time underwriters finally finish, borrowers may have lost patience or moved to faster digital lending platforms.

Doing everything manually slows down the entire digital loan approval process. Add in strict regulatory requirements and the pressure only grows. Every document, calculation, and decision needs a clear audit trail to meet standards like the NAIC Financial Analysis Handbook and Federal Reserve guidance. Manual systems simply cannot keep up with the scale of modern financial technology and digital lending demands.

The Compliance Challenge

Staying compliant is all about protecting the bank’s reputation and making safe lending choices. Traditional tools such as OCR or spreadsheet macros can copy numbers from documents but they do not understand the meaning behind the data, cannot adapt to new formats, and often miss unusual patterns that hint at automated risk assessment gaps.

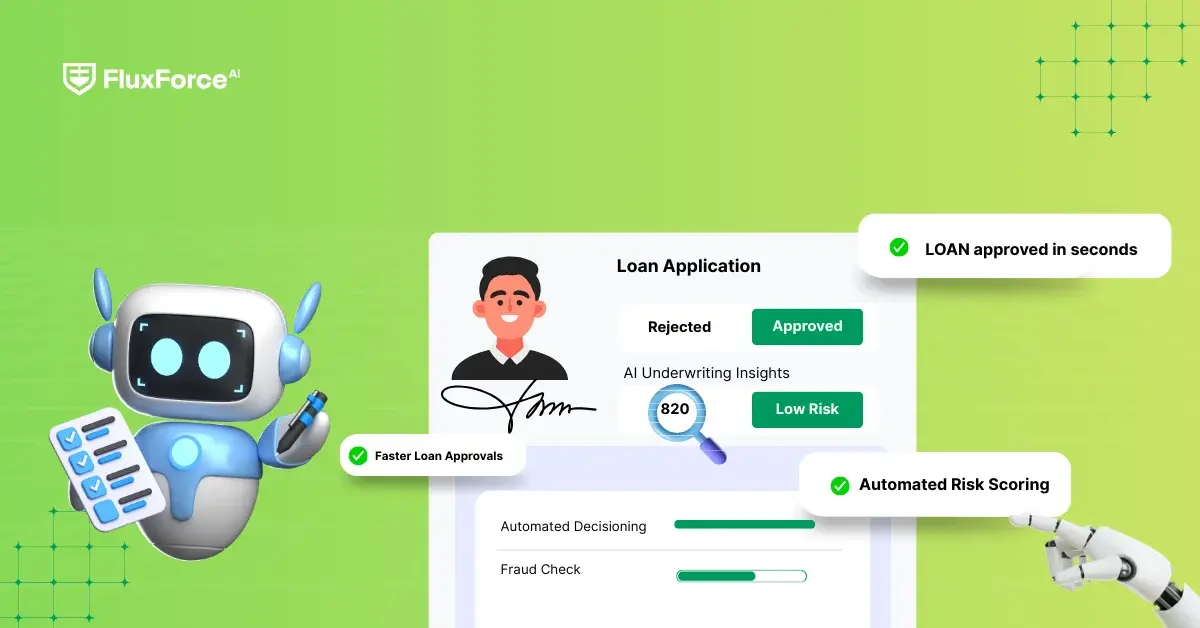

Enter AI Underwriting Agents

This is where AI underwriting agents in digital lending come in. These AI systems can automatically read thousands of financial documents, extract key data, calculate metrics like debt-service coverage ratio (DSCR), and support AI underwriting decisions in minutes instead of days. No more endless spreadsheets and no more chasing missing pages. Underwriters can spend their time on high-value tasks such as assessing management quality, market trends, and competitive positioning.

Scaling Lending the Smart Way

Automating these tasks through loan automation does more than save time. AI ensures data is consistent and accurate, helping teams detect risk factors 38% earlier than manual processes. With cleaner, standardized data, banks can track portfolio health, monitor covenants, and spot early warning signs faster.

Most importantly, AI allows banks to scale digital lending platforms and handle more deals without hiring additional staff. Loan teams can scale their operations while maintaining high standards for credit decisions.

Now we will explore how AI transforms each step of digital lending, showing exactly what changes when automation takes over.

How AI Changes the Loan Process Step by Step

.webp?width=1200&height=800&name=High-Impact%20Use%20Cases%20of%20AI%20Underwriting%20Agents%20in%20Banking%20(2).webp)

Faster Data Collection

The first big shift in digital lending with AI underwriting agents happens during data collection. Instead of staff spending hours sorting through tax returns, bank statements, and payroll records, AI can scan thousands of documents in minutes for faster digital loan approval. It pulls key figures, detects missing sections, and flags inconsistencies in real time. Research shows that AI-driven data intake can reduce document processing time by up to 80% compared to manual handling in financial technology systems.

Smarter Risk Assessment

Once the data is captured, automated risk assessment tools for digital loans take over. These tools use models trained on large financial histories to evaluate patterns humans often miss. They can measure creditworthiness more consistently, improving the reliability of credit scoring AI. A McKinsey study found that lenders using AI-based scoring models cut default rates by 10–15% while increasing approval rates for qualified borrowers.

Consistent Credit Evaluation

Traditional underwriters may reach different conclusions when reviewing similar applications in digital lending. With AI credit scoring and AI credit evaluation, the process becomes more uniform. The same factors are assessed the same way, every time. For banks, this translates into stronger compliance, reduced security risks, and less regulatory risk. For borrowers, it means a fairer process with fewer human biases in AI-driven credit evaluation.

Automated Loan Approval

With structured data and reliable scoring, the next stage is digital loan approval. AI can instantly generate a decision recommendation with supporting analysis for underwriters, improving loan automation efficiency. Some lending platforms are already approving small business loans in under 24 hours, compared to weeks under manual systems. This speed not only attracts borrowers but also helps banks compete in the crowded digital lending space.

Scaling Without Extra Staff

Perhaps the strongest benefit of AI underwriting is its impact on scalability. Manual teams often hit a ceiling, limited by staff hours, error rates, and manual risk management constraints. By using machine learning lending models and automated risk management systems, banks can process far more applications with the same number of employees.

Deloitte reports that institutions using AI-driven underwriting can handle up to 50% more loans per year without increasing headcount.

Faster processing, consistent scoring, and better automated risk management give lenders a direct path to growth. Banks can serve more customers, lower operational costs, and maintain compliance in financial technology ecosystems. For borrowers, faster and fairer approvals build trust in digital lending platforms, which boosts adoption.

High-Impact Use Cases of AI Underwriting Agents in Banking

Traditional underwriting was designed for a slower world. Today’s financial sector requires real-time decision-making, but manual teams struggle to keep up. This is where AI underwriting agents in digital lending prove their worth, not only by accelerating approvals but by supporting broader loan automation across lending operations. Here are some use cases that show how banks are scaling smarter with these agents.

Fraud and Compliance

Fraudulent loan applications and compliance failures in digital lending cost banks billions each year. AI underwriting agents bring precision by spotting unusual behavior across documents and transactions. Unlike static systems, they keep learning as new fraud patterns emerge.

- McKinsey reported that AI-driven fraud detection in digital lending platforms cut false positives by 50%, reducing delays for genuine borrowers.

- ING used AI for KYC and AML automation in financial technology systems, cutting onboarding time by 90% while lowering staff workload by 30%.

This means lenders can approve loans faster without compromising on trust or regulation.

Fair Credit Access

Conventional credit scoring leaves out many people and small businesses who lack long credit histories. AI underwriting agents widen the lens by analyzing digital spending habits, e-commerce records, and even utility payments.

- Upstart shared that its AI credit evaluation approved 27% more borrowers than traditional models, with no increase in default risk.

- Fintech firms in the UK reduced AI underwriting time from 3 days to just 30 minutes, while boosting approval rates for SMEs by 20%.

By bringing in richer data, AI agents make digital lending more inclusive while protecting lenders through automated risk assessment.

Customer-Centric Banking

The power of AI underwriting agents in digital lending goes beyond approving or rejecting loans. They continue to work behind the scenes after disbursement, monitoring repayments and alerting banks to early warning signals.

- Automated risk monitoring agents can flag weakening cash flows or missed micro-payments before defaults occur using automated risk management tools, giving banks time to offer support.

- Automated risk monitoring agents can flag weakening cash flows or missed micro-payments before defaults occur using automated risk management tools, giving banks time to offer support.

This shift transforms digital lending platforms from a one-time transaction into an ongoing financial relationship.

Business and Operational Benefits of Scaling Lending with AI Underwriting Agents

Process More Loans Without Extra Staff

Implementing AI underwriting agents in digital lending allows banks to process applications faster and handle larger volumes. Loan officers no longer spend hours manually reviewing documents or calculating financial ratios. Deloitte reports that banks using machine learning lending and automated risk management systems can manage up to 50% more loans annually without increasing headcount. This means growth without a proportional increase in operational costs.

Detect Risks Earlier with Automated Tools

Traditional underwriting can overlook subtle risks due to human error or inconsistent analysis. AI-powered credit scoring for online loans and automated risk assessment tools for digital loans continuously monitor portfolios and flag potential defaults early. A UK fintech reduced SME underwriting time from three days to 30 minutes while boosting approval rates by 20% using AI credit evaluation. Banks using AI in underwriting can scale safely without compromising portfolio quality.

Reduce Errors and Maintain Regulatory Compliance

Manual calculations for ratios, risk scores, and cash-flow models often result in errors that impact lending decisions. By using credit scoring AI and automation in risk management, banks significantly reduce mistakes. McKinsey reports that AI-driven scoring models cut default rates by up to 15%, while ensuring consistency for audits and regulatory requirements. Accurate financial data protects banks and builds borrower trust.

Improve Borrower Experience with Faster Approvals

Borrowers now expect quick and transparent decisions. With AI for underwriting, banks can provide digital loan approval in hours instead of days. ING’s AI-driven onboarding for KYC and AML reduced processing time by 90% and lowered staff workload by 30%. Faster approvals improve customer satisfaction, increase repeat business, and strengthen trust in digital lending platforms.

Enable Sustainable Growth Through Scalable Operations

Traditional lending teams hit capacity limits quickly. Scaling digital lending platforms with AI underwriting allows banks to approve more applications while maintaining risk standards. Continuous monitoring via risk assessment tools for digital loans supports portfolio growth and operational efficiency, making scaling sustainable over time.

Strengthen Trust in Global Trade

Conclusion

AI underwriting agents are changing how banks handle loans. By automating tasks like checking documents, calculating financial ratios, and assessing risk, digital lending platforms can process more applications faster and more accurately. Loan automation and AI credit evaluation reduce mistakes and make lending more consistent, while automated risk assessment helps keep portfolios compliant.

Using AI underwriting lets banks grow their lending operations without hiring more staff, deliver faster decisions to borrowers, and build stronger customer trust. Banks that use these tools wisely can expand credit access, serve more customers, and stay competitive in the changing digital finance world.

Share this article